Nifty 50

- SBI Life Insurance ₹1,843.8056.10 (3.14%)

- Trent₹2,968.90-374.90 (-11.21%)

- Titan Company₹4,623138.60 (3.09%)

- Coal India₹424.90-7.45 (-1.72%)

- Infosys₹1,070.1027.90 (2.68%)

- L&T₹3,980-61.00 (-1.51%)

- Tech Mahindra₹1,440.7034.20 (2.43%)

- Adani Enterprises₹3,164.90-41.70 (-1.30%)

- TCS₹2,10042.40 (2.06%)

- Bharat Electronics₹420.75-4.80 (-1.13%)

- HCL Technologies₹1,152.6018.40 (1.62%)

- Hindalco Industries₹970.05-10.35 (-1.06%)

- Eicher Motors₹7,586114.50 (1.53%)

- NTPC₹353.20-3.05 (-0.86%)

- Eternal₹287.704.30 (1.52%)

- InterGlobe Aviation₹5,367.50-41.00 (-0.76%)

- Jio Financial ₹243.013.01 (1.25%)

- Grasim Industries₹3,193.80-19.20 (-0.60%)

- Shriram Finance₹1,07411.70 (1.10%)

- Cipla₹1,463.60-8.70 (-0.59%)

- Offerings

- Tools & Platforms

Tools & Calculators

- Open API

- Calculators

- SIP Calculator

- CAGR Calculator

- Compound Interest Calculator

- FD Calculator

- RD Calculator

- EPF Calculator

- Retirement Calculator

- HDFC SIP Calculator

- Mutual Fund Return Calculator

- Lumpsum Calculator

- Step Up SIP Calculator

- ETF SIP Calculator

- Brokerage Calculator

- Equity Margin Calculator

- SWP Calculator

- EMI Calculator

- MTF Calculator

- Margin Pledge Calculator

- Markets

Stocks

F&O

Mutual Funds

- More

InCred Holdings Limited IPO

TBA/TBA shares

Minimum Investment

IPO Details

TBA

TBA

₹TBA

TBA

₹TBA to TBA

NSE, BSE

₹TBA Cr

TBA

InCred Holdings Limited IPO Timeline

Bidding Start

TBA

Bidding Ends

TBA

Allotment Finalisation

TBA

Refund Initiation

TBA

Demat Transfer

TBA

Listing

TBA

Explore IPO Opportunities

Explore our comprehensive IPO pages to stay updated on the latest trends and insights.

InCred Holdings Limited IPO

IPO Details

- Open date: TBA

- Close Date: TBA

- Minimum Investment: To be updated

- Lot Size: TBA

- Price Range: TBA

- Listing: BSE, NSE

- Issue Size: Fresh Issue of ₹1,250 crore + OFS of up to 9.90 crore equity shares

- Listing Date: TBA

IPO Timeline

- Bidding Start: TBA

- Bidding Ends: TBA

- Allotment Finalisation: TBA

- Refund Initiation: TBA

- Demat Transfer: TBA

- Listing: TBA

About InCred Holdings Limited

Incorporated in January 2011, InCred Holdings Limited is a diversified financial services company engaged in merchant banking, debt syndication, debt advisory, corporate consultancy, fund-raising, and investment management services. The company is registered as a Merchant Banker with SEBI and operates primarily through its material subsidiary, InCred Financial Services Limited (IFSL), a retail-focused, middle-layer NBFC registered with the Reserve Bank of India. Founded by Bhupinder Singh in 2017, InCred offers a diversified lending portfolio across Personal Loans, Student Loans, Secured Business Loans, Specialised MSME Loans, and Lending to Financial Institutions. With a technology-driven platform, robust risk management framework, and multi-channel distribution network, the company serves underserved borrower segments across India.

InCred Holdings Limited IPO Overview

InCred Holdings Limited’s initial public offering is a book-built issue comprising a fresh issue of up to ₹1,250 crore and an offer for sale of up to 9.90 crore equity shares by existing shareholders including KKR India Financial Investments, MNI Ventures, MEMG Family Office LLP, and V’Ocean Investments. The company filed its DRHP confidentially in November 2025 and received SEBI approval on February 5, 2026. The equity shares are proposed to be listed on BSE and NSE. IIFL Capital Services, InCred Capital Wealth Portfolio Managers, Kotak Mahindra Capital, Nomura Financial Advisory, and UBS Securities India are the book-running lead managers. The net proceeds from the fresh issue will be utilized primarily for investment in its wholly owned subsidiary, InCred Finance, to strengthen its tier-I capital base, support onward lending activities, and improve capital adequacy. The company’s shareholding pre-issue stands at 65,59,44,906 equity shares.

