RBI's Liquidity Absorption via VRRR Auction: Why Funds in SDF Have Narrowed to ₹1 Lakh Crore

Authored By Shishta Dutta | Last Modified: Jul 30, 2025 04:39 PM IST

The Reserve Bank of India (RBI) is once again in the spotlight, not for changing interest rates, but for how it’s managing surplus liquidity in the system.

The RBI has sharply reduced the amount of funds banks are parking under its Standing Deposit Facility (SDF) through a series of large-scale Variable Rate Reverse Repo (VRRR) auctions. Just a few weeks ago, SDF balances were consolidating between ₹2–3 lakh crore, and as of mid-July 2025, that figure has dropped to nearly ₹1 lakh crore.

This time, it is not just a routine liquidity adjustment but shows how the RBI is relying more on dynamic tools to manage short-term money market conditions. This shift is forcing central banks to adapt in a system flooded with funds, which is also going to affect rates and ultimately borrowers.

Therefore, discussing the technical aspects and context behind this broader implication is crucial.

What are VRRR and SDF?

Standing Deposit Facility (SDF)

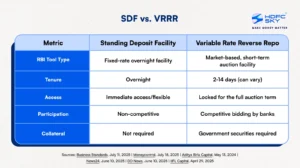

SDF is a passive liquidity absorption tool introduced by the RBI in April 2022, which aims to absorb excess liquidity from the banking system. Through this facility, banks can temporarily deposit their surplus funds with the RBI. The interest rate is fixed here but remains below the repo rate.

Most importantly, there is no collateral requirement, allowing central banks to manage excess liquidity without disruption.

Variable Rate Reverse Repo (VRRR) Auctions

VRRR is a short-term dynamic liquidity tool where banks bid to park surplus funds. The rate is auction-based and usually hovers near the repo rate. Mostly, it may offer better returns than the fixed SDF rate. It aligns more closely with the repo and helps keep the call rate within the policy corridor. It is the rate at which short-term funds are borrowed and lent in the money market.

The mechanics behind VRRR operations:

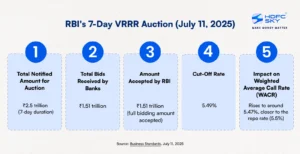

- Auctions are held regularly, mostly for 7-day terms.

- Banks submit competitive bids, and only the best offers (closest to repo) are accepted.

- In July, final rates for VRRR settled around 5.47–5.49%.

Think of SDF as the RBI’s quiet savings account for banks, which is simple and safe. On the other hand, VRRR works more like a short-term investment option that usually offers better returns but is a little competitive.

Why Did SDF Balances Fall So Sharply in July 2025?

To put it simply, it was the liquidity glut that eventually led to a fall in SDF balance. In July 2025, the banking system was in surplus, where liquidity crossed ₹4 trillion at one point. This surge mainly happened because the RBI transferred ₹2.69 trillion surplus to the government. Meanwhile, strong tax collections, especially GST, and a stable rupee led to high capital inflows.

With so much cash in the system, the RBI had to act to prevent short-term rates from falling below its comfort zone.

In response, the RBI conducted VRRR auctions of up to ₹2.5 lakh crore between July 11 and 18. Banks responded actively by bidding near or above the notified amount. This shift negatively affected the SDF usage:

- June 27: ₹2.24 lakh crore parked in SDF.

- July 16: Down to ₹1.09 lakh crore.

Most of the surplus was now routed through VRRR, which shows a strategic reshuffling by banks.

Why Banks Prefer VRRR Over SDF?

The reasons are straightforward. Banks receive a better interest rate from VRRR, while SDF allows banks to park extra money with the RBI overnight at a fixed rate (currently 5.25%). This rate remains 25 basis points below the repo rate.

Even a 15–20 basis point (a standard unit for measuring interest rates) advantage matters to banks. The plus point here is that the higher return by VRRR comes without any increased risk.

Stronger Policy Transmission

RBI Governor Sanjay Malhotra has stated that changes in interest rates must be reflected in the market promptly, so that the central bank’s policy can function effectively. If overnight interest rates drop too much below the RBI’s main rate (called the repo rate), it weakens the effect of rate hikes or pauses.

Currently, the RBI is helping to keep short-term interest rates closer to the repo rate by utilising VRRR auctions to absorb the excess liquidity. This is how they ensure their policy decisions reach banks and borrowers.

What to Watch Next

- The RBI is likely to continue with both VRRR and SDF by adapting them based on liquidity conditions.

- More surplus is expected with another CRR unwind scheduled for September 2025. That means, more VRRR auctions will follow.

- Government outflows, such as GST and bond redemptions, will also impact short-term liquidity and the RBI’s response.

Final Thought

We should not consider a drop in SDF balances a red flag. It is just that the RBI is actively using flexible tools to guide liquidity in the right direction. From the banks’ perspective, making better use of surplus funds and for the RBI, it is about better control.

This move helps keep short-term interest rates aligned with the RBI’s policy rate. It also shows that the RBI is adapting to a more dynamic liquidity environment by relying less on passive tools and more on active ones.

As liquidity conditions continue to evolve, such fine-tuned strategies will likely become the norm. Eventually, this idea will shift how central banking operates in high-liquidity times.

Disclaimer: At HDFC SKY, we take utmost care and due diligence in curating and presenting news and market-related content. However, inadvertent errors or omissions may occasionally occur.

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.

Please note that the information shared is intended solely for informational purposes and does not make any investment recommendations