Nifty 50

- Maruti Suzuki₹14,149737.00 (5.50%)

- Eicher Motors₹7,106-320.00 (-4.31%)

- Titan Company₹4,423.70146.50 (3.43%)

- Tata Consumer ₹1,073-39.80 (-3.58%)

- Adani Enterprises₹3,043.1080.60 (2.72%)

- TCS₹2,033-64.90 (-3.09%)

- Bajaj Finance₹1,00724.95 (2.54%)

- Infosys₹1,005.90-30.80 (-2.97%)

- Eternal₹265.255.85 (2.26%)

- Wipro₹170.35-5.13 (-2.92%)

- Adani Ports₹1,810.2034.10 (1.92%)

- HCL Technologies₹1,072-30.40 (-2.76%)

- Nestle₹1,413.8026.50 (1.91%)

- Tech Mahindra₹1,405.50-28.30 (-1.97%)

- Shriram Finance₹1,04613.35 (1.29%)

- Max Healthcare₹1,129-20.90 (-1.82%)

- SBI Life Insurance ₹1,77721.60 (1.23%)

- HDFC Life Insurance ₹575-8.25 (-1.41%)

- Cipla₹1,46813.90 (0.96%)

- Hindustan Unilever₹2,123.30-28.00 (-1.30%)

- Offerings

- Tools & Platforms

Tools & Calculators

- Open API

- Calculators

- SIP Calculator

- CAGR Calculator

- Compound Interest Calculator

- FD Calculator

- RD Calculator

- EPF Calculator

- Retirement Calculator

- HDFC SIP Calculator

- Mutual Fund Return Calculator

- Lumpsum Calculator

- Step Up SIP Calculator

- ETF SIP Calculator

- Brokerage Calculator

- Equity Margin Calculator

- SWP Calculator

- EMI Calculator

- MTF Calculator

- Margin Pledge Calculator

- Markets

Stocks

F&O

Mutual Funds

- More

Arohan Financial Services Limited IPO

TBA/TBA shares

Minimum Investment

IPO Details

TBA

TBA

₹TBA

TBA

₹TBA to TBA

NSE, BSE

TBA

TBA

Arohan Financial Services Limited IPO Timeline

Bidding Start

TBA

Bidding Ends

TBA

Allotment Finalisation

TBA

Refund Initiation

TBA

Demat Transfer

TBA

Listing

TBA

Explore IPO Opportunities

Explore our comprehensive IPO pages to stay updated on the latest trends and insights.

Arohan Financial Services Limited IPO

IPO Details

- Open date: TBA

- Close Date: TBA

- Minimum Investment: To be updated

- Lot Size: TBA

- Price Range: TBA

- Listing: BSE, NSE

- Issue Size: Fresh Issue of ₹600 crore + OFS of up to 4.04 crore equity shares

- Listing Date: TBA

IPO Timeline

- Bidding Start: TBA

- Bidding Ends: TBA

- Allotment Finalisation: TBA

- Refund Initiation: TBA

- Demat Transfer: TBA

- Listing: TBA

About Arohan Financial Services Limited

Incorporated in 2006, Arohan Financial Services Limited is a technology-enabled non-banking financial company – microfinance institution (NBFC-MFI) offering income-generating loans and a suite of financial and non-financial products to underserved and unserved customers across rural and semi-urban regions of India. The company operates through the Joint Liability Group (JLG) model, offering collateral-free loans to low-income households with an annual household income of ₹300,000 or less. Arohan is part of the Aavishkaar Group, which manages assets in excess of USD 1 billion across equity and credit. The company has a bank loan rating of A- by CARE and A (Stable) by ICRA, along with MFI grading of MF1 from CARE Ratings.

Arohan Financial Services Limited IPO Overview

Arohan Financial Services Limited’s initial public offering is a book-built issue comprising a fresh issue of up to ₹600 crore and an offer for sale of up to 4.04 crore equity shares by existing investors including US Teachers Insurance and Annuity Association, Michael & Susan Dell Foundation, Aavishkaar Goodwell India Microfinance Development Company-II Ltd, Tano Capital, TR Capital III Mauritius, and Danish Sustainable Development Goals Investment Fund. The DRHP was filed with SEBI on May 15, 2026. The equity shares are proposed to be listed on BSE and NSE. DAM Capital Advisors, Motilal Oswal Investment Advisors, and SBI Capital Markets are the book-running lead managers, while MUFG Intime India Private Limited is the registrar of the issue. The net proceeds from the fresh issue will be utilized to augment the company’s capital base to meet future business requirements towards onward lending and for general corporate purposes. The company’s shareholding pre-issue stands at 15,94,12,320 equity shares.

