Kotak Bank Emerges Top Nifty Loser Despite Strong Results As RoE Concerns Keep Investors Wary

Authored By HDFC SKY | Last Modified: May 4, 2026 02:34 PM IST

Mumbai, May 4: Shares of Kotak Mahindra Bank fell as much as 5% to emerge as the top Nifty loser, even as the lender posted a strong set of March quarter numbers—highlighting a classic market reaction where good results weren’t good enough.

The stock’s decline comes despite the bank reporting a 13% year-on-year jump in net profit to about ₹4,027 crore, beating Street estimates, alongside steady loan growth and improving asset quality.

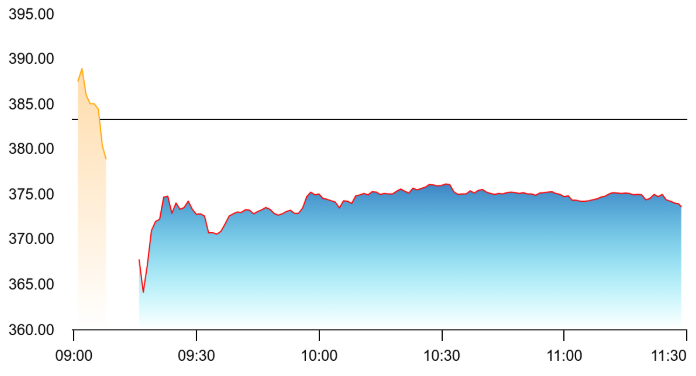

At the time of writing, the stock was down over two percent at Rs 375.

The stock is trading in the red as return on equity (RoE) continues to lag peers. Source: NSE

So why the fall?

At the heart of the reaction lies concerns around return ratios, particularly return on equity (RoE), which continues to lag peers. Brokerages broadly acknowledged that the quarter was operationally strong—margins improved sequentially, credit costs declined and asset quality strengthened—but flagged that profitability metrics are still not catching up with competitors.

Under Scrutiny

This is a critical point. In banking, RoE is the market’s ultimate report card, and Kotak’s inability to match peers on this front is becoming a persistent overhang. Even as margins expanded to 4.67% sequentially and NPAs declined, the bank’s overall capital efficiency remains under scrutiny.

There’s also a growth-versus-profitability trade-off at play. While loan growth has been healthy—advances rising around 16%—and deposits up about 15%, investors appear to be questioning whether this growth is translating into sufficiently strong shareholder returns.

Adding to the pressure is the fact that the stock has underperformed over a longer horizon, declining more than 10% over the past year compared to a relatively flat Nifty. That underperformance raises the bar for earnings—markets are not just looking for beats, but for a clear re-rating trigger.

Shifting Expectations

In essence, the market reaction reflects a shift in expectations. Kotak delivered a clean, stable quarter, but not a transformative one. With peers in the private banking space delivering stronger return profiles, investors are rotating towards names where profitability metrics look sharper.

Brokerages remain constructive in parts—some maintaining ‘buy’ ratings citing improving asset quality and stable margins—but the consensus takeaway is nuanced: earnings quality is solid, but valuation upside may be capped until RoE meaningfully improves.

The fall, therefore, is less about disappointment in the numbers and more about what’s missing from them—a decisive improvement in returns.

In market terms, Kotak didn’t stumble; it simply didn’t sprint fast enough in a race where peers are accelerating.

Source:

- https://www.nseindia.com/get-quote/equity/KOTAKBANK/Kotak-Mahindra-Bank-Limited

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.

Please Note: The information shared is intended solely for informational purposes and does not make any investment recommendations