The Income Tax Department is watching more closely than ever. With upgraded systems, AI-backed analytics, and tighter compliance norms, scrutiny has gone up, and so has the anxiety around income tax notices.

But here’s the truth: an income tax notice isn’t always a sign of wrongdoing. It could be something as simple as a mismatch in your bank interest or missing a form.

The important part is knowing what to do next.

Let’s take a deep dive into why notices are being sent more frequently, how you should respond, and how to stay off the radar in the future.

Why Are More People Getting ITR Notices In 2025?

The reason is very simple: the government aims to improve tax compliance without increasing tax rates.

For the Assessment Year (AY) 2026, the Income Tax Department has flagged close to 1.65 lakh cases for scrutiny, marking a surge nearly three to four times higher than the usual volume.

Out of these, more than one lakh taxpayers have already received notices under Section 143(2) of the Income Tax Act.

This particular section authorizes the department to thoroughly examine income tax returns if it suspects errors, mismatches, or financial red flags indicating potential risk.

To do that, they have launched several tools:

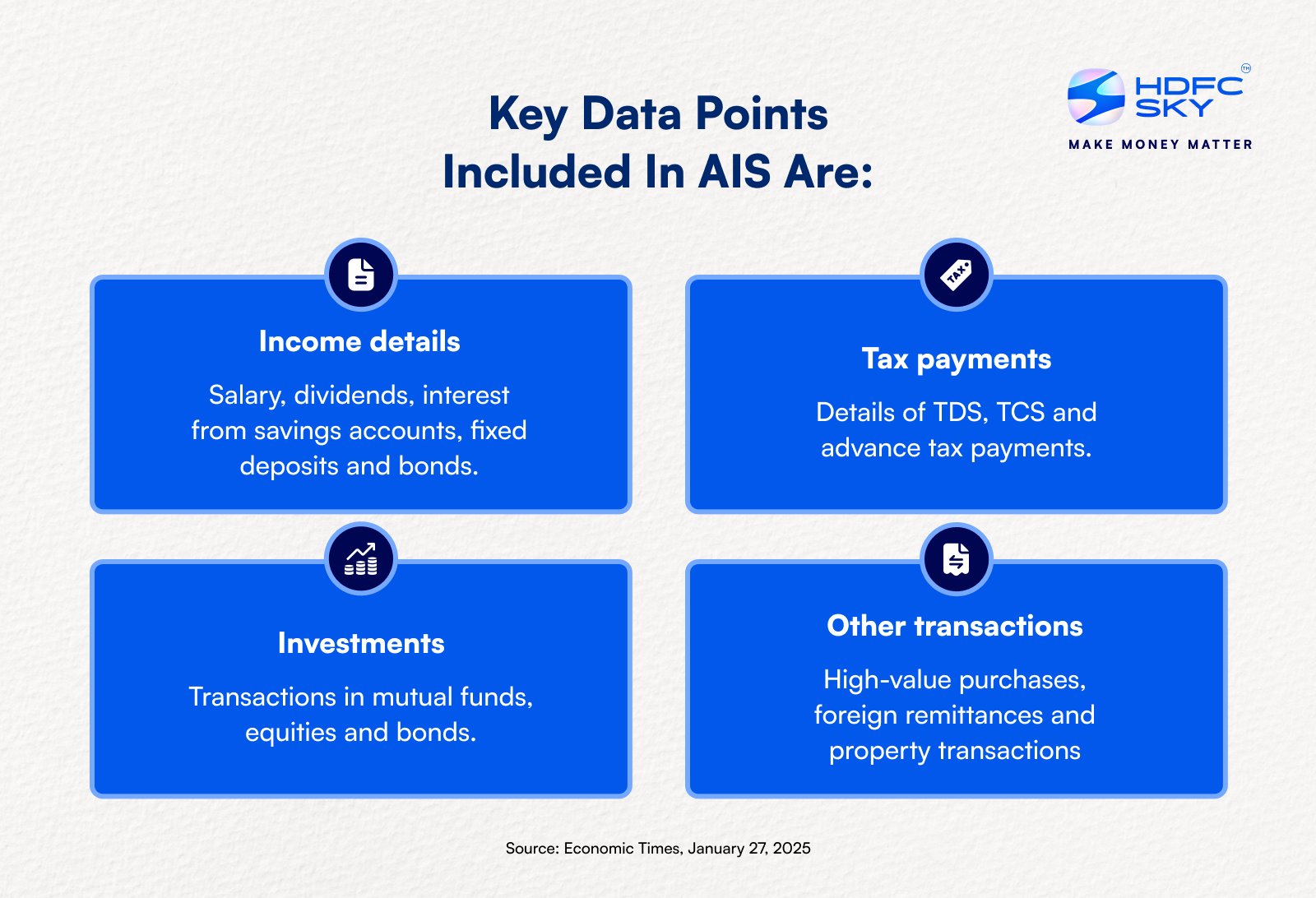

- Annual Information Statement (AIS): The Annual Information Statement (AIS) is an important initiative by the Income Tax Department, designed to give taxpayers a comprehensive summary of their financial activities during a given financial year. By pulling in data from banks, employers, and other financial institutions, it aims to enhance transparency and make tax filing more accurate and hassle-free.

- Taxpayer Information Summary (TIS): The Taxpayer Information Summary (TIS) presents a categorized information about an individual’s financial data. It includes both the system-generated figures, after eliminating duplicate entries, and the values confirmed or modified by the taxpayer.

System-generated figures refer to values automatically processed by the system after aggregating and removing duplicates from sources like Form 26AS, AIS, and TDS statements. Values accepted by the taxpayer refer to the final amounts the taxpayer confirms or adjusts in the TIS, which are then used to pre-fill the income tax return.

- Data-sharing between agencies: PAN-linked transactions are monitored across banks, brokerages, and registrar offices.

Real-Life Example: How Small Errors Trigger Notices

