HCLTech Falls Over 3% As Cautious FY27 Outlook Disappoints Street Despite Q1 Beat

Authored By HDFC SKY | Published at: Jul 14, 2026 12:15 PM IST

Mumbai, July 14: HCL Technologies share price fell as much as 3.3% on Tuesday after the IT major’s better-than-expected June-quarter earnings failed to impress investors, with the company opting to retain its full-year revenue and margin guidance. The stock emerged among the top losers on the Nifty IT index, as analysts said the unchanged outlook signalled continued demand uncertainty despite a healthy quarterly performance.

The country’s third-largest IT services exporter reported a 20% year-on-year rise in consolidated net profit to Rs 4,624 crore for the quarter ended June, while revenue increased 14%, both exceeding Street expectations. However, management maintained its FY27 revenue growth guidance of 1-4% in constant currency and EBIT margin guidance of 17.5-18.5%, dashing hopes of an upgrade after a strong quarter and robust deal wins. As of writing the stock was down 3.1% at Rs 1,183.30.

Guidance disappoints despite earnings beat

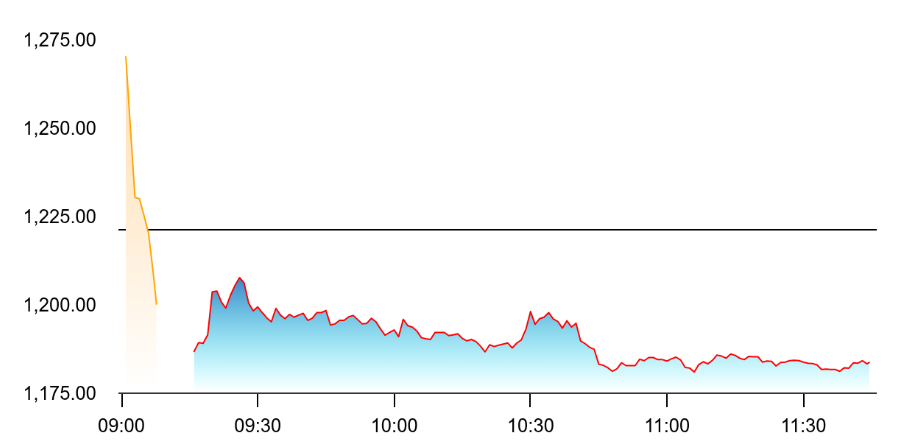

Stock is down as investors fear the future after muted outlook. Source: NSE

While HCLTech’s quarterly performance was broadly in line with the company’s execution track record, analysts said investors were looking for a stronger signal on demand recovery. Instead, management’s decision to stick with its earlier guidance suggested that macroeconomic uncertainty continues to weigh on technology spending.

Chief Executive Officer C Vijayakumar acknowledged that discretionary spending remains uneven across several verticals due to geopolitical tensions and global macroeconomic challenges, although he maintained that the company’s deal pipeline remains healthy and AI-led opportunities continue to expand.

Brokerages said the unchanged outlook overshadowed the earnings beat, prompting investors to lock in gains after the stock’s recent recovery.

Brokerages remain divided

Global and domestic brokerages offered mixed views on the stock following the results, with several maintaining a cautious stance on valuations and demand visibility.

One broker turned the most bearish by downgrading HCLTech to ‘Sell’ from ‘Neutral’ and cutting its target price to Rs 1,040 from Rs 1,135. The brokerage believes the company’s near-term growth prospects remain constrained, citing limited room for earnings upgrades and persistent weakness in discretionary spending.

Another retained its ‘Underweight’ rating while marginally raising its target price to Rs 1,060 from Rs 1,000. The brokerage highlighted continued softness in telecom and manufacturing demand, adding that spending recovery remains slower than anticipated. Another maintained an ‘Underperform’ rating, trimming its target price to Rs 1,070 from Rs 1,165.

Some brokerages see long-term opportunity

Not all brokerages turned cautious. One reiterated its ‘Buy’ rating and raised its target price, citing HCLTech’s resilient execution, improving deal momentum and expanding artificial intelligence capabilities.

The brokerage believes the company remains well positioned to benefit from large cost-transformation deals and AI-led spending once macroeconomic conditions improve. Another also lifted its target price while maintaining a constructive stance, pointing to the company’s strong execution and healthy order pipeline.

Several domestic brokerages echoed similar optimism, arguing that the earnings beat demonstrates HCLTech’s ability to execute well even in a challenging demand environment. However, most agreed that sustained revenue acceleration will depend on a broader recovery in global technology spending.

Demand recovery still elusive

Analysts continue to see discretionary spending as the biggest challenge for the Indian IT sector. Clients across banking, telecom, manufacturing and retail remain cautious on large technology investments amid geopolitical uncertainty and a slowing global economy.

Although generative AI continues to drive conversations with clients, many projects remain in the pilot stage, limiting near-term revenue contribution. Brokerages expect meaningful monetisation of AI-related investments to take time, keeping overall sector growth subdued over the next few quarters.

What lies ahead

Investors will now closely monitor management commentary over the coming quarters for signs of improving client spending and any possibility of a guidance revision. Progress in converting the company’s healthy deal pipeline into revenue, along with growth in AI-led services, will remain key triggers for the stock.

For now, analysts believe HCLTech’s strong operational execution is being overshadowed by a challenging demand environment. While the June-quarter earnings reinforced confidence in the company’s delivery capabilities, the absence of a guidance upgrade suggests management remains cautious about the pace of recovery in global IT spending, keeping investor sentiment subdued despite the earnings beat.

Source

- https://www.nseindia.com/get-quote/equity/HCLTECH/HCL-Technologies-Limited

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.

Please Note: The information shared is intended solely for informational purposes and does not make any investment recommendations