InCred Holdings Limited Upcoming IPO Details

|

Category |

Details |

|

Issue Type |

Book Built Issue IPO |

|

Total Issue Size |

Fresh Issue of ₹1,250 crore + OFS of up to 9.90 crore equity shares |

|

Fresh Issue |

[●] shares (aggregating up to ₹1,250 crore) |

|

Offer for Sale (OFS) |

9,90,20,833 shares (aggregating up to ₹[●] crore) |

|

IPO Dates |

TBA |

|

Price Bands |

TBA |

|

Lot Size |

TBA |

|

Face Value |

₹10 per share |

|

Listing Exchange |

BSE, NSE |

|

Shareholding pre-issue |

65,59,44,906 shares |

|

Shareholding post-issue |

To be updated |

InCred Holdings Limited IPO Lots

|

Lots |

Shares |

Amount |

|

|

Retail (Min) |

TBA |

TBA |

TBA |

|

Retail (Max) |

TBA |

TBA |

TBA |

|

S-HNI (Min) |

TBA |

TBA |

TBA |

|

S-HNI (Max) |

TBA |

TBA |

TBA |

|

B-HNI (Min) |

TBA |

TBA |

TBA |

InCred Holdings Limited IPO Reservation

|

Shares Offered |

|

|

QIB Shares Offered |

Not more than 50% of the Offer |

|

Retail Shares Offered |

Not less than 35% of the Offer |

|

NII (HNI) Shares Offered |

Not less than 15% of the Offer |

InCred Holdings Limited IPO Valuation Overview

|

KPI |

Value |

|

Earnings Per Share (EPS) |

₹ |

|

Price/Earnings (P/E) Ratio |

TBD |

|

Return on Net Worth (RoNW) |

|

|

Net Asset Value (NAV) |

₹ |

|

Return on Equity (RoE) |

|

|

Return on Capital Employed (RoCE) |

|

|

EBITDA Margin |

|

|

PAT Margin |

|

|

Debt to Equity Ratio |

|

Objectives of the IPO Proceeds

The Net Proceeds are intended to be utilized as per the details provided in the table below:

|

Particulars |

Amount (in ₹ million) |

|

Investment in wholly owned subsidiary InCred Finance to strengthen Tier-I capital base |

Up to 12,500 |

|

Support onward lending activities and improve capital adequacy |

— |

|

General corporate purposes* |

[●] |

*To be determined upon finalisation of the Offer Price and updated in the Prospectus prior to filing with the RoC. The company plans to use the fresh issue proceeds mainly to strengthen the capital base of its subsidiary, InCred Financial Services.

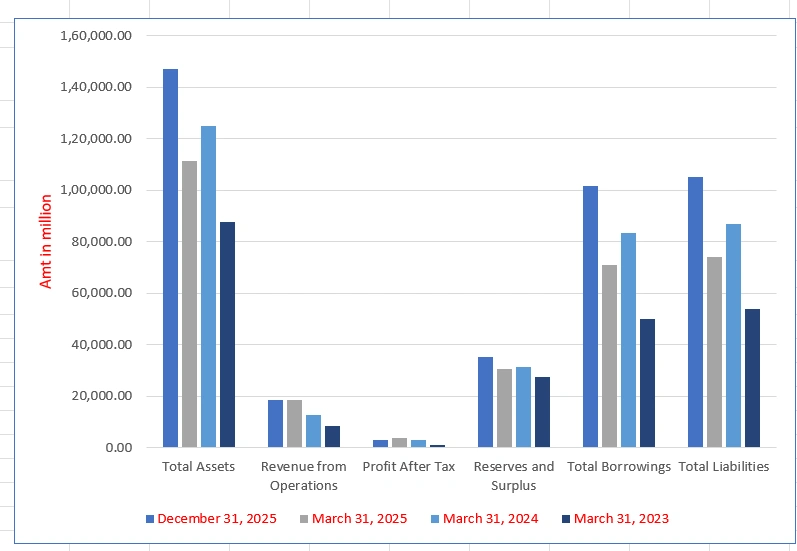

InCred Holdings Limited Financials (₹ in Million)

