Tata Consultancy Services Shares Climb 4% As Q1 Earnings Exceed Estimates

Authored By HDFC SKY | Published at: Jul 10, 2026 03:04 PM IST

Mumbai, July 10: Tata Consultancy Services (TCS) share price rallied on Friday after the IT major reported better-than-expected June-quarter earnings, with investors taking comfort from resilient revenue growth, strong deal wins and management’s optimistic commentary on demand recovery. The stock rose as much as 4%, lifting the broader Nifty IT index as analysts said the results suggested that the worst of the slowdown in discretionary technology spending may be over, even though the sector continues to face macroeconomic headwinds.

TCS reported a 5% year-on-year rise in consolidated net profit to ₹13,349 crore, while revenue increased 14% to ₹72,275 crore during the April-June quarter. The company also maintained healthy order inflows, reinforcing confidence in its long-term growth outlook. As of writing the stock was up 1.1% at Rs 2,072.70.

Brokerages remain constructive

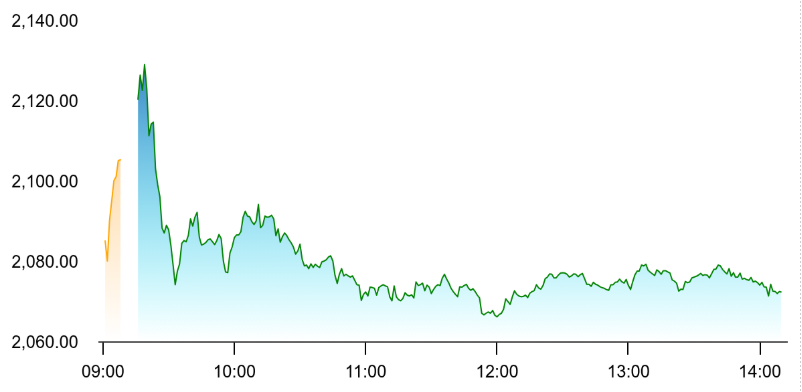

The stock cheered up after its report card. Source: NSE

Global and domestic brokerages broadly retained their positive stance on the stock after the earnings announcement, although many maintained that the recovery in the broader IT services sector is likely to be gradual.

The brokers reiterated ‘Overweight’ rating, saying TCS delivered a better-than-feared quarter despite a challenging macro environment. They highlighted the company’s resilient execution, healthy deal pipeline and encouraging management commentary on demand trends, while noting that an improvement in discretionary spending could support growth over the coming quarters.

They stated that TCS’s results reinforced its position as one of the best-placed players in the sector, pointing to robust deal wins and improving business momentum, and cautioning that a broad-based recovery in client technology spending is still evolving.

Several other brokerages retained their existing recommendations, arguing that while near-term growth may remain moderate, TCS continues to stand out because of its diversified client base, strong balance sheet and industry-leading execution capabilities.

AI momentum continues to strengthen

One of the biggest takeaways from the earnings announcement was the company’s growing artificial intelligence business.

TCS said its annualised AI revenue increased to $2.6 billion, up from $2.3 billion in the previous quarter, reflecting rising enterprise adoption of AI-led transformation projects. Clients continue to prioritise investments in generative AI, cloud modernisation and automation despite lingering macroeconomic uncertainty.

Chief Executive K Krithivasan also indicated that demand conditions were improving in sectors such as manufacturing and life sciences, while expressing confidence that business activity would strengthen further during the second quarter. Analysts said the AI pipeline remains a key long-term growth driver, although meaningful financial benefits from large-scale AI adoption are likely to accrue gradually rather than immediately.

Deal wins and demand outlook remain key positives

Brokerages also highlighted TCS’s strong order book as a key positive, saying it provides healthy revenue visibility despite persistent macro uncertainties.

The company reported a total contract value (TCV) of $9.5 billion during the quarter, reflecting continued client demand for digital transformation projects. Analysts believe this should support revenue growth once discretionary spending by global clients begins to recover more meaningfully.

While some verticals continue to witness cautious client spending, financial services remained resilient and contributed to the company’s better-than-expected performance during the quarter. A weaker rupee also provided some support to reported earnings.

Sector sentiment improves

TCS’s earnings helped improve sentiment across the IT sector, with shares of Infosys, Wipro, HCLTech and Tech Mahindra also advancing as investors interpreted the results as an encouraging signal ahead of the rest of the earnings season.

Analysts said TCS’s performance suggests that demand has stabilised after several quarters of subdued discretionary spending. However, they cautioned that the broader recovery is likely to remain uneven, with clients continuing to scrutinise technology budgets amid global economic uncertainty.

For investors, the focus will now shift to upcoming quarterly results from other large IT companies to assess whether TCS’s resilience reflects a broader sector-wide improvement. Management commentary on deal pipelines, AI-related opportunities and client spending trends is expected to be closely watched as markets look for confirmation that India’s $280-billion IT services industry is entering a more sustained recovery phase.

Source:

- https://www.nseindia.com/get-quote/equity/TCS/Tata-Consultancy-Services-Limited

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.

Please Note: The information shared is intended solely for informational purposes and does not make any investment recommendations