India’s Household Savings Set to Power Financial Markets with $9.5 Trillion Inflows: Goldman Sachs

Authored By Shishta Dutta | Last Modified: Oct 3, 2025 05:36 PM IST

India’s financial landscape is undergoing a quiet revolution. According to a recent Goldman Sachs report, Indian households are expected to channel $9.5 trillion into financial assets over the next decade, transforming how capital is mobilized across the economy.

As incomes rise, savings preferences evolve, and digital platforms expand, India is poised to undergo a historic shift from physical to financial wealth.

In advanced economies, household wealth has undergone a clear shift toward financial instruments. Pension funds, capital markets, and insurance products now account for the bulk of household asset allocations. Robust financial infrastructure, tax incentives, and long-standing institutional trust have supported this transition.

In contrast, many emerging markets, including India, still see a dominant share of household savings directed toward physical assets such as real estate and gold. This reflects a mix of cultural preferences, inflation-hedging behavior, and limited access to formal financial markets in certain segments.

However, this also highlights the immense untapped potential for financialization in India. As incomes rise, access improves, and investor awareness deepens, household capital is likely to migrate toward more productive financial avenues.

The Rise of Financialisation

Traditionally, Indian households have leaned heavily towards physical assets, real estate, gold, and land. However, Goldman Sachs sees a paradigm shift underway. Over the next 10 years, as a base case, household financial savings are projected to average 13% of GDP, up from the 11.6% seen in the past decade.