|

Particulars |

December 31, 2025 |

March 31, 2025 |

March 31, 2024 |

March 31, 2023 |

|

Total Assets |

147,163.09 |

111,259.61 |

125,005.29 |

87,676.18 |

|

Revenue from Operations |

18,489.42 |

18,736.21 |

12,727.01 |

8,656.51 |

|

Profit After Tax |

2,901.45 |

3,731.50 |

3,090.39 |

1,090.64 |

|

Reserves and Surplus |

35,467.56 |

30,595.40 |

31,557.48 |

27,449.55 |

|

Total Borrowings |

101,637.64 |

70,973.12 |

83,585.10 |

50,171.54 |

|

Total Liabilities |

105,138.66 |

74,190.90 |

86,972.64 |

53,808.45 |

Financial Status of InCred Holdings Limited

SWOT Analysis of InCred Holdings Limited

|

Strengths and Opportunities |

Weaknesses and Threats |

|

Retail-focused lending franchise with diversified product portfolio |

Concentration risk with personal loans at 55.56% of AUM |

|

Fastest PAT growth (85% CAGR) among diversified NBFC peers |

Intense competition from banks and established NBFCs |

|

Strong AUM growth at 44% CAGR between FY23 and FY25 |

Regulatory changes affecting NBFC sector |

|

Risk-first approach resulting in healthy asset quality (Net Stage 3: 0.87%) |

Rising interest rates impacting borrowing costs |

|

Proprietary AI-enabled technology platform across customer value chain |

Asset quality pressures in unsecured lending segments |

|

Multi-channel distribution network with 158 branches across 19 states |

Macroeconomic slowdown affecting borrower repayment capacity |

|

Experienced management team backed by marquee investors like KKR |

Technology and cyber security risks |

|

Robust funding profile with AA-/Stable credit rating |

Dependence on wholesale funding sources |

|

India’s NBFC credit growing at 16.7% YoY in FY26 |

Execution risks in scaling new product verticals |

|

Personal loan segment growing at 16.2% in FY26 |

Geopolitical and economic uncertainty |

InCred Holdings Limited IPO Strengths

Retail-Focused Lending Franchise with Diversified Product Portfolio

InCred Holdings Limited has built a robust retail-focused lending franchise with a diversified portfolio spanning five key verticals: Personal Loans (55.56% of AUM), Student Loans (22.15%), Secured Business Loans including Loan Against Property and school financing (8.74%), Specialised MSME Loans (7.83%), and Lending to Financial Institutions (5.55%). This diversification reduces concentration risk and enables the company to capture opportunities across multiple high-growth lending segments, serving underserved borrower segments often overlooked by traditional banks.

Strong Growth in AUM and Profitability Across Lending Segments

InCred Holdings has demonstrated exceptional financial performance, with AUM and PAT growing at a CAGR of 44.04% and 84.97%, respectively, between FY23 and FY25. The company was recognized by CRISIL as the fastest-growing diversified NBFC in India in terms of PAT CAGR and the second-fastest in AUM CAGR among diversified peers. As of December 31, 2025, AUM stood at ₹14,447.86 crore, reflecting the company’s ability to scale operations profitably across multiple lending segments.

Risk-First Approach Resulting in Healthy Asset Quality

InCred Holdings follows a disciplined “risk-first” lending philosophy supported by an AI-enabled proprietary technology platform. This approach has resulted in healthy asset quality with Gross Stage 3 loans at 2.28% and Net Stage 3 loans at 0.87% as of December 31, 2025. The company reported a credit cost of 1.74% for Fiscal 2025, the second-lowest among diversified peers, demonstrating superior risk management capabilities.

Proprietary AI-Enabled Technology Platform Across the Customer Value Chain

InCred Holdings has developed an in-house, AI-enabled proprietary technology platform that manages the entire lending lifecycle from origination and credit assessment to ongoing account management and collections. The company’s “InCred” mobile app had over 4.5 lakh users as of December 2025. The technology team grew from 114 professionals in FY23 to 152 as of December 31, 2025, reflecting continuous investment in technology capabilities.

