Nifty 50

- Tech Mahindra₹1,57160.70 (4.02%)

- Hindalco Industries₹945.10-14.20 (-1.48%)

- Kotak Mahindra Bank₹390.7013.55 (3.59%)

- Dr. Reddy's Labs₹1,210.30-14.10 (-1.15%)

- Jio Financial ₹242.707.05 (2.99%)

- Wipro₹175.90-1.84 (-1.04%)

- TCS₹2,26564.00 (2.91%)

- Sun Pharmaceutical₹1,934-16.10 (-0.83%)

- Reliance Industries₹1,32932.40 (2.50%)

- Apollo Hospitals₹8,820-68.00 (-0.77%)

- ICICI Bank₹1,45233.80 (2.38%)

- Max Healthcare₹1,090-8.20 (-0.75%)

- Hindustan Unilever₹2,14344.60 (2.13%)

- Bharti Airtel₹1,908-13.80 (-0.72%)

- Eicher Motors₹7,569150.50 (2.03%)

- Cipla₹1,419.50-10.00 (-0.70%)

- Mahindra & Mahindra₹3,178.9061.10 (1.96%)

- Trent₹2,842-18.20 (-0.64%)

- Bajaj Finance₹1,055.3017.70 (1.71%)

- HDFC Life Insurance ₹564-3.60 (-0.63%)

- Offerings

- Tools & Platforms

Tools & Calculators

- Open API

- Calculators

- SIP Calculator

- CAGR Calculator

- Compound Interest Calculator

- FD Calculator

- RD Calculator

- EPF Calculator

- Retirement Calculator

- HDFC SIP Calculator

- Mutual Fund Return Calculator

- Lumpsum Calculator

- Step Up SIP Calculator

- ETF SIP Calculator

- Brokerage Calculator

- Equity Margin Calculator

- SWP Calculator

- EMI Calculator

- MTF Calculator

- Margin Pledge Calculator

- Markets

Stocks

F&O

Mutual Funds

- More

- What Exactly Is Repo Rate Transmission?

- Why Your EMI Doesn’t Drop the Day RBI Cuts Rates

- Why RBI Says Transmission Takes 6–12 Months

- Stage 1: Financial Markets React Immediately

- Stage 2: Banks Adjust Internal Funding Costs

- Stage 3: Lending Benchmarks Move

- Stage 4: Borrowers See EMI Change

- Stage 5: Spending and Economic Growth Respond

- A Real EMI Example: How Much Delay Changes Your Savings

- Why Some Borrowers Benefit Faster Than Others

- What You Can Do Instead of Waiting

- Conclusion

- What Exactly Is Repo Rate Transmission?