Let’s say you earned ₹90,000 interest from an FD but only reported ₹60,000. Or took freelance income or foreign consulting payments, but didn’t add them to your ITR. Or, sold mutual funds and had LTCG (Long-Term Capital Gains), but assumed it was exempt.

Each of these cases may trigger automated alerts.

The Income Tax Department uses a system called CASS (Computer Assisted Scrutiny Selection) to pick cases based on data and risk factors. Along with this, a newer tool called the Risk Management Strategy (RMS) helps spot people who didn’t file their income tax returns, even though they were supposed to (non-filers).

Using these methods, around 2.5 to 3 lakh cases have been identified for further review or investigation.

Types of Notices Explained

Section 142(1): Inquiry Before Assessment

- A notice under this section is sent to request specific details from the taxpayer, such as:

- Copies of books of accounts or relevant documents

- Any other written information asked for by the assessing officer

- This may also include details like statements of assets and liabilities, especially if they are already recorded in the accounts.

- If an assessee has not filed their Income Tax Return, the department may issue a notice directing them to do so within a stipulated time frame.

- Such a notice may also be served regardless of whether the return has already been filed or not.

- If the Assessing Officer finds the submitted details to be accurate and sufficient, they may decide not to proceed further with the assessment.

- It is important for the assessee to furnish the requested information, even if they believe it may not be directly relevant to the assessment process.

Time Limit for Response to Notice

The assessee must submit the return or provide the required information within the deadline specified in the notice.

Section 143(1): Intimation on Summary Assessment

Under the Income Tax Act, this communication is officially referred to as an ‘intimation’ rather than a ‘notice’. It is sent after the taxpayer has filed their return. If the assessing officer spots clear issues, such as:

- A calculation mistake in the return

- A claim that appears obviously incorrect

- Losses from previous financial years where the return was filed after the due date under Section 139(1). Section 139(1) of the Income Tax Act mandates every eligible person to file their income tax return within the prescribed due date for a financial year.

- Expenses disallowed in the Tax Audit Report but not reflected as disallowed in the income tax computation.

