Ashok Leyland Share Slides After Reporting 14% Increase in Earnings as Street Cautious on Margins

Authored By HDFC SKY | Published at: May 29, 2026 03:09 PM IST

Mumbai, May 29: Ashok Leyland share price declined on Thursday after the commercial vehicle maker reported March quarter earnings, with investors turning cautious despite healthy growth in profitability and continued strength in its core business. The stock came under pressure as market participants assessed valuation concerns and the broader outlook for the commercial vehicle cycle following a sharp rally in recent months.

The company reported a consolidated net profit of ₹1,291 crore for the fourth quarter, marking a rise of around 14% year-on-year. Revenue growth, improved realisations and operational efficiencies supported earnings during the quarter. Ashok Leyland also announced an interim dividend of ₹2.5 per share, reflecting confidence in its cash flows and balance sheet position.

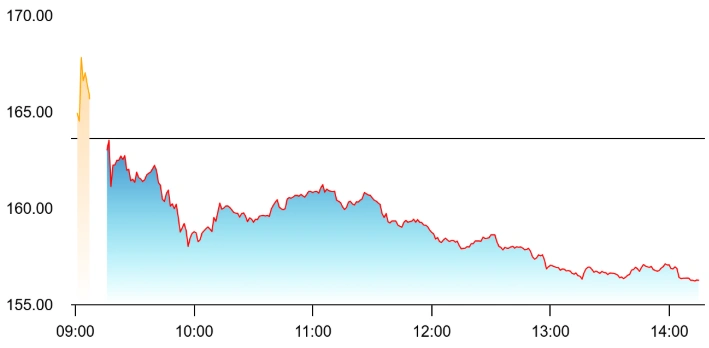

However, the results failed to trigger fresh buying momentum in the stock, with investors appearing to book profits after the recent run-up. The reaction also suggested that a large part of the earnings improvement had already been factored into valuations ahead of the results announcement. As of writing, the share was trading 4.6% lower at Rs 156.

Margin Performance Is a Key Monitorable

Analysts warned against margin pressures due to increased input costs arising from the ongoing Iran conflict. Input costs surged 29%, bumping up expenses by 19%.

The stock slid as input costs rose scaring investors. Source: NSE

The company has also benefited from sustained momentum in the medium and heavy commercial vehicle segment, supported by infrastructure activity, replacement demand and improving fleet utilisation levels. Market participants noted that Ashok Leyland’s focus on expanding its presence in alternate fuel technologies and electric mobility remains strategically important as the commercial vehicle industry gradually transitions toward cleaner transportation solutions.

Its aftermarket business and financial services arm also continued to support earnings visibility, helping diversify revenue streams beyond core vehicle sales.

Brokerages Divided on Valuation Comfort After Rally

Brokerage commentary after the results remained mixed, with several analysts retaining constructive long-term views on the company while flagging limited near-term upside after the recent rally in the stock.

Some brokerages pointed to Ashok Leyland’s strong positioning in the domestic commercial vehicle market, improving balance sheet and healthy return ratios as factors that continue to support the investment case. Others, however, warned that demand growth could moderate in the coming quarters if infrastructure spending slows or freight activity weakens.

Investors are also closely tracking the outlook for fleet replacement demand, rural recovery and financing conditions, all of which play a critical role in determining commercial vehicle sales momentum.

Despite Friday’s decline, sentiment around the stock remains supported by expectations that India’s long-term infrastructure and logistics growth story could continue to benefit leading commercial vehicle manufacturers such as Ashok Leyland over the medium term.

Source:

- https://www.nseindia.com/get-quote/equity/ASHOKLEY/Ashok-Leyland-Limited

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.

Please Note: The information shared is intended solely for informational purposes and does not make any investment recommendations