Arohan Financial Services Limited Upcoming IPO Details

| Category | Details |

| Issue Type | Book Built Issue IPO |

| Total Issue Size | Fresh Issue of ₹600 crore + OFS of up to 4.04 crore equity shares |

| Fresh Issue | [●] shares (aggregating up to ₹600 crore) |

| Offer for Sale (OFS) | 4,04,37,529 shares (aggregating up to ₹[●] crore) |

| IPO Dates | TBA |

| Price Bands | TBA |

| Lot Size | TBA |

| Face Value | ₹10 per share |

| Listing Exchange | BSE, NSE |

| Shareholding pre-issue | 15,94,12,320 shares |

| Shareholding post-issue | To be updated |

Arohan Financial Services Limited IPO Lots

| Application | Lots | Shares | Amount |

| Retail (Min) | TBA | TBA | TBA |

| Retail (Max) | TBA | TBA | TBA |

| S-HNI (Min) | TBA | TBA | TBA |

| S-HNI (Max) | TBA | TBA | TBA |

| B-HNI (Min) | TBA | TBA | TBA |

Arohan Financial Services Limited IPO Reservation

| Investor Category | Shares Offered |

| QIB Shares Offered | Not more than 50% of the Offer |

| Retail Shares Offered | Not less than 35% of the Offer |

| NII (HNI) Shares Offered | Not less than 15% of the Offer |

Arohan Financial Services Limited IPO Valuation Overview

| KPI | Value |

| Earnings Per Share (EPS) | ₹3.98 |

| Price/Earnings (P/E) Ratio | TBD |

| Return on Net Worth (RoNW) | 2.90% |

| Net Asset Value (NAV) | ₹136.97 |

| Return on Equity (RoE) | 2.95% |

| Return on Capital Employed (RoCE) | 3.93% |

| EBITDA Margin | 41.73% |

| PAT Margin | 5.38% |

| Debt to Equity Ratio | 2.50 |

Objectives of the IPO Proceeds

The Net Proceeds are intended to be utilized as per the details provided in the table below:

| Particulars | Amount (in ₹ million) |

| Augmenting capital base to meet future business requirements towards onward lending | 6,000.00 |

| General corporate purposes* | [●] |

*To be determined upon finalisation of the Offer Price and updated in the Prospectus prior to filing with the RoC.

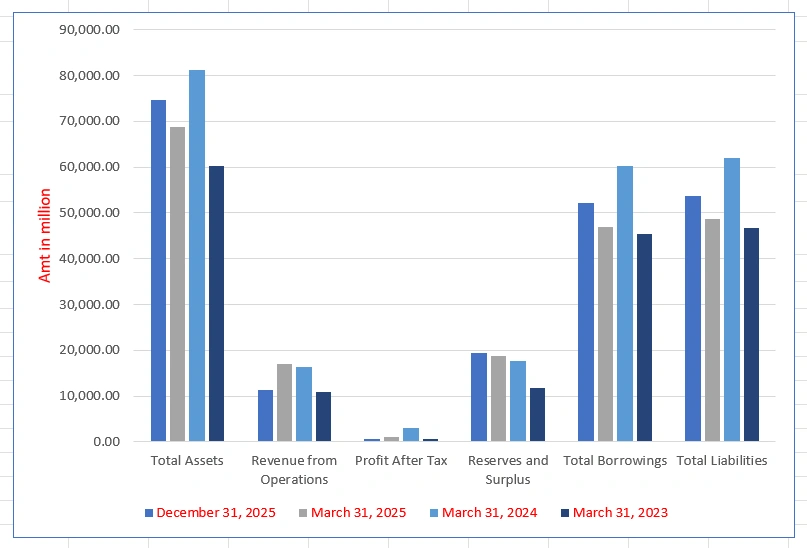

Arohan Financial Services Limited Financials (₹ in Millions)