Extensive Multi-Channel Distribution Network and Customer Reach

InCred Holdings has built a multi-channel distribution network with 158 branches across 152 cities in 19 states and union territories, covering more than 17,000 pin codes. The distribution network includes direct sourcing through the mobile application and website, channel partners, educational consultants, branch-led approach for secured business loans, and partnerships with business aggregator platforms, enabling the company to serve customers across diverse geographies.

Experienced Professional Management Team Backed by Reputed Investors

The company is led by an experienced management team including Chairman and CEO Bhupinder Singh, an industry veteran with over two decades of experience in financial services. The company is backed by marquee investors including KKR India Financial Investments, MNI Ventures, MEMG Family Office LLP, OAKS Asset Management, Elevar AIF, Zerodha Broking, and Kamath Associates.

Robust Funding Profile and Diversified Liability Management Framework

InCred Holdings maintains a well-diversified liability profile with borrowing relationships with over 51 lenders including public sector banks, private sector banks, mutual funds, development finance institutions, and small finance banks. The company is rated “AA-/Stable” by both CRISIL Ratings and ICRA. Its capital adequacy ratio stood at 24.97% as of December 2025, significantly above the regulatory requirement of 15%.

More About InCred Holdings Limited

Business Overview

InCred Holdings Limited, incorporated in January 2011, is a diversified financial services company operating through its material subsidiary, InCred Financial Services Limited (IFSL), a retail-focused, middle-layer NBFC registered with the Reserve Bank of India. The company was founded by Bhupinder Singh in 2017 and has built its business around multiple lending segments. The InCred Group has three distinct businesses: InCred Finance (lending-focused NBFC), InCred Capital (integrated institutional platform), and InCred Money (retail wealth-tech investment distribution vertical).

Product Portfolio

The company offers a diversified suite of loan products across five key verticals:

- Personal Loans: The largest segment contributing 55.56% of AUM at ₹8,027.12 crore as of December 31, 2025. These are unsecured loans offered through the InCred mobile application and channel partners.

- Student Loans: The second-largest category at 22.15% of AUM or ₹3,200.51 crore. These loans are distributed through partnerships with educational consultants, test preparation centres, and student portals.

- Secured Business Loans: Including Loan Against Property and school financing, contributing 8.74% of AUM or ₹1,262.64 crore. These are distributed through a cluster-based branch-led approach.

- Specialised MSME Loans: Contributing 7.83% of AUM or ₹1,131.14 crore. These include embedded finance and asset-backed financing facilities.

- Lending to Financial Institutions: Contributing 5.55% of AUM or ₹801.40 crore. These are originated and managed by the internal relationship management team.

Technology Platform

InCred Holdings has developed an in-house, AI-enabled proprietary technology platform that manages the entire lending lifecycle. The platform is built on four foundational pillars: mobile-first philosophy, custom workflows and flexible API framework, modern scalable architecture, and centralised data repository. The company has begun deploying autonomous AI agents at key points across the customer lifecycle, including AI-powered voice and conversational agents for lead qualification and AI voice agents for collections.

Distribution Network

The company has a multi-channel distribution network with 158 branches across 152 cities in 19 states and union territories, covering more than 17,000 pin codes. The distribution channels include:

- Direct sourcing through the InCred mobile application and website

- Channel partners including DSAs, connectors, and digital lending service providers

- Educational consultants, test preparation centres, and student portals for student loans

- In-house feet-on-street sales team for secured business loans

- Partnerships with business aggregator platforms for embedded finance

Credit Ratings and Capital Adequacy

The company is rated “AA-/Stable” by both CRISIL Ratings and ICRA. Its capital adequacy ratio stood at 24.97% as of December 2025, significantly above the regulatory requirement of 15%. The company maintained borrowing relationships with over 51 lenders as of December 31, 2025.

Industry Outlook

India NBFC Sector Overview

The Indian non-banking financial company (NBFC) sector continues to demonstrate robust growth, with NBFC credit standing at approximately ₹52 trillion in December 2024 and expected to exceed ₹60 trillion in FY2026. NBFC credit grew 16.7% year-on-year in FY26, underlining the sector’s growing role in meeting the financing needs of borrowers often underserved by traditional banking channels. The market expanded to approximately ₹1.04 lakh crore as of March 2026, with NBFCs increasing their market share to around 59%.