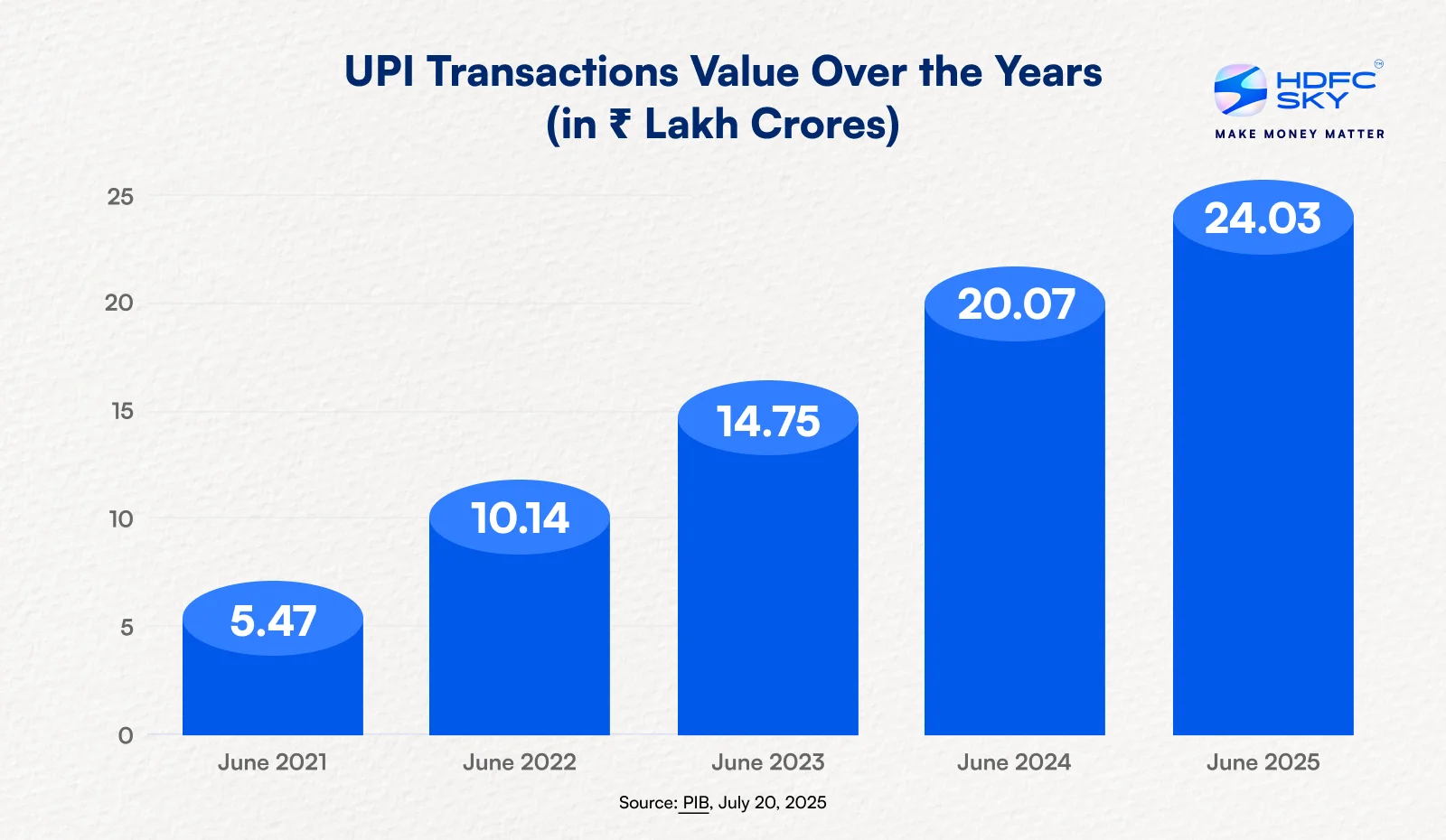

This marks the deepening financialization of India’s savings base. This shift isn’t happening in isolation. It’s being accelerated by India’s rapidly evolving digital infrastructure, especially the rise of real-time payment systems like UPI.

The scale of UPI today is staggering. In June 2025 alone, it facilitated over ₹24.03 lakh crore in payments across 18.39 billion transactions.

There have been several decisive policy nudges over the past two decades that helped accelerate this shift.

- The launch of the National Pension System (NPS) in 2004 introduced the idea of regulated, long-term retirement savings for citizens beyond government employees.