| Particulars | December 31, 2025 | March 31, 2025 | March 31, 2024 | March 31, 2023 |

| Total Assets | 74,618.38 | 68,857.87 | 81,154.41 | 60,181.71 |

| Revenue from Operations | 11,281.34 | 16,917.48 | 16,286.93 | 10,875.34 |

| Profit After Tax | 607.44 | 1,096.86 | 3,138.21 | 707.16 |

| Reserves and Surplus | 19,323.95 | 18,662.16 | 17,573.44 | 11,876.37 |

| Total Borrowings | 52,194.32 | 47,034.03 | 60,158.43 | 45,334.90 |

| Total Liabilities | 53,700.31 | 48,606.59 | 62,006.85 | 46,801.46 |

Financial Status of Arohan Financial Services Limited

SWOT Analysis of Arohan Financial Services Limited

| Strengths and Opportunities | Weaknesses and Threats |

| Second largest NBFC-MFI in Eastern India and ninth largest in India by AUM | Significant profit decline of 65% in Fiscal 2025 due to elevated provisions |

| Technology-enabled operations with AI-driven voice bot ‘Arohi’ for collections | Sector-wide asset quality stress with 17% YoY portfolio contraction |

| Strong institutional backing from Aavishkaar Group and marquee investors | Regulatory sensitivity highlighted by 2024 RBI cease-and-desist order |

| Best-in-class asset quality with GNPA of 1.69% and NNPA of 0.39% in Q3 FY26 | High employee attrition exceeding 40% post-pandemic |

| Diversified funding relationships across 41 lenders | Unsecured lending model vulnerable to borrower overleveraging |

| Microfinance sector serving nearly 80 million borrowers | Intense competition from banks and other NBFC-MFIs |

| Industry showing signs of recovery with 3% QoQ growth in Q4 FY26 | Rising operational costs impacting profitability |

| CGFMU credit guarantee cover on 42.86% of AUM reducing credit risk | Reliance on Joint Liability Group model with joint liability risks |

| Expansion into secured lending products like gold and home loans | Macroeconomic shocks affecting low-income borrower repayment |

| Increasing formalisation and digital adoption in microfinance | Regulatory changes affecting NBFC-MFI sector |

Arohan Financial Services Limited IPO Strengths

Strong Rural and Semi-Urban Presence with Extensive Branch Network

Arohan Financial Services Limited has established a robust presence across 17 states and 320 districts in India through a network of 1,073 branches as of December 31, 2025. The company serves 1.95 million active customers, primarily low-income households with annual income of ₹300,000 or less. This extensive reach enables the company to tap into financially under-penetrated rural and semi-urban markets, positioning it as the second largest NBFC-MFI in Eastern India and the ninth largest in India by AUM.

Technology-Driven Operations Enhancing Efficiency and Scale

Arohan Financial Services has built a comprehensive technology infrastructure that processes over 2.50 million transactions monthly as of December 31, 2025. The company’s digital platforms include ‘ApnaArohan’ for customer onboarding, ‘ArohanPrivilege’ for digital loan sourcing, and ‘MeraArohan’ for field operations. The company has also implemented an innovative AI-driven voice bot named ‘Arohi’ for recovery processes, which can cover the entire customer pool in a single day, significantly boosting operational efficiency.

Large Customer Base and Branch Network Driving Scale

The company serves approximately 1.95 million active customers through its 1,073 branches across 17 states. Its applications have been downloaded over 0.67 million times and processed more than 1.50 million transactions as of December 31, 2025, boosting customer engagement and self-service. The company had a workforce of 9,502 employees as of December 31, 2025, supporting its extensive operations.

Strong Risk Management Framework with Best-in-Class Asset Quality

Arohan Financial Services maintains a well-established risk management framework with an independent credit function. The company utilizes ‘NIRNAY’, its proprietary credit scorecard introduced in April 2022, to assist in customer selection and risk-based pricing. Despite the challenging microfinance environment in Fiscal 2025, the company maintained Gross NPA at 2.85% and Net NPA at just 0.53%, among the best in the Top 10 NBFC-MFIs. In Q3 FY26, asset quality further improved with GNPA at 1.69% and NNPA at 0.39%.