Growth Projections

NBFC assets under management are expected to grow 12-18% in FY26, led by MSMEs, gold loans, and retail lending. The growth of AUM for NBFCs is expected to remain robust at 15-17% over FY2025 and FY2026. Retail loans account for 57% of NBFC portfolios, with the retail segment expected to grow at a moderate pace of 16-18% in FY2026.

Key Growth Drivers

- Credit Growth: Bank credit growth accelerated to 15.9% in FY26, reflecting strong economic activity and credit demand. Personal loans, which make up 33% of overall credit, grew 16.2% in FY26.

- MSME Lending: MSME lending is expected to remain one of the strongest drivers of credit expansion in 2026, with the MSME sector growing by 11.6%.

- Education and Personal Loans: Education loans rose by 13.2%, while personal loans grew by 13.8%.

- Regulatory Support: ICRA has a stable outlook on the NBFC sector, barring NBFC-microfinance.

Competitive Landscape

NBFCs are likely to outperform banks in FY27 as stronger earnings growth, robust loan expansion, and stable asset quality trends create a favourable backdrop. Large NBFCs could see 3-5% earnings upgrades as borrowing costs ease. Credit offtake improved in March 2026 at 15.9% year-on-year.

How Will InCred Holdings Limited Benefit

- The company’s diversified product portfolio across personal loans, student loans, secured business loans, MSME loans, and lending to financial institutions positions it to benefit from India’s NBFC credit growth at 16.7% YoY in FY26.

- The personal loan segment’s 16.2% growth in FY26, representing 33% of overall credit, directly benefits the company’s largest product vertical which contributes 55.56% of AUM.

- The company’s focus on student loans (22.15% of AUM) positions it to benefit from the 13.2% growth in education loans, driven by increasing demand for higher education financing.

- The specialised MSME loan vertical (7.83% of AUM) is well-positioned to capture MSME lending growth at 11.6%, with MSME lending expected to remain a strong driver of credit expansion.

- The company’s robust funding profile with AA-/Stable rating and capital adequacy of 24.97% provides financial flexibility to scale operations and capture market opportunities.

- The proprietary AI-enabled technology platform enables efficient underwriting, risk management, and collections, supporting the company’s ability to maintain healthy asset quality (Net Stage 3: 0.87%) while scaling rapidly.

- The multi-channel distribution network with 158 branches across 19 states and 17,000+ pin codes provides extensive customer reach and market penetration capabilities.

- The company’s recognition as the fastest-growing diversified NBFC in PAT CAGR (85%) between FY23 and FY25 demonstrates its ability to outperform peers and capture market share.

Peer Group Comparison

|

Name of Company |

Revenue (₹ in million) |

P/E Ratio |

P/B Ratio |

Basic EPS (₹) |

Diluted EPS (₹) |

RoNW (%) |

NAV (₹) |

|

InCred Holdings Limited |

18,736.21 |

NA |

NA |

5.81 |

5.58 |

10.38% |

58.74 |

|

Peer Group |

|||||||

|

Bajaj Finance Limited |

6,96,835.10 |

35.43 |

5.96 |

26.89 |

26.82 |

19.10% |

159.37 |

|

HDB Financial Services Limited |

1,63,002.80 |

24.35 |

3.35 |

27.40 |

27.32 |

14.72% |

198.80 |

|

Aditya Birla Capital Limited |

4,05,899.80 |

27.30 |

2.79 |

12.80 |

12.67 |

11.03% |

124.08 |

|

Poonawalla Fincorp Limited |

41,897.60 |

NM |

4.13 |

(1.27) |

(1.27) |

(1.20)% |

105.76 |

|

SBI Cards and Payment Services |

1,80,722.20 |

32.02 |

4.45 |

20.15 |

20.14 |

14.63% |

144.86 |

|

Five-Star Business Finance |

28,478.39 |

13.19 |

2.25 |

36.61 |

36.50 |

18.68% |

214.13 |

|

SBFC Limited |

13,061.57 |

29.66 |

3.18 |

3.21 |

3.15 |

12.72% |

29.40 |

Key Strategies for InCred Holdings Limited

Scaling Existing Product Portfolio Through Channel and Category Expansion

InCred Holdings intends to drive growth across its multi-product platform by expanding distribution channels, geographic presence, and customer categories. For personal loans, the company will expand across categories and geographies with focus on engaging specific customer sub-groups and reaching new postal codes. In student loans, the company intends to broaden sourcing channels by increasing channel partners and selectively expanding support for a wider range of academic programmes. For secured business loans, the company will further expand its branch footprint and gradually enter new locations, particularly tier II and III towns.