- Why Your EMI Doesn’t Drop the Day RBI Cuts Rates

- Why RBI Says Transmission Takes 6–12 Months

- Stage 1: Financial Markets React Immediately

- Stage 2: Banks Adjust Internal Funding Costs

- Stage 3: Lending Benchmarks Move

- Stage 4: Borrowers See EMI Change

- Stage 5: Spending and Economic Growth Respond

- A Real EMI Example: How Much Delay Changes Your Savings

- Why Some Borrowers Benefit Faster Than Others

- What You Can Do Instead of Waiting

- Conclusion

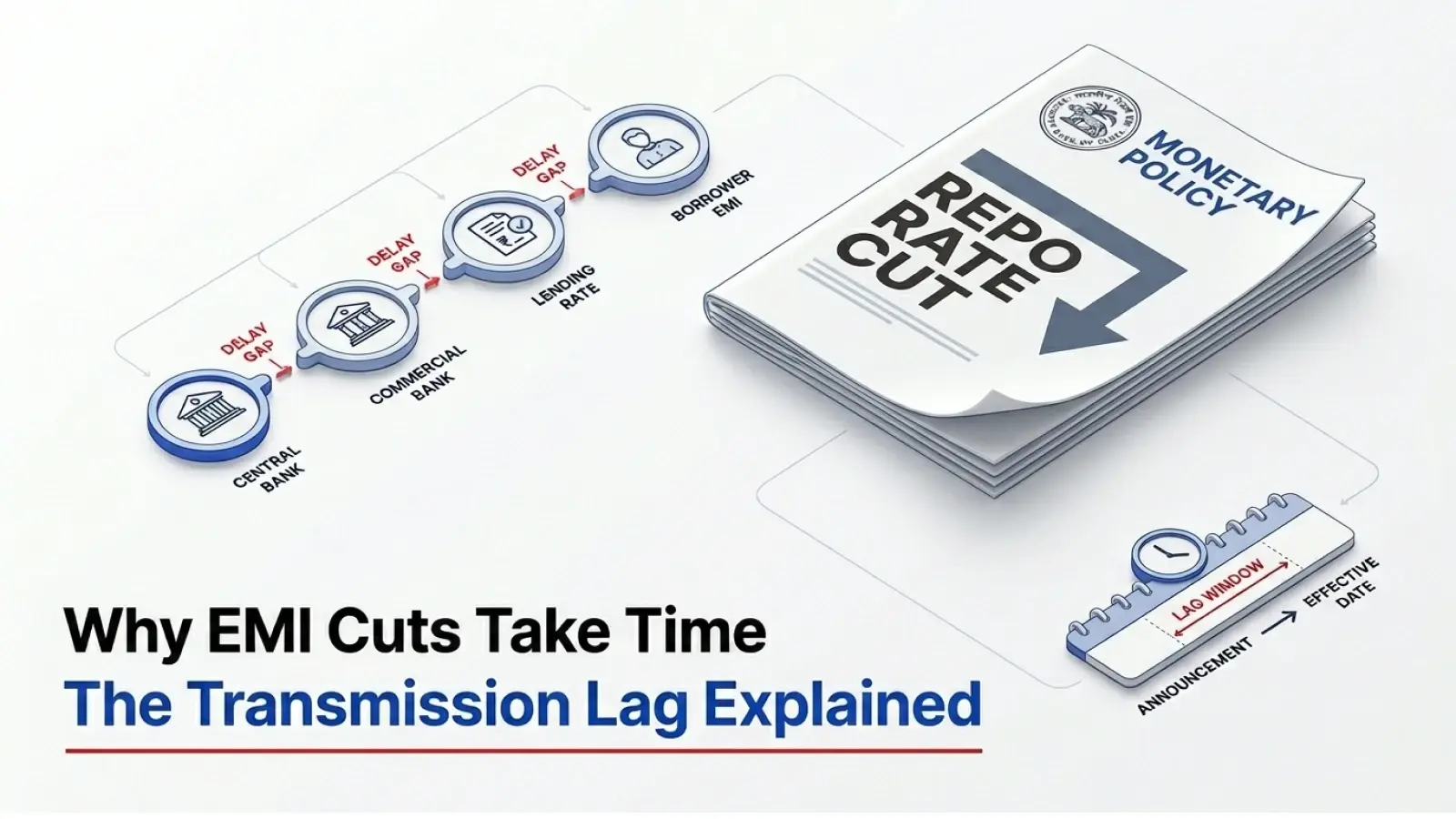

The Repo Rate Transmission Lag: Why RBI Rate Cuts Take 6–12 Months to Show Up in Your EMI

By Aseem Shrivastava | Published at: Jun 3, 2026 10:47 AM IST

The RBI announces a rate cut, headlines promise cheaper loans, and borrowers expect instant relief. Yet their monthly payments often stay exactly the same. This delay happens because rate cuts do not move directly into loans overnight. This process, known as repo rate transmission lag, can take weeks or even months. Understanding The Repo Rate Transmission Lag: Why RBI Rate Cuts Take 6–12 Months to Show Up in Your EMI helps borrowers know what to expect and where the waiting happens.

What Exactly Is Repo Rate Transmission?

The repo rate is the interest rate at which the Reserve Bank of India lends money to commercial banks. Repo rate transmission describes how that change moves through the banking system and eventually reaches borrowers.

The process usually follows this path:

RBI cuts repo → banks’ borrowing costs may fall → banks adjust lending benchmarks → your loan interest changes → your EMI or loan tenure changes.

A repo rate cut is the starting signal, not the final outcome.

Also Read: Decoding RBI’s monetary policy statement: The 5 lines that actually move markets

Why Your EMI Doesn’t Drop the Day RBI Cuts Rates

Several moving parts slow down the journey from an RBI announcement to actual savings in your monthly loan payment.