Experienced Management Team with Deep Industry Expertise

Arohan Financial Services is led by Managing Director Manojkumar N Nambiar, who has over 16 years of experience in the microfinance industry in India. He is an active director on the board of the MFIN, the sector-level self-regulatory organisation for microfinance institutions. The senior management team collectively brings decades of experience across banking, finance, risk management, and technology, providing strong leadership for the company’s growth trajectory.

Institutional Promoter Ownership and Strong Investor Backing

Arohan Financial Services is part of the Aavishkaar Group, which has over 18 years of experience in advising and nurturing businesses with social impact in India and abroad. The company is backed by marquee investors including US Teachers Insurance and Annuity Association, Michael & Susan Dell Foundation, Tano Capital, and others. This strong institutional backing provides credibility, access to capital, and strategic guidance for the company’s growth.

More About Arohan Financial Services Limited

Business Overview

Arohan Financial Services Limited, incorporated in 2006, is a technology-enabled NBFC-MFI offering income-generating loans and a suite of financial and non-financial products to underserved customers across rural and semi-urban regions of India. The company operates through the Joint Liability Group (JLG) model, providing collateral-free loans to low-income households with an annual household income of ₹300,000 or less.

Product Offerings

The company’s product portfolio includes:

- Credit Offerings: Income-generating loans and other loan products for essential household purposes

- Insurance Products: Arohan is a registered Corporate Agent (Composite) with IRDAI, offering reliable insurance solutions as part of its broader financial inclusion mission

- Term Loans: The company also offers term loans to microfinance institutions

- Digital Platforms: ‘ApnaArohan’, ‘ApnaBazaar’, ‘ArohanPrivilege’, and ‘MeraArohan’ for customer onboarding, loan servicing, and repayments

Branch Network and Geographic Presence

Arohan Financial Services operates across 17 states and 320 districts in India through 1,073 branches as of December 31, 2025. The company serves 1.95 million active customers. The company commenced its business in 2006 with operations in a single location in Kolkata and has gradually expanded its footprint across Eastern, North-Eastern, Central, Northern, Western, and Southern regions of India.

Technology Infrastructure

Arohan has built a comprehensive technology infrastructure that processes over 2.50 million transactions monthly as of December 31, 2025. Key technology platforms include:

- ‘Profile’ (CBS): Core banking system implemented in 2017 to manage lending business

- ‘MeraArohan’: In-house loan origination application enabling real-time recording of operational transactions

- ‘ArohanPrivilege’: Advanced technology-based digital loan sourcing facility with end-to-end customer journeys

- ‘Arohi’: AI-driven voice bot for recovery processes with vernacular capabilities

- ‘Sanjaya’: In-house app for field staff tracking with geotagging and time stamps

Credit Ratings and Certifications

The company maintains strong credit ratings including:

- Bank loan rating of A- by CARE and A (Stable) by ICRA

- MFI grading of MF1 from CARE Ratings

- Coveted GOLD Standard in Client Protection Principles under the CERISE_SPTF Methodology

- Alpha Social Rating with a Positive Outlook from M-CRIL

- COCA Dimensions of C1 by CARE EDGE

- ISO/IEC 27001:2022 certification for information security management

Industry Outlook

India Microfinance Sector Overview

India’s microfinance sector plays a vital role in promoting financial inclusion, currently serving nearly 80 million borrowers. As of March 2025, NBFC-MFIs remained the largest contributors to microfinance loan outstanding, holding a 39% share, followed by banks at 32%, small finance banks at 16%, NBFCs at 12%, and others at 1%. The sector has faced significant challenges in recent years, with borrower overleveraging and tighter lending norms under MFIN Guardrails 2.0 leading to asset quality stress.

Sector Growth and Recovery

The microfinance industry witnessed a 17% year-on-year contraction in total portfolio outstanding between March 2025 and March 2026. However, the latest data indicates an inflection point, with the sector portfolio recording a 3% quarter-over-quarter growth between December 2025 and March 2026 for the first time in several quarters, signalling a resumption of growth momentum. Growth for the sector is expected to remain moderate at around 4% in FY2026, with a rebound anticipated in FY2027 as portfolio quality improves.

