HSIE Institutional Report: Astral Feb, 11 2026

Authored By Prime Research | Last Modified: Feb 11, 2026 01:29 PM IST

Growth Momentum Builds; Market Share to Rise

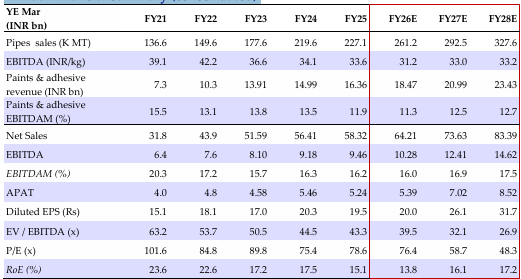

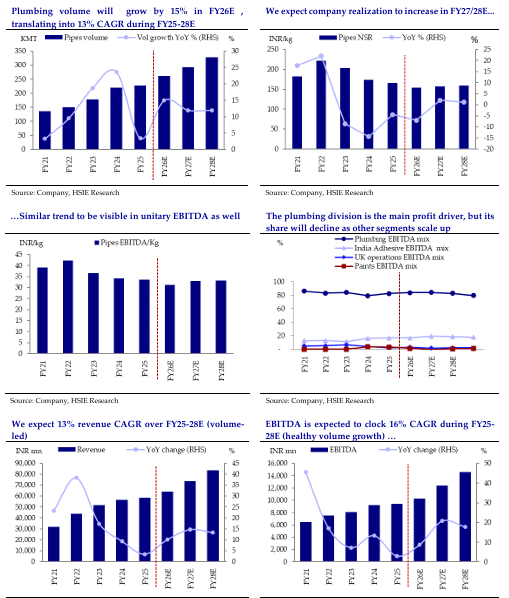

We met with Astral ED and CFO Mr. Hiranand Savlani. The management highlighted that plumbing demand has picked up in Q4, aided by channel restocking, with January plumbing volume growth exceeding 20% YoY. Management anticipates the company’s plumbing volume growth to exceed 14% for FY26. Management reiterated their focus on expanding its value-added portfolio to drive growth and support margin expansion. India’s adhesives business continues to post double-digit growth, while the company targets 15% revenue growth with 15-16% EBITDA margins in FY26. Following several corrective measures, the UK adhesive business is showing signs of recovery, while the paint and bathware segments are expected to grow by around ~20%. The company will incur INR 1.2bn capex for CPVC resin plant over the next one year. Apart from this, the company doesn’t expect any major expansion capex for the next two years. The new CPVC resin plant should boost the company’s margins and help capture more market share. We anticipate healthy plumbing volumes in Q4, fueled by demand revival, market share gain, and normalizing channel inventories amid recovering PVC prices. We forecast volume/revenue/ EBITDA/APAT CAGRs of 13/13/16/18% during FY25-28E. We like Astral due to its strong plumbing volume growth, favorable product mix (high CPVC revenue share), healthy margins and return ratios, and robust balance sheet. We broadly maintain our estimates. We maintain BUY with an unchanged TP of INR 1,900/sh by valuing the company at 60x Mar-28E EPS.

Plumbing Demand Remains Healthy; PVC Prices on Recovery Path

The company highlighted that it has gained market share in Q3, aided by ramp up of Hyderabad and Kanpur plant. Plumbing demand in Q4 has picked up, aided by channel restocking, with January plumbing volume growth exceeding 20% YoY. Management anticipates plumbing volume growth to remain more than 14% for FY26. It noted that PVC resin prices are rising from January onward, with most of the increase passed on to the market, and sees potential for inventory gains in Q4.

Decent India Adhesive Performance; UK Operations on Recovery

India’s adhesives business continues to post double-digit growth, while the company targets 15% revenue growth with 15-16% EBITDA margins in FY26. The UK operations achieved ~9% YoY revenue growth in 9MFY26, with EBITDA margins at ~3%; management expects double-digit revenue growth and margins to improve in FY27. In paints, it projects at least 20% revenue growth in FY26 to reach INR 2.4bn, with Q3 momentum carrying into Q4. However, higher employee and other costs are pressuring margins, prompting plans to rationalize manpower expenses over the next 2-3 quarters. The company aims for 12-14% EBITDA margins in the adhesives and paints segment for FY26, though this appears challenging after achieving about 10.8% in 9MFY26. In bathware, the company aims for 20-25% annual revenue growth over the next five years. The segment is nearing EBITDA breakeven, with expectations to contribute to profits from FY27 onward.

Focus on Expanding Value-Added Mix

The company remained focused on expanding its value-added product mix—including water tanks, valve projects, fire sprinkler pipes, OPVC, PTMT, and low-noise pipe products. Competition intensity is relatively lower in the value-added segment, supporting better margins for the company. Additionally, the manufacturing of these products is expected to drive stronger revenue growth.

