NSE and Jio Eye Blockbuster Listings; Lessons Linger from Paytm, LIC and Reliance Power

Authored By HDFC SKY | Last Modified: Jun 19, 2026 12:38 PM IST

Mumbai, June 19: As India prepares for what could be its biggest-ever wave of public offerings, investors are once again gripped by IPO fever.

The National Stock Exchange (NSE), India’s largest bourse, has filed for a long-awaited listing that could raise more than $3 billion, while billionaire Mukesh Ambani’s telecom-to-digital giant Jio Platforms is expected to launch an offering worth about $4 billion. Together, they are poised to rank among the largest IPOs in Indian corporate history and could reignite enthusiasm in the primary market.

Yet history offers a cautionary tale.

Some of India’s most glamorous IPOs—backed by powerful brands, celebrity promoters and massive investor demand—have gone on to become cautionary examples of how hype and valuation can overwhelm fundamentals. From Reliance Power’s spectacular collapse in 2008 to Paytm’s record-breaking flop in 2021, investors have repeatedly learned that a blockbuster IPO does not guarantee blockbuster returns.

The Original Sin: Reliance Power

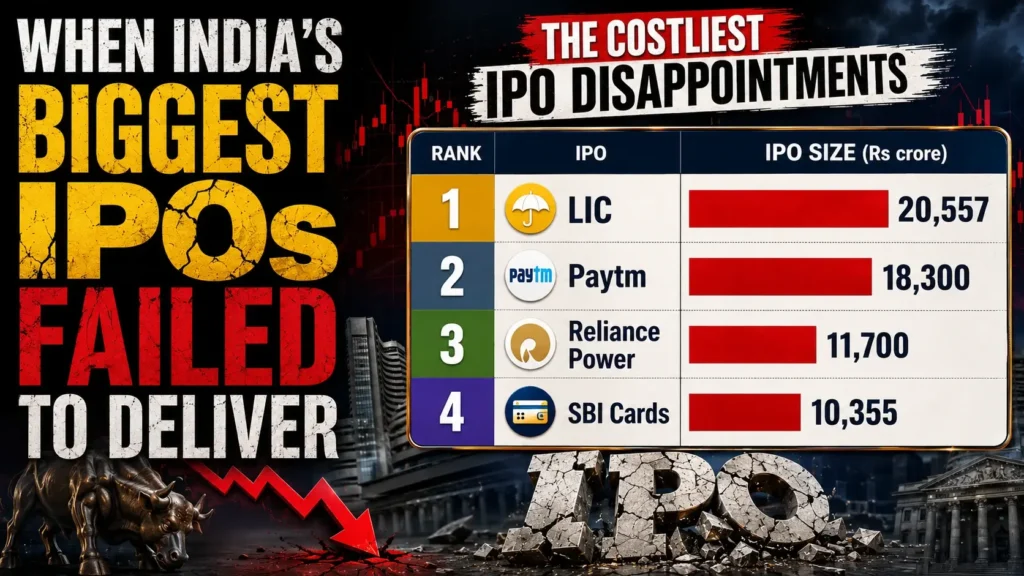

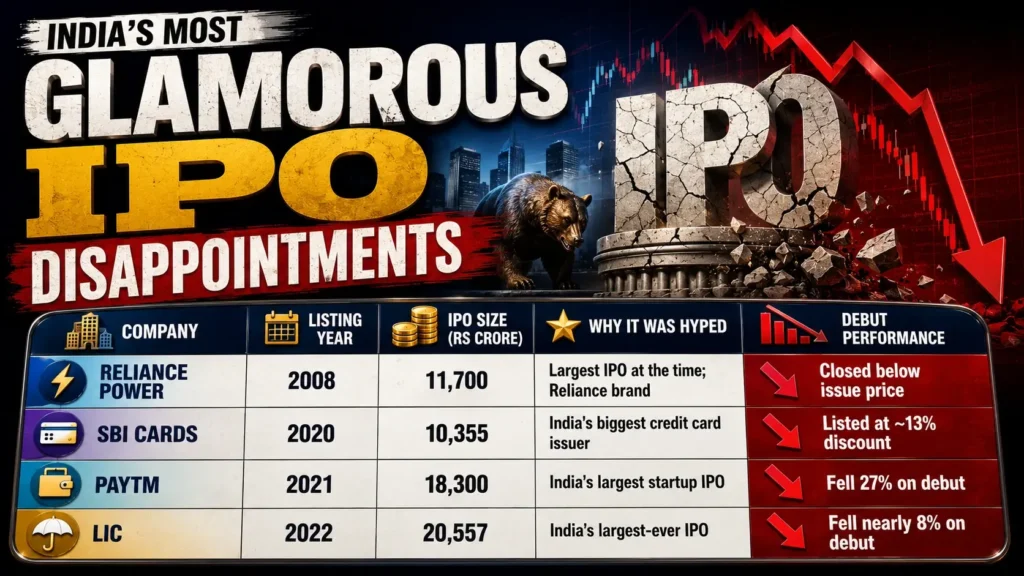

No discussion of disappointing IPOs in India begins anywhere other than Reliance Power.