Key Growth Drivers

- Financial Inclusion: India’s microfinance sector continues to expand its reach to underserved populations, with NBFC-MFIs playing a crucial role in bridging the credit gap

- Government Support: Initiatives like the Credit Guarantee Fund for Micro Units (CGFMU) provide credit guarantee cover for eligible microfinance loans, reducing credit risk for lenders

- Digital Adoption: Increasing use of technology platforms, AI-driven tools, and digital payment channels is improving operational efficiency and customer reach

- Formalisation: The sector is witnessing steady formalisation driven by stronger regulatory oversight, increased adoption of hallmarking, and rising consumer demand for transparency

- Product Diversification: NBFC-MFIs are expanding beyond traditional microfinance into secured lending products, insurance, and other financial services

Asset Quality Trends

Asset quality stress in the NBFC-MFI sector surged in 2024-25 amid borrower overleveraging and operational challenges, with pressure expected to persist in the first half of the current fiscal. However, signs of stabilisation have emerged, with companies like Arohan reporting improving asset quality indicators in Q3 FY26.

How Will Arohan Financial Services Limited Benefit

- The company’s position as the second largest NBFC-MFI in Eastern India and ninth largest in India positions it to benefit from the microfinance sector’s anticipated recovery and growth.

- The industry’s 3% QoQ growth in Q4 FY26 signals a resumption of growth momentum, creating opportunities for the company to expand its portfolio.

- The company’s extensive branch network of 1,073 branches across 17 states provides a strong foundation to capture market share in underserved rural and semi-urban regions.

- The CGFMU credit guarantee cover on 42.86% of AUM reduces credit risk and supports risk-based pricing discipline, improving the company’s risk profile.

- The company’s strong institutional backing from Aavishkaar Group and marquee investors provides access to capital and strategic guidance for growth.

- The company’s proprietary credit scoring model ‘NIRNAY’ and AI-driven tools like ‘Arohi’ enable efficient underwriting and collections, supporting healthy asset quality.

- The company’s planned expansion into secured lending products like gold loans, home loans, and home-improvement loans will diversify the portfolio and reduce risk concentration.

- The company’s focus on cross-sell initiatives through platforms like ApnaBazaar and ApnaArohan will drive non-interest and fee-based income growth.

Peer Group Comparison

| Name of Company | Revenue (₹ in million) | Face Value (₹) | Basic EPS (₹) | Diluted EPS (₹) | NAV (₹) | P/E Ratio | RoNW (%) |

| Arohan Financial Services Limited | 16,917.48 | 10 | 7.20 | 7.18 | 132.60 | NA | 5.42% |

| Peer Group | |||||||

| CreditAccess Grameen Limited | 57,523.30 | 10 | 33.32 | 33.24 | 435.14 | 45.04 | 7.64% |

| Muthoot Microfin Limited | 25,616.93 | 10 | (13.29) | (13.07) | 154.62 | NM | NM |

| Satin Creditcare Network Limited | 25,946.90 | 10 | 16.92 | 16.92 | 231.19 | 12.57 | 7.32% |

| Fusion Finance Limited | 23,197.60 | 10 | (111.41) | (111.41) | 149.51 | NM | NM |

| Spandana Sphoorty Financial Limited | 23,551.60 | 10 | (145.17) | (145.17) | 369.30 | NM | NM |

| Bandhan Bank Limited | 2,49,148.29 | 10 | 17.04 | 17.04 | 151.21 | 12.10 | 11.27% |

| Ujjivan Small Finance Bank Limited | 72,005.87 | 10 | 3.75 | 3.71 | 30.64 | 16.82 | 12.11% |

| Jana Small Finance Bank Limited | 54,856.55 | 10 | 47.89 | 47.67 | 388.96 | 9.55 | 12.25% |

| Utkarsh Small Finance Bank Limited | 43,647.60 | 10 | 0.22 | 0.22 | 27.00 | 70.41 | 0.80% |

| ESAF Small Finance Bank Limited | 43,293.08 | 10 | (10.13) | (10.12) | 37.74 | NM | NM |

| Suryoday Small Finance Bank Limited | 21,710.01 | 10 | 10.82 | 10.75 | 181.28 | 16.74 | 5.97% |

Key Strategies for Arohan Financial Services Limited

Diversify Portfolio Through Geographical Coverage and Cross-Sell Initiatives

Arohan Financial Services intends to diversify its portfolio through geographical expansion, strengthened customer engagement initiatives, cross-sell-led offerings, and selective secured lending. The company plans to introduce differentiated offerings such as ‘Sarathi’, a balance transfer product enabling eligible customers to consolidate lenders with improved pricing. Through ‘ArohanPrivilege’, the company offers a differentiated model for “used-to-credit” customers featuring technology-based lending with cashless repayments. The company also plans to selectively scale secured lending offerings including gold loans, home loans, and home-improvement loans to diversify risk and improve balance-sheet stability.

