Tata Elxsi Shares Tumble 5% As June Quarter Performance Upsets Investors

Authored By HDFC SKY | Published at: Jul 15, 2026 05:50 PM IST

Mumbai, July 15: Tata Elxsi share price slumped nearly 5% on Wednesday after the engineering research and design (ER&D) company reported a June-quarter performance that disappointed investors, prompting brokerages to cut earnings estimates and maintain bearish ratings. While the company delivered year-on-year growth in revenue and profit, sequential performance remained muted, margins came under pressure and demand weakness in its key transportation business continued to weigh on sentiment.

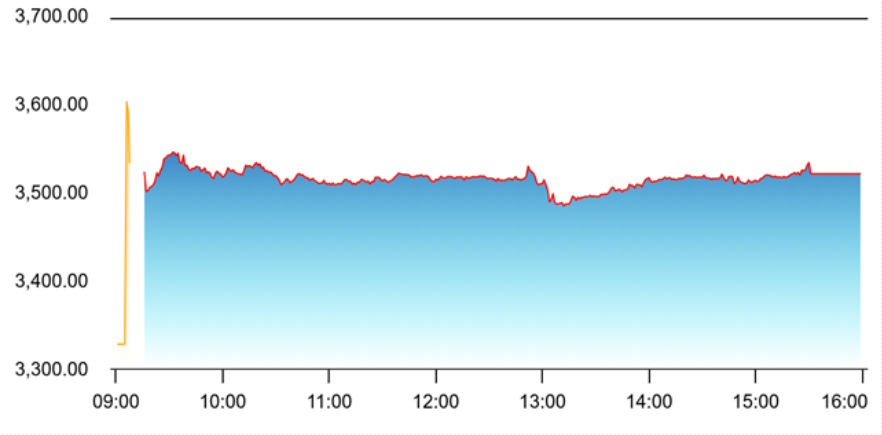

The decline came despite Tata Elxsi reporting a net profit of Rs 170.6 crore for the first quarter of FY27, up 18.2% year-on-year, while revenue from operations increased 14.5% to Rs 1,021.1 crore. However, revenue rose just 2.8% sequentially, missing the market’s expectations. At close the stock was down 4.8% at Rs 3,520.40.

Brokers See Downside

Brokerages reiterated ‘Sell’ rating on the stock and lowered target price, implying a downside of up to 16%.

According to the brokerages, Tata Elxsi’s revenue growth in constant currency terms was broadly in line with expectations, but the improvement was largely driven by the media and communications vertical. Its two largest businesses—transportation and healthcare—continued to remain weak, raising concerns over the pace of recovery.

The stock fell as investors and brokers lamented earnings. Source: NSE

The brokerages also highlighted that recent investments and large deal wins have yet to translate into meaningful revenue acceleration, while continued pricing pressure and higher employee costs are weighing on margins.

Margins Remain a Key Concern

Apart from slower revenue growth, investors were concerned about profitability.

Brokerages noted that margins remained under pressure as Tata Elxsi continued to invest in new capabilities and absorb costs associated with large transformation programmes. The company has also been witnessing slower decision-making by global clients, particularly in the automotive segment, delaying project ramp-ups and impacting utilisation levels.

The transportation vertical, which contributes the largest share of Tata Elxsi’s revenue, remained weak amid a slowdown in spending by global automotive manufacturers. Demand in healthcare also remained subdued, offsetting strength in media and communications.

Automotive Weakness Continues

The automotive business continues to be the biggest challenge for Tata Elxsi.

Global automobile manufacturers have remained cautious on discretionary engineering spending amid macroeconomic uncertainty and changing electric vehicle investment priorities. Although the company has secured several large deals over the past few quarters, analysts believe meaningful revenue contribution from these contracts may take longer than initially expected.

Brokerages said the slower-than-expected recovery in automotive engineering services is likely to keep revenue growth moderate over the next few quarters.

Brokerages Cut Earnings Estimates

Following the quarterly results, brokerages revised their earnings forecasts lower to reflect slower revenue growth and weaker margins.

They trimmed earnings estimates over FY27-FY29 and retained negative stance, arguing that the stock’s valuation remains expensive despite the recent correction. At current levels, the brokerages believe the risk-reward remains unfavourable given the lack of near-term earnings catalysts.

Analysts cited persistent weakness in the transportation vertical, delayed deal execution and limited visibility on margin improvement.

Long-Term Growth Drivers Intact

Despite the near-term challenges, analysts acknowledged that Tata Elxsi remains well positioned in high-growth areas such as software-defined vehicles, artificial intelligence, healthcare technology and digital engineering.

The company continues to invest in next-generation technologies and has built a healthy pipeline of large strategic deals. However, investors are likely to seek evidence of sustained execution and stronger demand before turning more constructive on the stock.

Outlook

The sharp decline in Tata Elxsi’s share price underscores the market’s sensitivity to slowing growth and margin pressures in the ER&D sector. While the company continues to report healthy year-on-year growth, analysts believe sequential execution and recovery in the automotive business will be the key variables to watch over the coming quarters.

With brokerages maintaining cautious recommendations and trimming earnings estimates, investor sentiment is expected to remain subdued until there are clearer signs of an improvement in demand, margins and deal conversion.

Source

- https://www.nseindia.com/get-quote/equity/TATAELXSI/Tata-Elxsi-Limited

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.

Please Note: The information shared is intended solely for informational purposes and does not make any investment recommendations