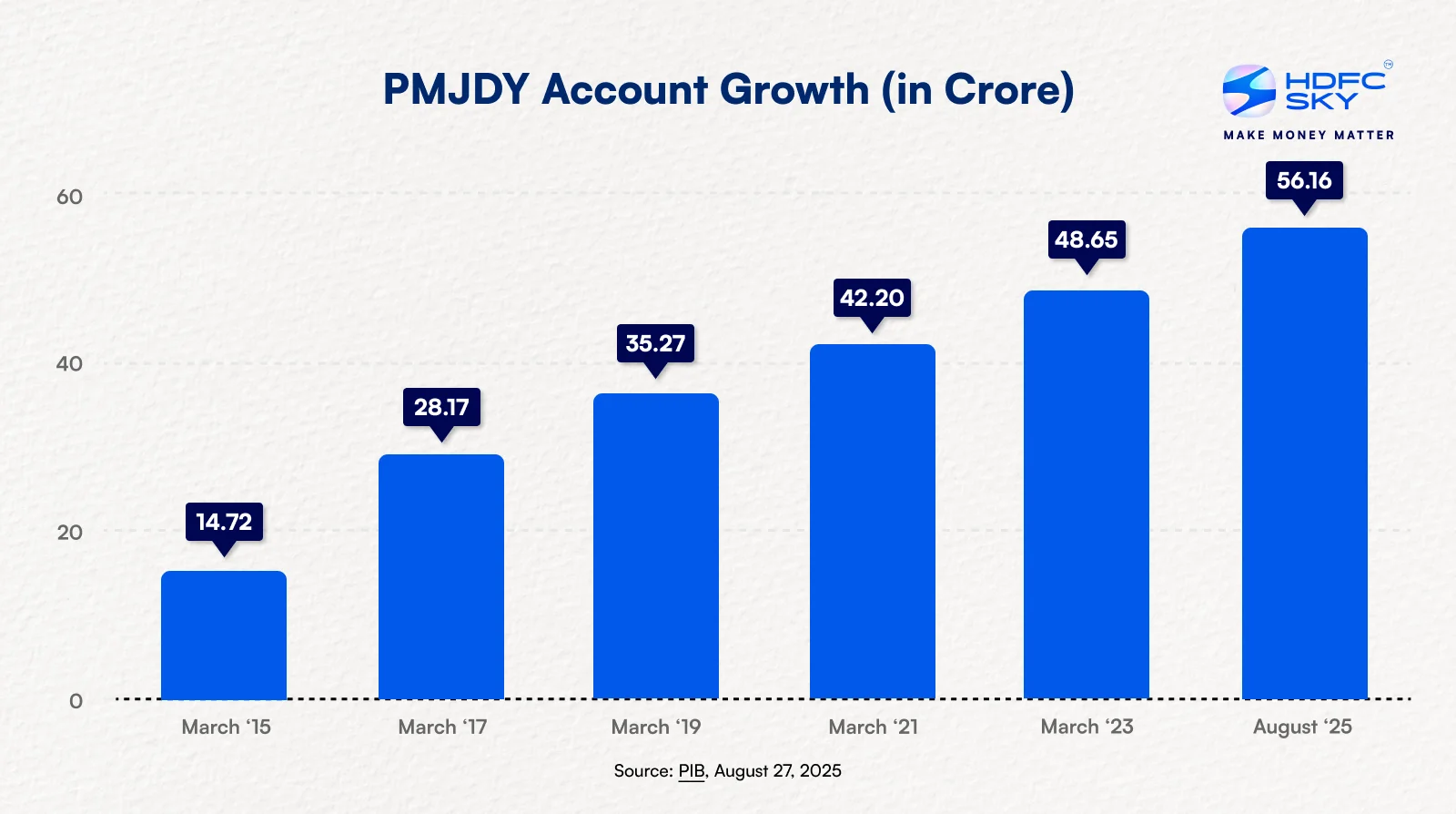

- The Pradhan Mantri Jan Dhan Yojana (PMJDY), introduced in 2014, brought over 56.16 crore unbanked individuals into the formal financial system. It has helped bridge the gap between the banking system and the unbanked, fostering dignity, self-reliance, and deeper economic inclusion.

- The JAM trinity (Jan Dhan-Aadhaar-Mobile) enabled seamless identity verification and direct benefit transfers, building trust in digital finance.

- Campaigns like ‘Mutual Funds Sahi Hai’, launched in 2017, demystified retail investing. The campaign seeks to help individuals from all backgrounds understand how consistent investments, especially through Systematic Investment Plans (SIPs), can build long-term wealth, even with small amounts.

- Platforms like Unified Payments Interface (UPI) and DigiLocker made onboarding and transactions frictionless, particularly for first-time savers.

Where Will the $9.5 Trillion Go?

Goldman Sachs estimates that more than $4 trillion of the total inflows will be directed toward long-term savings instruments such as insurance, pension schemes, and retirement funds. Equities and mutual funds are projected to receive robust inflows of approximately $0.8 trillion, while bank deposits are expected to attract around $3.5 trillion over the next decade.

This allocation reflects a more sophisticated and long-term investor mindset, with a growing tilt toward regulated, return-generating assets.