Strengthen Core Operating Fundamentals Across the Customer and Credit Lifecycle

Arohan Financial Services seeks to capitalise on microfinance opportunities through a disciplined and calibrated sourcing approach, maintaining a balanced mix of new and existing borrowers while differentiating between new-to-credit and used-to-credit segments. The company places significant emphasis on centre discipline, with centres serving as the primary interaction point with borrowers, supporting improved collection efficiency. The recovery function, first established post-demonetisation and subsequently scaled during the COVID-19 pandemic, plays a critical role in managing delinquencies and containing credit costs, complemented by coverage under the CGFMU.

Strengthen Balance Sheet and Improve Operating Leverage

Arohan Financial Services aims to drive higher productivity across its branch network and field teams through process simplification, improved digital workflows, and increased use of centralised credit processes. The company intends to achieve scale efficiencies by leveraging shared infrastructure across both unsecured and secured lending verticals, thereby reducing the marginal cost of origination. The strategy prioritises operating leverage through improved utilisation of existing branch infrastructure, with a focus on driving higher productivity from branches established in recent years and adopting a calibrated approach to incremental branch expansion.

Continue to Improve Customer Experience by Developing Technology Infrastructure

Arohan Financial Services is committed to continuously investing in its information technology platform to ensure scalability and effective internal controls. The company plans to further enhance and automate collections tracking through ‘MeraArohan’ and continue leveraging Aadhaar e-KYC approval to enable end-to-end borrower authentication. The company plans to further scale its digital customer platforms, including ‘ApnaArohan’ and ‘ArohanPrivilege’, which enable customers to apply for loans, receive disbursements, and make repayments digitally, thereby improving accessibility and convenience.

FAQs

How can I apply for Arohan Financial Services Limited IPO?

You can apply via HDFCSky using UPI-based ASBA (Application Supported by Blocked Amount) through your bank account.

What is the total issue size of Arohan Financial Services Limited IPO?

The IPO comprises a fresh issue of ₹600 crore and an OFS of up to 4.04 crore equity shares.

When was the DRHP filed with SEBI for Arohan Financial Services Limited IPO?

The Draft Red Herring Prospectus was filed with SEBI on May 15, 2026.

On which exchanges will Arohan Financial Services Limited shares be listed?

The equity shares are proposed to be listed on both BSE (Bombay Stock Exchange) and NSE (National Stock Exchange).

What is the face value of Arohan Financial Services Limited equity shares?

The face value of each equity share is ₹10 per share.

Infographic Content

Arohan Financial Services Limited IPO Highlights

Arohan Financial Services Limited is a technology-enabled NBFC-MFI serving 1.95 million customers through 1,073 branches across 17 states, offering income-generating loans and financial inclusion products to underserved rural and semi-urban communities.

- Offer Size:₹600 crore (Fresh Issue) + OFS of up to 4.04 crore equity shares

- Purpose:The net proceeds will be utilized to augment the company’s capital base to meet future business requirements towards onward lending and for general corporate purposes.

- Financials (Fiscal Year ended March 31, 2025):Revenue from Operations ₹16,917.48 million; Profit After Tax ₹1,096.86 million; EPS ₹7.20.

- ☑ Listing:Mainboard IPO on BSE & NSE

How to apply IPO with HDFC SKY?

Follow these simple steps to apply for an IPO through HDFC SKY. Secure your investments and explore new opportunities with ease by accessing the IPOs available on the platform.

1Login to your HDFC SKY Account

2Select Issue

3Enter Number of Lots and your Price.

4Enter UPI ID

5Complete Transaction on Your UPI App

By signing up I certify terms, conditions & privacy policy