- Deductions claimed under Chapter VI-A or Section 10AA for a financial year where the return was submitted after the due date specified in Section 139(1).

Then, an intimation is issued to inform the taxpayer about these discrepancies.

Time Limit for Response to Notice

The assessee is required to respond to the intimation within 30 days from the date of its issuance. In the absence of a response within 30 days, the Assessing Officer may proceed based on the discrepancies identified in the intimation. This can lead to penal consequences under Section 271, or even prosecution under Section 276D, which may result in imprisonment.

Section 143(2): Notice on Scrutiny Assessment

This type of notice is sent when the taxpayer either hasn’t shared the required details or the assessing officer isn’t convinced by the information given.

It may ask for clarification on deductions and exemptions claimed, along with more details about how profits were calculated, allowing the officer to carry out a deeper investigation.

Time Limit for Response to Notice

The assessee must submit their response within the time frame specified in the notice.

Section 148: Notice on Income Escaping Assessment

In some cases, the assessee may have failed to report certain income in their return, and this omission might have gone unnoticed during the regular assessment. The Assessing Officer, upon discovering such information later, is empowered to reassess the income for that specific financial year.

Additionally, if no prior assessment was carried out on the return and the time limit under Section 143 has lapsed, the Assessing Officer still holds the authority to reopen the return and initiate assessment proceedings.

Time Limit for Response to Notice

Under Section 148, the Assessing Officer directs the assessee to file a return of income within three months from the end of the month in which the notice is issued. If the assessee fails to comply within the prescribed time, the Assessing Officer may proceed with a Best Judgment Assessment under Section 144.

However, the assessee may seek relaxation of the time limit by submitting a request to the CBDT under Section 119(2). In certain cases, the Assessing Officer may also grant a time extension at their discretion.

Note that every notice clearly states a response window.

It is always important to check your email and SMS alerts from the Income Tax Department or log into the e-filing portal regularly during tax season.

Ignoring notices may lead to:

- Penalties

- Interest charges

Common Mistakes To Avoid While Responding

- Submitting incomplete documentation

- Uploading the wrong financial year’s data

- Trying to ‘explain’ without supporting evidence

Every claim must be backed by clear documents. If the scrutiny is high-level, keep your paperwork neat, organized, and ideally signed by a tax consultant.

Do Notices Always Mean Tax Payable?

Not necessarily. Sometimes, they’re just asking for clarification. If your response satisfies the department, the case gets closed.

The good news is that as long as you’re cooperative and transparent, the system is designed to be fair.

