HSIE Institutional Report: PNC Infratech Feb, 11 2026

Authored By Prime Research | Last Modified: Feb 11, 2026 12:14 PM IST

Muted Performance

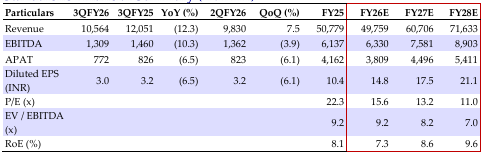

PNC Infratech (PNC) reported Q3FY26 revenue/EBITDA/APAT of INR 10.6/1.3/0.8bn, a miss on our estimates by -13.2/-19.4/-22.6% respectively. FY26 has been impacted by a prolonged monsoon, lower tendering, delay in appointed dates, subdued execution in water & canal, stretched JJM receivables and land availability issues. The OB as of Dec’25 stood at INR 193bn (~3.8x FY25 revenue). Road Highway, Road Expressway, Railway, Airport Runway and Canal EPC projects constitute 71% of OB. FY26 revenue is expected to decline 10% YoY vs. +5% growth earlier, with an EBITDA margin of 12.5% and OI for FY26 expected at INR 120bn (Q4FY26: INR 60bn). OB remains diversified, comprising Solar+BESS and mining projects (revenue guidance – INR 1/5/6bn in FY26/27/28 respectively). PNC’s standalone has INR 13bn cash and robust FY26 order backlog. We expect orders awards to pick up in FY27, new revenue streams like renewables and mining to aid order inflow and bid pipeline of INR 287bn remains healthy. We have cut estimates and valuation multiple to factor slow ordering; maintain BUY with a reduced SOTP of INR 318/sh (12x Dec-27E EPS vs. 14x, 1.2x FCFE Dec-27E for BOT, and 1.1x P/BV for HAM).

PNC Infratech Q3FY26 Financial Highlights

Revenue stood at: INR 10.6bn (-12.3/+7.5% YoY/QoQ, a miss by 13.2%). EBITDA: INR 1.3bn (-10.3/-3.9% YoY/QoQ, a miss by 19.4%). EBITDA margin: 12.4% (+28/-146bps YoY/QoQ, vs. our estimate of 13.3%). APAT: INR 0.8bn (-6.5/+6.1% YoY/QoQ, a beat of 22.6%).

Robust Order Pipeline Supported by RE and Mining

The OB as of Dec’25 stood at INR 193bn, including solar+BESS (to be executed in 24 months) and coal mining project (to be executed in five years). Road highway, road expressway, railway, and canal EPC projects constitute 83% of the total OB. The company guided for its FY26 OI at INR 120bn (Q4FY26 OI expected at INR 60bn). The current bid pipeline stands at INR 287bn. The total OB of RE and mining stands at INR 49.6bn.

Strong Balance Sheet Through Strategic Asset Monetization

PNC’s standalone debt stands at INR 11bn as of Dec’25, while net D/E is at 0.19 (Sep’25: 0.14x). The total equity investment in ongoing/awarded HAM projects stands at INR 17.44bn, of which INR 11.1bn has been infused until Dec’25 with a balance of INR 6.3bn to be spread across FY26/27/28. NWC days stood at 137/139/113 as of Dec’25/Sep’25/Mar’25. Capex in 9MFY26 stood at INR 1.25bn while annual capex targeted in FY26/27 stands at INR 4/1.5bn. Management has guided for equity requirement of INR 4bn for BESS, spread across FY27/28.

PNC Infratech Standalone Financial Summary (INR mn)

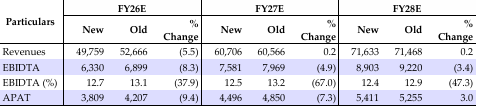

Change in Estimates (INR mn)

Source: HSIE Research (HSIE Results Daily Report – 11 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.