HSIE Institutional Report: ONGC Feb, 16 2026

Authored By Prime Research | Last Modified: Feb 16, 2026 10:24 AM IST

Crude Production Volume and Realization Declines

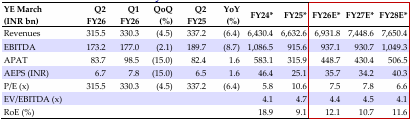

We maintain our REDUCE rating on ONGC, with a target price of INR 220 as we expect slower ramp-up in oil & gas production. Q3FY26 quarter’s reported EBITDA at ~INR 173bn (-8.7% YoY, -2.1% QoQ) and PAT at ~INR 84bn (+1.6% YoY, -15.0% QoQ) were marginally lower than our estimates due to lower-than-expected crude oil production volume.

ONGC Standalone Financial Performance

EBITDA declined to an eight-quarter low of ~INR 173.2bn (-8.7% YoY, -2.1% QoQ) due to lower crude oil production and reduced oil realization. Operating expenditure stood at INR 64.03bn (-1.8% YoY, -7.3% QoQ). Depreciation and depletion costs increased sequentially to ~INR 66.1bn. (-2.5% YoY, +3.8% QoQ) and exploration cost written off increased to ~INR 20.5bn (+6.5% YoY, +86.7% QoQ). Interest cost came in at ~INR 11.5bn (+7.3% YoY, +3.9% QoQ). Other income reduced sequentially to ~INR 30.9bn (+70.8% YoY, 9.6% QoQ).

Standalone Operational Performance

Q3 net crude oil realization stood at a nineteen-quarter low of USD 63.2/bbl (-15.0% YoY, -8.1% QoQ). Gas realization stood at INR 23.5/scm (+5.1% YoY, -1.8% QoQ). Crude oil production was at 4.8mmt (-1.8% YoY, -1.0% QoQ) and gas production was at 5.0bcm (+0.2% YoY, +1.4% QoQ). Total oil sales volume, including JV, was at 4.7mmt (+0.6% YoY, 2.4% QoQ), while gas sales volume was at 3.95bcm (+0.6% YoY, +1.0% QoQ).

Conference Call Takeaways

(1) Consolidated crude oil production stood at 5.12mmt (-2.2% YoY, -1.3% QoQ) and consolidated gas production stood at 5.09bcm (-0.3% YoY, +1.2% QoQ). (2) For the 9MFY26, 18% of the total gas production was New Well Gas (NWG) which has resulted in additional revenue to the tune of INR 50bn. Management expects 24% of gas production in FY27E to be NWG. Management reiterated its target of achieving 35,000-40,000 bpd of peak crude oil production and 7-8mmscmd of gas production from KG 98/2 field with gas production reaching 5-6mmscmd by the end of FY27. (3) OPaL – is running at 90%+ capacity utilization. 9MFY26 revenue/EBITDA stood at INR 97.9/3.53bn respectively and net debt stood in the range of INR 230-240bn. Management does not intend to infuse any further funds into this entity and expects petchem prices to move up in FY27 leading to better profitability. (4) Guidance – with the natural decline at the Mumbai High being arrested and Daman upside expected to produce 4-5mmscmd of gas in FY27, management has guided for 21mmt of oil production and 21.5mmt of gas production in FY27. (5) FY26E capex guidance for standalone entity maintained in the range of INR 320-330 bn with focus on exploration and production.

Change in Estimates and Valuation

We have reduced our FY26/27E EPS estimates by 0.6/3.4% to INR 35.67/34.21, owing to lower-than-expected crude oil production volume reported in Q3FY26. We value ONGC’s standalone business and OVL at 7x Mar-27E EPS at INR 155 and investments at INR 65, leading to a TP of INR 220. The stock is currently trading at 7.8x Mar-27E EPS.

Standalone Financial Summary

Changes in Estimates

Source: HSIE Research (HSIE Results Daily Report – 16 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.