Preventive Tips For The Future

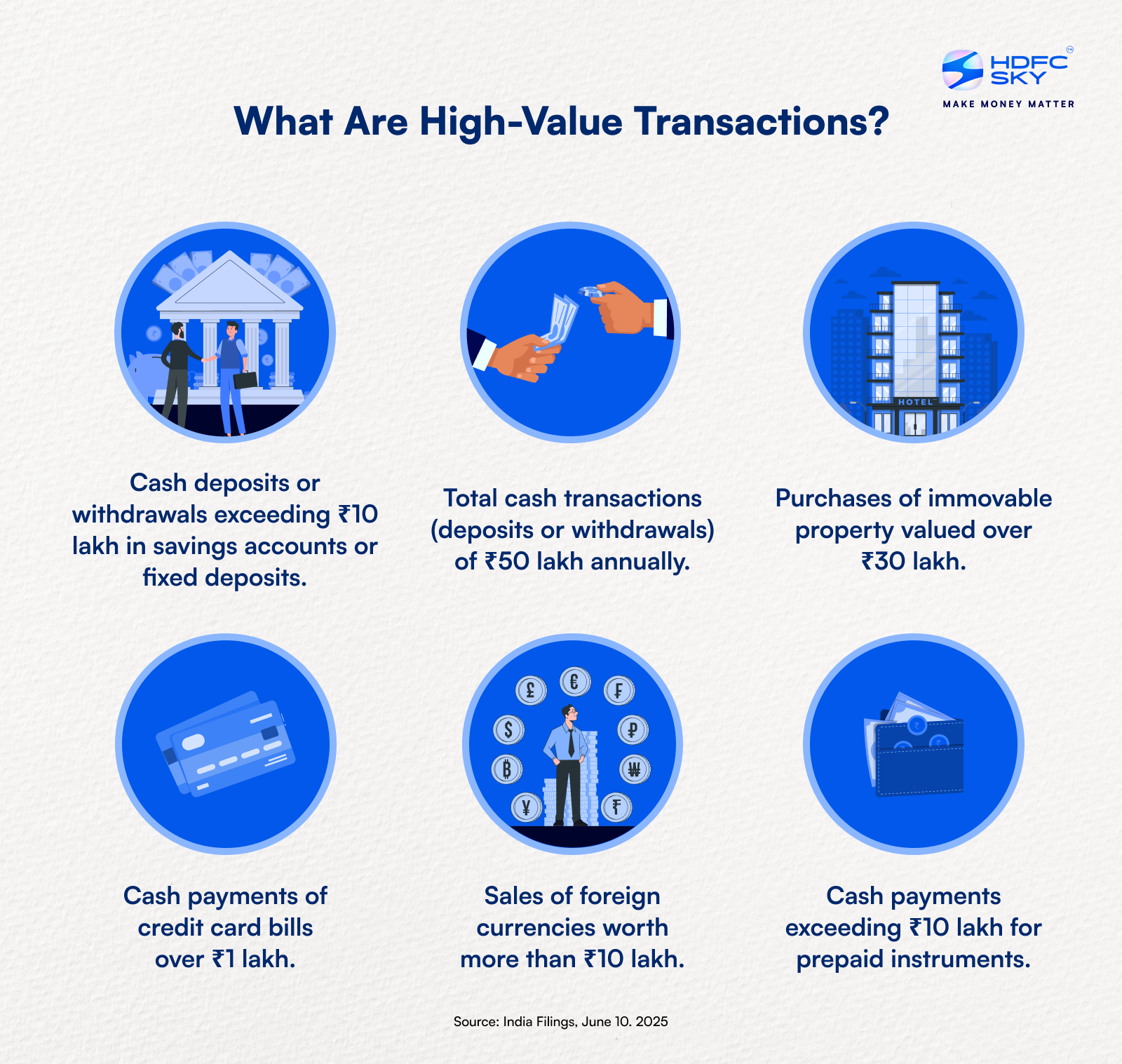

1. Report High-Value Transactions: Make sure to report all major financial transactions to the Income Tax Department accurately and on time.

2. Accurate Disclosures in ITR: Make sure your Income Tax Return covers all necessary details and disclosures as required by law.

3. Maintain Accurate Records: Maintain clear and well-organized records of all your financial transactions and documents.

4. File ITR Early: Don’t delay filing your tax return. Submitting it early helps reduce mistakes and prevents last-minute stress.

5. Accurate Income and Deductions: Always report your income accurately and avoid overstating deductions or expenses. Being truthful in your financial declarations helps you steer clear of unnecessary scrutiny

6. Verify Your Tax Payments: Make sure the taxes you’ve reported match the entries in Form 26AS. This form shows all the tax deducted at source (TDS) or tax collected at source (TCS) from your different income sources.

Final Thoughts

Today’s tax system is more transparent and tech-savvy than ever. If you’ve filed your ITR with honesty and attention to detail, there’s little to worry about.

And if a notice does land in your inbox?

Respond smartly, keep your documentation ready, and don’t hesitate to seek help.

Think of it as a checkpoint. After all, in a digital economy, financial hygiene matters as much as financial growth.

Disclaimer: At HDFC SKY, we take utmost care and due diligence in curating and presenting news and market-related content. However, inadvertent errors or omissions may occasionally occur.

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.

Please note that the information shared is intended solely for informational purposes and does not make any investment recommendations