Introduce New Products and Verticals Through a Structured Product Development Process

InCred Holdings intends to strengthen its long-term growth trajectory by adopting a structured and disciplined product development process for introducing new products and verticals. The approach involves identifying promising market opportunities, dedicating time to careful validation and development, and establishing robust operational frameworks and specialist teams before scaling up. The company’s LAP business followed this approach, scaling from ₹1,286.02 million AUM through 9 branches in FY23 to ₹8,607.18 million through 139 branches as of December 31, 2025.

Continue to Develop Risk Management Processes Through Technology-Enabled Solutions

InCred Holdings intends to enhance its risk management framework by leveraging data analytics, artificial intelligence, and machine learning to improve credit evaluation accuracy and strengthen fraud detection capabilities. For personal loans, the company plans to use multi-bureau scorecards and additional data points to further enhance underwriting. For student loans, the company will recalibrate its internal scorecard model to better predict student employability potential. Technology will continue to serve as a key enabler for operational efficiency by streamlining loan origination, disbursement, and ongoing monitoring processes.

Further Diversify Sources of Borrowings with a Prudent Approach to ALM

InCred Holdings is focused on strengthening and broadening its liability management practices by expanding and diversifying its borrowing base both in terms of number of lending relationships and different types of borrowing products. The company intends to maintain a prudent mix of long and short-term borrowings within its overall funding mix, providing stability and predictability to its financial position. The company will continue to seek funding from a wide range of sources while maintaining a disciplined focus on the cost of borrowing.

Continue Focus on Talent Acquisition, Capability Building, and Employee Retention

InCred Holdings remains committed to attracting and retaining talented employees while continuously building their capabilities to meet evolving business needs. The company provides targeted training and development programmes designed to strengthen essential skills and keep employees informed about cyber security best practices. The company supports motivation and long-term alignment by offering competitive incentives, including the continued award of ESOPs to eligible team members. The company’s efforts have been recognised with prestigious industry accolades including “Most Preferred Workplace – BFSI” and “Employer of the Future.”

FAQs

How can I apply for InCred Holdings Limited IPO?

You can apply via HDFCSky using UPI-based ASBA (Application Supported by Blocked Amount) through your bank account.

What is the total issue size of InCred Holdings Limited IPO?

The IPO comprises a fresh issue of ₹1,250 crore and an OFS of up to 9.90 crore equity shares.

When did InCred Holdings receive SEBI approval for its IPO?

InCred Holdings received SEBI approval on February 5, 2026, after filing its DRHP in November 2025.

On which exchanges will InCred Holdings Limited shares be listed?

The equity shares are proposed to be listed on both BSE (Bombay Stock Exchange) and NSE (National Stock Exchange).

What is the face value of InCred Holdings Limited equity shares?

The face value of each equity share is ₹10 per share.

Infographic Content

InCred Holdings Limited IPO Highlights

InCred Holdings Limited is a diversified financial services company operating through its NBFC subsidiary InCred Financial Services, offering personal loans, student loans, secured business loans, MSME loans, and lending to financial institutions across 19 states.

· Offer Size: ₹1,250 crore (Fresh Issue) + OFS of up to 9.90 crore equity shares

· Purpose: The net proceeds will be utilized primarily for investment in subsidiary InCred Finance to strengthen Tier-I capital base, support onward lending, and improve capital adequacy.

· Financials (Fiscal Year ended March 31, 2025): Revenue from Operations ₹18,736.21 million; Profit After Tax ₹3,731.50 million; EPS ₹5.81

· Listing: Mainboard IPO on BSE & NSE

How to apply IPO with HDFC SKY?

Follow these simple steps to apply for an IPO through HDFC SKY. Secure your investments and explore new opportunities with ease by accessing the IPOs available on the platform.

1Login to your HDFC SKY Account

2Select Issue

3Enter Number of Lots and your Price.

4Enter UPI ID

5Complete Transaction on Your UPI App

By signing up I certify terms, conditions & privacy policy