Sectoral Performance on June 30, 2026: IT Rout Overshadows Realty, Pharma Strength as Broader Markets Hold Firm

Authored By HDFC SKY | Published at: Jun 30, 2026 05:26 PM IST

Mumbai, June 30: Sectoral indices ended on a mixed note on Tuesday, with heavy selling in information technology stocks dragging benchmark indices lower, while buying in realty, consumer durables, pharmaceuticals and select auto names helped limit the downside. Domestic-facing sectors outperformed even as investors remained cautious ahead of key U.S. economic data and the start of a new monthly derivatives series.

IT leads the decline

The Nifty IT index tumbled 2.7%, emerging as the session’s biggest loser as investors trimmed positions in export-oriented technology stocks amid concerns over discretionary spending and uncertainty surrounding the U.S. interest-rate outlook.

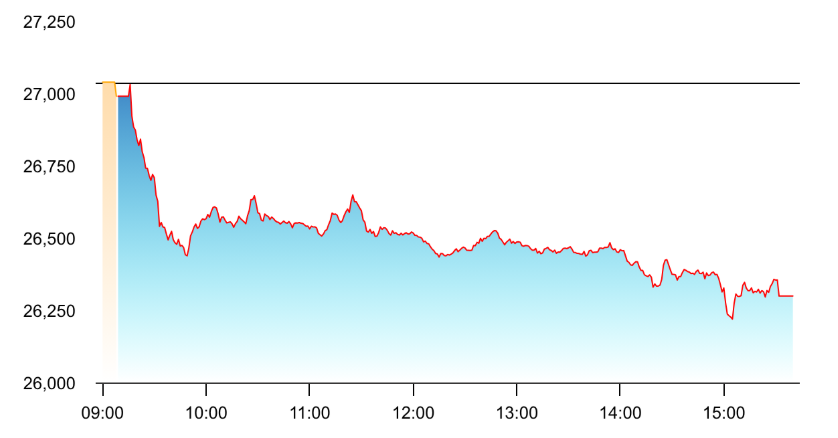

Nifty IT plunged amid a plethora of fears: AI, Accenture’s weak outlook, possibility of US rate hikes later this year. Source: NSE

Heavyweights Infosys (down 3.5%), TCS (down 3.2%), Wipro (down 2.9%), HCLTech, and Tech Mahindra, LTIMindtree all traded lower, with selling pressure intensifying through the afternoon session.

Realty, consumer durables shine

Domestic-facing sectors attracted buying interest, with the Nifty Realty and Nifty Consumer Durables indices gaining more than 1% each.

Real estate developers DLF (up 0.9%), Godrej Properties (up 2%), Prestige Estates Projects (up 1.6%), Phoenix Mills and Lodha Developers advanced, while consumer discretionary stocks such as Titan Company (up 3%), Dixon Technologies (up 1%) and Whirlpool of India (up 1.5%) also witnessed healthy gains. To be sure, Dixon rose after a report said the government’s approval for the company’s proposed joint venture with Chinese smartphone maker Vivo is in its final stages.

Pharma extends gains

The Nifty Pharma index extended gains, rising 0.4%, supported by buying in defensive healthcare names.

Stocks including Cipla (up 0.8%), Lupin (up 0.4%) and Aurobindo Pharma (up 2%) traded in positive territory as investors rotated into relatively defensive sectors amid weakness in technology shares. Aurobindo jumped after announcing the completion of its acquisition of Lannett Company, Inc., USA.

Auto sees stock-specific action

The Nifty Auto index traded mixed as company-specific developments dictated investor sentiment.

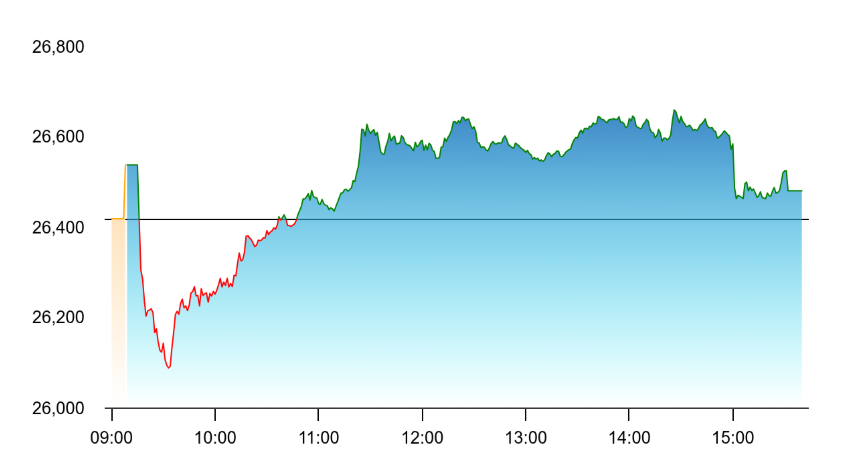

Nifty Auto edged up with Maruti rising after a thumbs-up from Jefferies even as Royal Enfield maker Eicher Motors slumped over Delhi’s new electric vehicle policy. Source: NSE

Maruti Suzuki India emerged as the top Nifty gainer after Jefferies upgraded the stock to “Buy” and raised its target price. Tata Motors Passenger Vehicles also advanced, while Ola Electric Mobility and Ather Energy rallied after the Delhi government approved its EV Policy 2.0, offering subsidies for electric two-wheelers and tax exemptions for eligible electric cars.

On the other hand, Eicher Motors slumped 4.8% after analysts warned that Delhi’s new electric vehicle policy, which envisages a gradual transition away from petrol-powered two-wheelers, could pose long-term challenges for Royal Enfield.

PSU banks, FMCG under pressure

The Nifty PSU Bank and Nifty Media indices each lost around 0.7%, while the Nifty FMCG index also declined by a similar margin.

Among FMCG names, Tata Consumer Products and Hindustan Unilever traded lower. In the banking space, State Bank of India, Bank of Baroda, Punjab National Bank and Canara Bank witnessed declines.

Broader market resilient

Despite the decline in benchmark indices, the broader market showed a positive bias.

The Nifty Midcap 100 index gained 0.4%, while the Nifty Smallcap 100 climbed 1%, supported by stock-specific buying.

Among notable movers, Vedanta Iron & Steel extended its post-listing rally for an 11th straight session, Vodafone Idea edged higher on improving subscriber trends and passive inflow expectations, while Yes Bank fell after announcing plans to raise up to ₹16,000 crore through a combination of equity and debt instruments.

Source

- NSE

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.

Please Note: The information shared is intended solely for informational purposes and does not make any investment recommendations