Cpvc Resin Backward Integration to Boost Margins

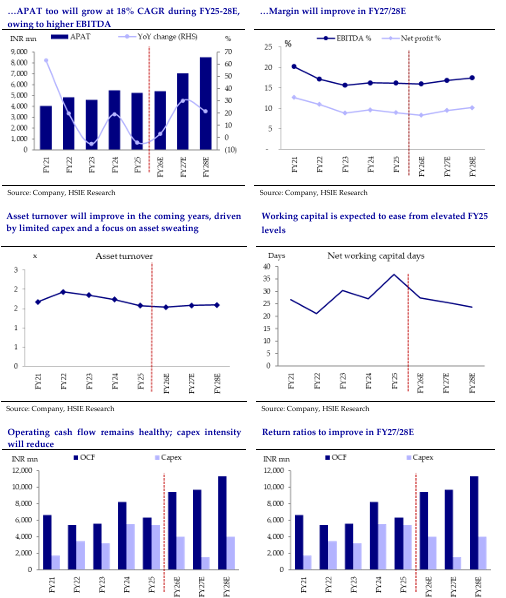

Two quarters back, Astral announced backward integration by acquiring an 80% stake in Nexelon Chem Pvt Ltd to produce CPVC resin. Nexelon’ to start production of its 40,000 MT CPVC resin plant costing INR 1.2b from H2FY27, sufficient to support the Astral’s 46,000 MT CPVC pipes capacity, though some resin will still need to be procured from the market. In-house CPVC production will boost margins and give greater control over pipe quality. It anticipates ~20-25% margins from these operations, though some benefits will be passed on to the market to gain share. We believe the company’s backward integration will drive both volume growth and margin expansion.

Focus on Asset Sweating, Return Ratios to Improve

Company expects to incur INR 3.5bn capex for FY26E (INR 2.9bn incurred in 9MFY26). It will incur INR 1.2bn capex for CPVC resin plant over next one year. Apart from this, company don’t expect any major expansion capex for next two year. During the 9MFY26, the company has increased its pipes and fitting production capacity from 382K MT to 410K MT. The Kanpur plant (~19K MT capacity) has started operations in Q3FY26 and will ramp up gradually in coming quarters as utilisation improves. The company plans to expand O-PVC, PEX, Kanpur and Hyderabad capacities in upcoming quarters, with no greenfield expansions plan. With no further significant expansion planned, major capital expenditures will not arise. This will boost return ratios.

Outlook

We anticipate healthy plumbing volumes in Q4, fuelled by demand revival, market share gain and normalizing channel inventories amid recovering PVC prices. The new CPVC resin plant would help capture more market share and boost the company’s margins. We forecast volume/revenue/ EBITDA/APAT CAGRs of 13/13/16/18%, during FY25-28E. We like Astral due to its strong plumbing volume growth, favourable product mix (high CPVC revenue share), healthy margins and return ratios, and robust balance sheet. We broadly maintain our estimates. We maintain BUY with an unchanged TP of INR 1,900/sh by valuing the company at 60x Mar-28E EPS.

Annual Financial Summary (Consolidated)

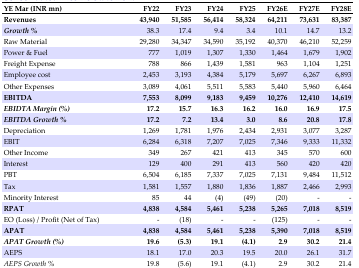

Consolidated Income Statement

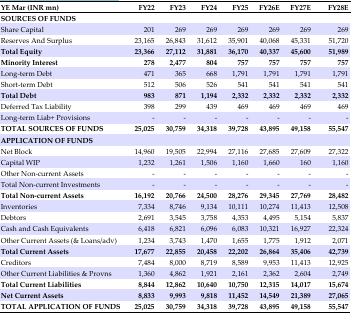

Consolidated Balance Sheet

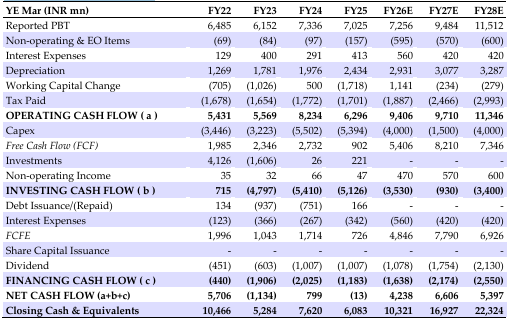

Consolidated Cash Flow

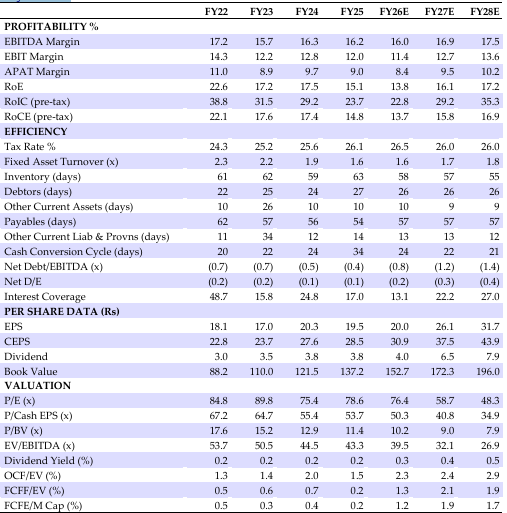

Key Ratios

Astral Price History

Rating Criteria

- BUY: >+15% return potential

- ADD: +5% to +15% return potential

- REDUCE: -10% to +5% return potential

- SELL: >10% Downside return potential

Source: HSIE Research (HSIE Results Daily Report – 11 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.