Launched during the peak of the 2007-08 bull market, the company was promoted by Anil Ambani at a time when the Reliance name carried near-mythical appeal among retail investors. The IPO attracted unprecedented demand and became the largest public issue in India at the time.

Also Read: NSE IPO: What It Means For Investors

There was just one problem: the company had virtually no operating assets generating revenue.

Investors were effectively buying a promise of future power projects. When the stock debuted in February 2008, the market quickly questioned the lofty valuation attached to those promises. Shares slumped below the issue price almost immediately and never recovered their early aura.

For an entire generation of retail investors, Reliance Power became synonymous with IPO hype gone wrong. It demonstrated that even the most powerful brand in Indian business could not justify an excessive valuation indefinitely.

Paytm: India’s Biggest IPO Becomes Its Biggest IPO Shock

More than a decade later, another IPO captured the imagination of investors.

Digital payments giant Paytm arrived on the market in November 2021 after raising $2.5 billion in what was then India’s largest-ever IPO. The company embodied the country’s startup boom, backed by SoftBank, Ant Group and a narrative that digital payments would transform India’s economy. The issue was oversubscribed and priced at the top end of its range despite widespread concerns about valuation.

Those concerns proved prescient.

On its first day of trading, Paytm plunged 27%, wiping billions of dollars off its market value and becoming one of the worst debuts for a major Indian listing. Investors questioned whether the company could ever generate sufficient profits to justify its valuation.

The listing became a watershed moment for India’s startup ecosystem. Public-market investors made it clear that they would no longer reward growth at any cost. Revenue growth and customer acquisition were no longer enough; profitability mattered.

LIC: The IPO Everyone Wanted

If Paytm was a bet on India’s digital future, Life Insurance Corporation of India represented the country’s financial past.

The government’s decision to list LIC in 2022 was billed as a once-in-a-generation event. Millions of policyholders applied. Retail investors viewed the insurer as one of India’s most trusted institutions. The IPO raised more than ₹20,500 crore, making it India’s largest public offering at the time.

But the listing arrived amid a global market selloff, rising inflation and concerns about economic growth.

LIC shares opened well below the issue price and ended their debut session nearly 8% lower, stunning investors who had expected a strong listing from a household name that dominated India’s insurance industry.

The disappointment was particularly acute because many first-time investors had participated purely because of LIC’s reputation. The episode underscored a harsh market reality: even dominant businesses can produce poor shareholder returns if they are listed at the wrong time or valuation.

SBI Cards: The IPO That Met a Pandemic

Sometimes, timing is everything.

SBI Cards and Payment Services entered the market in March 2020 amid enormous anticipation. Backed by State Bank of India and operating in one of the country’s fastest-growing consumer-finance segments, the company was viewed as one of the most attractive financial-sector listings in years.

Then COVID-19 happened.

As global markets plunged, SBI Cards debuted at a discount of more than 12% to its issue price. Concerns over consumer spending, loan defaults and economic disruption overshadowed what many analysts considered a strong underlying business.

Unlike some IPO disappointments, SBI Cards’ weak debut was driven less by valuation concerns and more by one of the worst market environments in modern history.

Why Glamorous IPOs Often Disappoint

These offerings were very different businesses operating in different sectors and economic environments. Yet they shared several common characteristics.

First, they arrived with extraordinary media attention. Investors were not merely buying shares; they were buying stories.

Second, valuations often reflected future expectations rather than current earnings. In many cases, years of projected growth were already embedded in the offer price.

Third, retail participation surged because investors feared missing out on the next big success story.

Finally, the IPO often represented a liquidity event for existing shareholders. By the time public investors gained access, private investors had already enjoyed years of value creation.

The result was a familiar pattern: expectations climbed faster than fundamentals.

The Jio and NSE Test

That history is particularly relevant as investors prepare for the potential listings of Jio and NSE.

Unlike many past IPO disappointments, both companies have clear advantages. NSE dominates India’s exchange industry and is the world’s largest derivatives exchange by contract volume, while Jio transformed India’s telecom market and sits at the centre of Reliance Industries’ digital ambitions.

Investor excitement is already building, with market participants describing the offerings as potential record-breakers.

But if the lessons of Reliance Power, Paytm, LIC and SBI Cards have taught investors anything, it is that glamour alone is not enough.

The most important question is not whether Jio and NSE are great companies.

It is whether they are great investments at the price investors are ultimately asked to pay.

As India’s IPO machine gears up for another historic chapter, that distinction may prove more important than ever.

Source:

- market data

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.

Please Note: The information shared is intended solely for informational purposes and does not make any investment recommendations