- Banks Don’t Fund Loans Only from RBI

Banks do not depend only on RBI borrowing to issue loans. They mainly use customer deposits, which often carry fixed interest commitments. If deposit costs remain high, banks cannot reduce lending rates immediately, and strong competition for deposits can delay the process further. - Banks Protect Their Interest Margins

Banks need to maintain healthy profits while managing lending risks. Even after a repo cut, they may pass on only part of the benefit at first. This cautious approach often causes loan rates to fall more slowly than the RBI’s benchmark rate. - Loan Benchmark Matters More Than Most Borrowers Realise

Your loan type plays a major role in timing. Repo-linked loans such as EBLR or RLLR often adjust within one to three months. MCLR-linked loans usually take six to twelve months, while fixed-rate loans may not offer immediate relief at all. - The Hidden Delay: Your Loan Reset Date

Even repo-linked loans do not change instantly. Banks revise loan rates on specific reset dates. For example, if RBI cuts rates in April but your loan resets in July, your EMI changes only then. The same rate cut can affect borrowers differently.

Why RBI Says Transmission Takes 6–12 Months

Monetary policy works with what economists call “long and variable lags.” This is normal around the world, not just in India. The effect moves through several stages before borrowers feel the benefit.

Stage 1: Financial Markets React Immediately

Bond markets, stock markets, and banking shares often respond within hours of an RBI announcement. Investors quickly adjust expectations, but these market reactions do not directly lower household loan payments. Borrowers still need to wait for banks to process changes.

Stage 2: Banks Adjust Internal Funding Costs

Banks first assess how the repo cut affects their funding mix, deposit obligations, and future lending plans. They may revise deposit rates gradually. This internal adjustment period often creates one of the biggest delays in transmission.

Stage 3: Lending Benchmarks Move

Once banks complete their internal review, they update benchmark rates such as EBLR, RLLR, or MCLR. Some benchmarks respond faster than others. Even after this step, individual borrowers may still need to wait for loan-specific resets.

Stage 4: Borrowers See EMI Change

Only after benchmark updates and loan reset dates align do borrowers finally notice lower EMIs or shorter loan tenures. This is the moment most people expect immediately, but it often arrives several months after the RBI announcement.

Stage 5: Spending and Economic Growth Respond

Lower EMIs can increase disposable income, encouraging households to spend more or save differently. Businesses may also borrow more. These broader economic effects take additional time, which is why policy changes influence growth gradually.

A Real EMI Example: How Much Delay Changes Your Savings

Consider a home loan of ₹50 lakh with a tenure of 20 years at an interest rate of 8.75%. If RBI cuts the repo rate by 0.50% and the full benefit reaches the borrower immediately, the monthly EMI could fall by around ₹1,550.

That reduction may seem modest, but over time it adds up significantly.

Now imagine the bank takes nine months to pass on the same cut. During those months, the borrower continues paying the higher EMI and spends nearly ₹14,000 more than necessary before receiving any relief.

This example shows why timing matters. A delayed rate cut may eventually help, but borrowers lose valuable savings while they wait.

Why Some Borrowers Benefit Faster Than Others

Not every borrower experiences the same timeline. Several factors influence how quickly rate cuts reach individual loans.

- Public sector and private banks often differ in how quickly they pass on rate cuts.

- New loans sometimes receive updated rates faster than older loan accounts.

- Home loans usually see quicker transmission than personal or unsecured loans.

- Borrowers with strong credit scores may receive faster repricing opportunities.

- Loan agreements and benchmark clauses can directly affect transmission speed.

What You Can Do Instead of Waiting

While banks take time to pass on RBI rate cuts, borrowers do not need to stay passive. A few simple checks and timely actions can help you understand your position and improve your chances of benefiting sooner.

- Check Your Loan Benchmark

Review your loan documents and identify whether your loan follows EBLR, RLLR, or MCLR. Knowing your benchmark helps you estimate how quickly rate cuts may affect your EMI. - Ask for Benchmark Conversion

If your loan still uses MCLR, ask your bank whether you can switch to a repo-linked benchmark. A small conversion fee could lead to faster future benefits. - Track Your Reset Cycle

Find out your next loan reset date and mark it clearly. This date often determines when your EMI changes, regardless of when RBI announces the rate cut. - Negotiate With Your Bank

Do not hesitate to speak with your lender. Banks sometimes offer revised terms or better rates, especially when borrowers have strong repayment records and stable finances. - Consider Refinancing if Transmission Is Weak

If your lender delays passing on benefits repeatedly, compare refinancing options with other banks. A loan transfer may help you secure faster and better interest rate reductions.

Conclusion

RBI rate cuts do not work like instant discounts on your loan. The banking system needs time to absorb and pass on every change. Understanding the transmission lag helps borrowers stay realistic and plan better. Smart borrowers do not simply wait—they monitor benchmarks, track reset dates and explore refinancing when needed.

By signing up I certify terms, conditions & privacy policy