HSIE Institutional Report: LG Electronics India Feb, 13 2026

Authored By Prime Research | Published at: Feb 13, 2026 12:24 PM IST

Soft Quarter; Demand Reviving

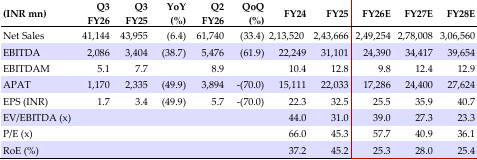

LG’s revenue declined 6% YoY to INR 41.14bn, owing to 10% YoY decline in home appliances segment, while home entertainment division witnessed sub par 2% YoY growth. Management highlighted that home appliance segment witnessed soft demand post Diwali, while the home entertainment segment witnessed initial uplift in demand, driven by GST cut. EBITDA margin declined 270bps YoY to 5.1%, leading to EBITDA/APAT decline of 39/50% YoY. The company expects double-digit revenue growth and mid-teen operating margins in Q4 (higher YoY), supported by robust demand visibility across categories, while guiding for low single-digit revenue growth for FY26. For FY27, the company anticipates double-digit revenue growth coupled with early double-digit margins (broadly in line with FY25 level). The company also targets to double its export contribution by FY27, leveraging emerging opportunities from trade agreements with the US and EU. Considering in-line Q3 performance, we broadly maintain our estimates and retain our ADD rating with an unchanged target price of INR 1,545/share, based on 38x Mar’28E EPS.

LG Electronics India Q3FY26 Highlights

Revenue declined 6% YoY to INR 41.14bn, owing to 10% YoY decline in home appliances segment (68% revenue mix), while home entertainment division witnessed sub-par 2% YoY growth. EBITDA margin declined 270/380bps YoY/QoQ to 5.1%, owing to increase in employee cost and other expenses relative to revenue due to negative operating leverage. Consequently, EBITDA declined 39% YoY. Home appliances and air solutions segment witnessed EBIT margin decline of 310/425bps YoY/QoQ to 4%, whereas home entertainment segment witnessed margin erosion of 390/300bps YoY/QoQ to 9.6%. APAT declined 50% YoY owing to lower EBITDA, higher depreciation and tax rate. Company has booked INR 125mn expense on account of new labor law and INR 173mn prior-period tax expenses, We have classified both these expenses as exceptional items.

Earnings Call Takeaways and valuation

The company expects double-digit revenue growth and mid-teen operating margins in Q4 (higher YoY), supported by robust demand visibility across categories, while guiding for low single-digit revenue growth for FY26. For FY27, the company anticipates double-digit revenue growth coupled with early double-digit margins (broadly in line with FY25 level). The company implemented 2-3% price hikes on refrigerators and washing machines in Nov-25 to offset rising costs. Exports currently account for 7% of revenue. US and EU trade agreements are set to accelerate company growth, with management targeting a doubling export in FY27. Considering in-line Q3 performance, we broadly maintain our estimates and retain our ADD rating with an unchanged target price of INR 1,545/share, based on 38x Mar’28E EPS.

Financial summary

Source: HSIE Research (HSIE Results Daily Report – 13 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.