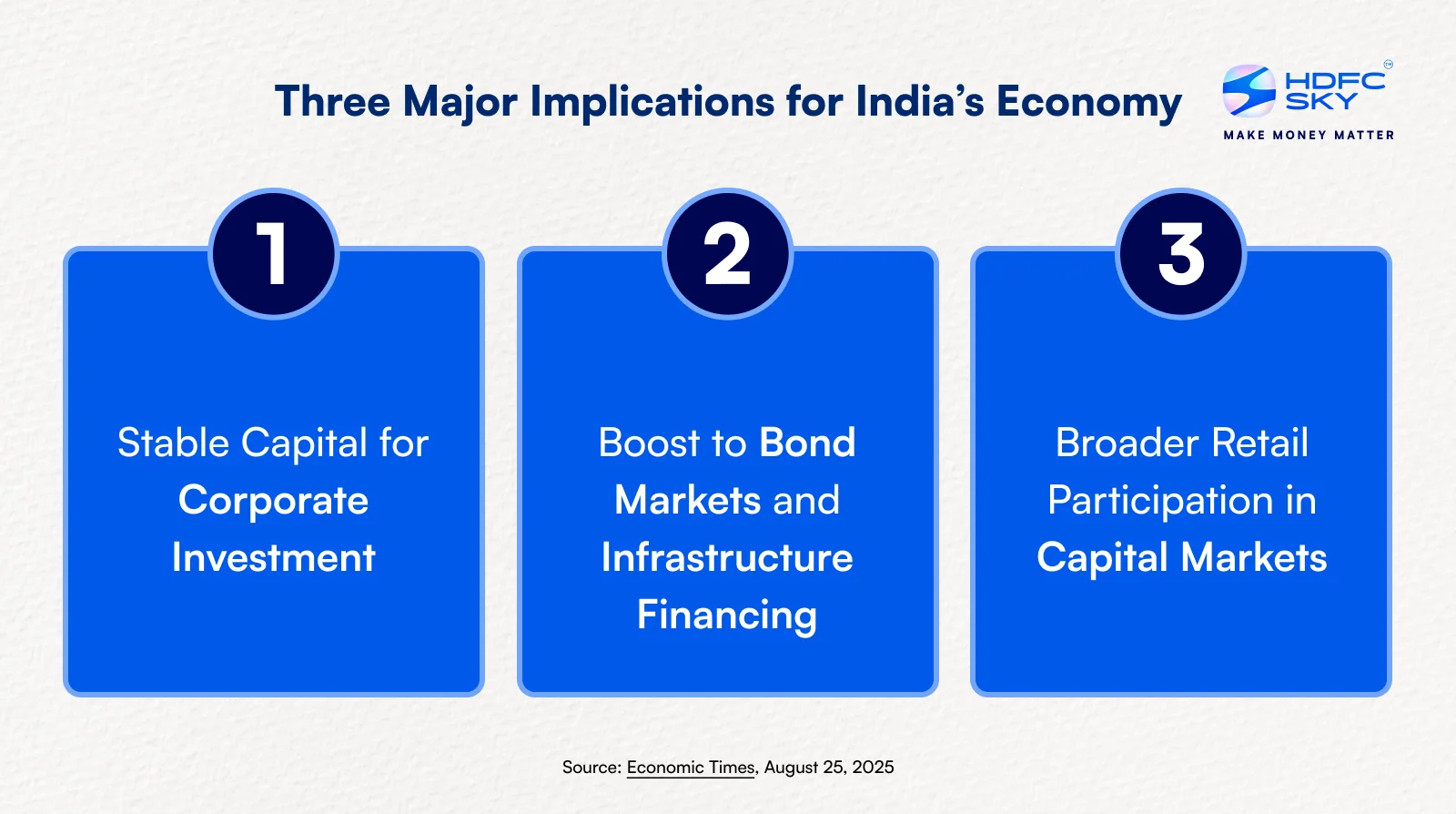

Three Major Implications for India’s Economy of $9.5 Trillion Inflows

Let’s understand these in detail.

1. Stable Capital for Corporate Investment

These domestic inflows can provide a reliable and long-term funding base for Indian corporates, reducing reliance on volatile foreign capital and limiting pressure on the current account deficit. This is especially crucial as India ramps up capital-intensive investments in infrastructure and manufacturing.

With a steady stream of household capital, companies can plan with greater confidence, access lower-cost financing, and insulate themselves from global liquidity shocks.

2. Boost to Bond Markets and Infrastructure Financing

Higher household allocations to insurance and pension funds will benefit the long-duration bond market, enabling longer-tenure corporate and sovereign bond issuances. This bodes well for infrastructure development, where long-dated financing is essential.

A robust domestic investor base for such bonds can lower borrowing costs, and improve fiscal planning for both government and private sector projects.

3. Broader Retail Participation in Capital Markets

As Indian families become more financially literate and connected through digital platforms, retail participation in equities, exchange-traded funds (ETFs), real estate investment trust (REITs), and other instruments will deepen. This could also accelerate the demand for wealth management services, financial advisors, and fintech solutions tailored for savings and investing. Greater retail involvement not only democratizes wealth creation but also reduces market concentration.

It marks a shift from passive saving to active financial planning, enabling households to play a more informed role in shaping India’s capital markets.

Why is this Shift Happening Now?

The move toward financial assets is being shaped by:

- Rising income levels

- Urbanization

- Wider access to digital financial platforms

- Tax incentives

With inflation stabilizing and interest rates offering reasonable returns, financial assets are becoming more attractive, especially when adjusted for liquidity, risk, and returns.

The convenience of low-ticket digital investing is drawing in first-time savers, particularly from younger and semi-urban demographics.

Final Word

If Goldman Sachs’ base-case projection holds, India’s household savings could emerge as a trillion-dollar tailwind for its financial system, fueling everything from capital markets to corporate capex and infrastructure bonds. In an era of deglobalization and rising interest rate uncertainty, this inward shift in capital sourcing could be India’s greatest structural advantage in the coming decade.

It would reduce reliance on volatile foreign inflows, deepen domestic financial markets, and provide the long-term funding backbone for India’s growth ambitions. As household savings become the economy’s silent workhorse, the next leap in India’s financial maturity may come not from global capital, but from its own middle class.

Disclaimer: At HDFC SKY, we take utmost care and due diligence in curating and presenting news and market-related content. However, inadvertent errors or omissions may occasionally occur.

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.

Please note that the information shared is intended solely for informational purposes and does not make any investment recommendations