Nifty 50

- Trent₹2,928.9086.50 (3.04%)

- Axis Bank₹1,257-71.50 (-5.38%)

- Power Grid Corp₹289.105.55 (1.96%)

- HDFC Bank₹778-41.60 (-5.08%)

- Nestle₹1,45325.80 (1.81%)

- Kotak Mahindra Bank₹381.70-8.25 (-2.12%)

- NTPC₹347.505.65 (1.65%)

- Maruti Suzuki₹13,519-284.00 (-2.06%)

- Bharti Airtel₹1,939.9031.10 (1.63%)

- Jio Financial ₹239.10-3.88 (-1.60%)

- SBI₹1,060.6016.30 (1.56%)

- TCS₹2,251-18.00 (-0.79%)

- UltraTech Cement₹11,900173.00 (1.48%)

- Infosys₹1,087.90-8.60 (-0.78%)

- JSW Steel₹1,255.5018.20 (1.47%)

- Mahindra & Mahindra₹3,166-13.20 (-0.42%)

- Max Healthcare₹1,104.7014.80 (1.36%)

- Reliance Industries₹1,321.90-5.30 (-0.40%)

- HCL Technologies₹1,22016.10 (1.34%)

- InterGlobe Aviation₹5,233.50-15.00 (-0.29%)

- Offerings

- Tools & Platforms

Tools & Calculators

- Open API

- Calculators

- SIP Calculator

- CAGR Calculator

- Compound Interest Calculator

- FD Calculator

- RD Calculator

- EPF Calculator

- Retirement Calculator

- HDFC SIP Calculator

- Mutual Fund Return Calculator

- Lumpsum Calculator

- Step Up SIP Calculator

- ETF SIP Calculator

- Brokerage Calculator

- Equity Margin Calculator

- SWP Calculator

- EMI Calculator

- MTF Calculator

- Margin Pledge Calculator

- Markets

Stocks

F&O

Mutual Funds

- More

The 3-Bucket Portfolio Strategy That Wealthy Indian Families Use to Manage Generational Wealth

By Aseem Shrivastava | Published at: Jun 4, 2026 01:13 PM IST

Wealthy Indian families don’t really approach investing as a collection of products. They tend to keep things more organized than that. Money is first given a clear purpose, and only then is it invested. That simple mindset is what sits behind the 3-bucket portfolio approach, even if they don’t always call it that.

It is one of the simplest ways they manage wealth across generations without losing balance between safety and growth.

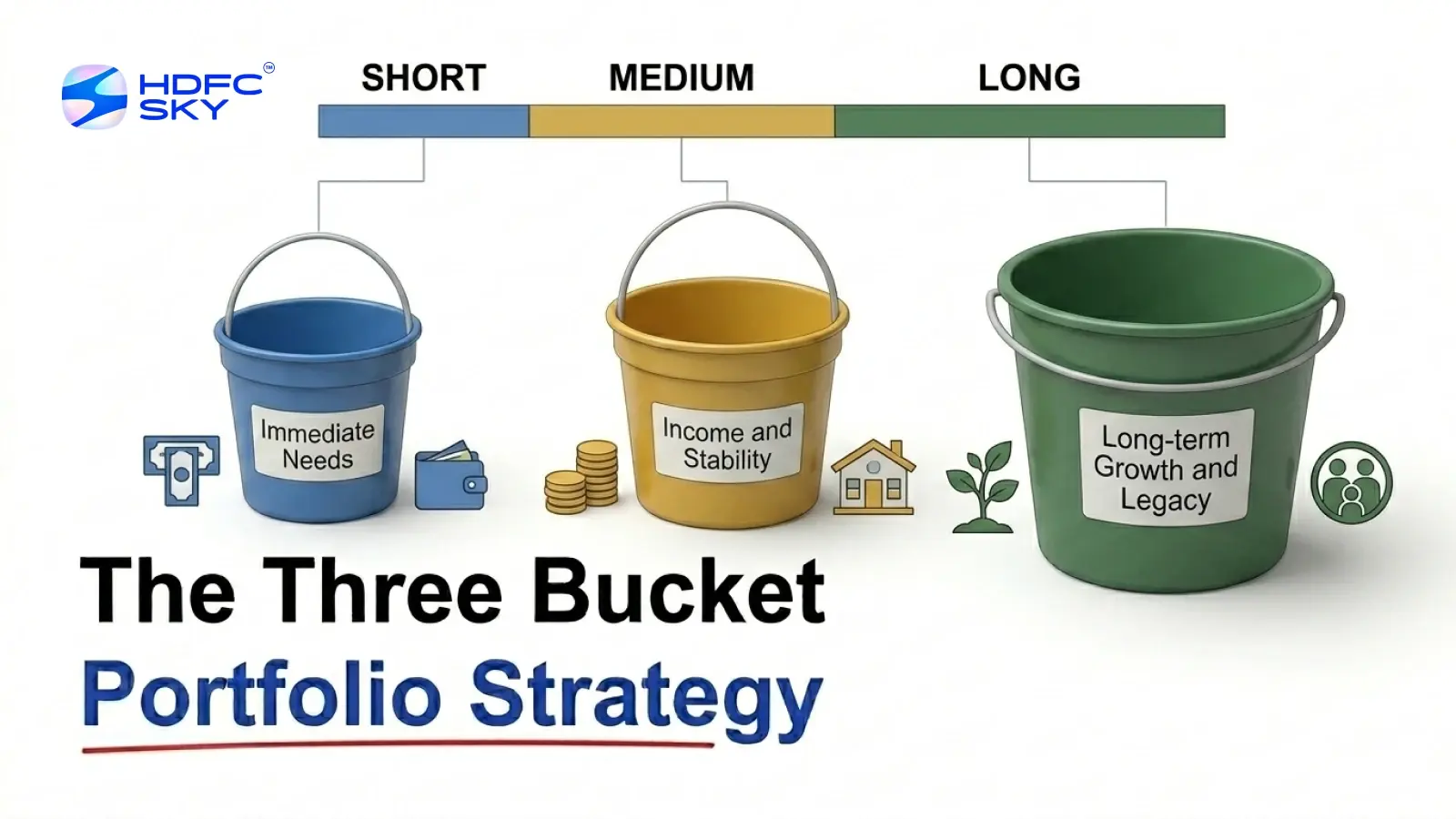

A Simple Way to Organize Wealth

Instead of pooling all investments together, wealth is divided into three buckets based on time horizon and financial goals. Each bucket serves a distinct purpose.

Bucket 1: Immediate Needs

This bucket focuses on liquidity and accessibility. It includes emergency funds and short-term expenses. Investments typically consist of cash, savings accounts, or liquid funds, where safety is prioritized over returns.

Bucket 2: Income and Stability

This bucket balances risk and return. It supports planned expenses and provides consistent income. Common instruments include debt funds, conservative hybrid funds, and other low-volatility investments.

Bucket 3: Long-term Growth and Legacy

This bucket is designed for long-term wealth creation. Investments such as equities, index funds, and other growth-oriented assets are held for extended periods, often decades, to benefit from compounding.

Also Read: How HNIs are using sovereign gold bonds instead of physical gold and its tax reason

Why This Structure Works

The biggest advantage of this approach is clarity. Each portion of wealth has a defined role, which reduces emotional decision-making during market fluctuations.

How to Get Started

Start by dividing your money based on time horizons:

- Allocate funds for short-term needs separately

- Invest a portion in stable, income-generating instruments

- Keep long-term investments untouched to allow growth

The structure may not feel perfect initially, but clarity improves as you consistently follow the approach.

By signing up I certify terms, conditions & privacy policy