NTPC Green Energy Slips Over 3% as Q4 FY26 Net Profit Drops 15%

Authored By HDFC SKY | Published at: May 25, 2026 12:12 PM IST

Mumbai, May 25: NTPC Green Energy Limited (NSE: NTPCGREEN) came under selling pressure on Monday morning, with the stock slipping sharply from its opening level despite the company reporting a dramatic improvement in full-year profitability, as investors appeared to book gains after recent strength in the renewable energy counter.

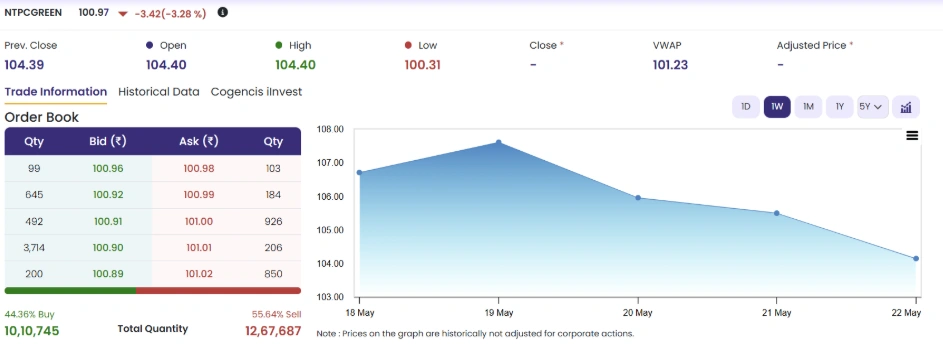

The stock opened at ₹104.40 in line with its previous close of ₹104.39 before sellers took control almost immediately, pulling the counter down to a session low of ₹100.31 within the first hour of trade. The LTP stood at ₹100.99, down ₹3.40 or 3.26% from the previous close, with the VWAP for the session at ₹101.23 sitting above the LTP, indicating that selling pressure accelerated through the morning session as the stock slid below its volume-weighted average.

The order book at the time of writing showed 45.01% buy-side interest versus 54.99% on the sell side, with total buy quantity of 9,94,336 shares against 12,14,660 shares on the sell side, confirming that bearish momentum remains dominant heading into the afternoon session.

Weekly Trend

The weekly chart reveals a stock in a clear and sustained distribution phase over the past five sessions. NTPCGREEN opened the week of May 18 near ₹106.85, briefly spiked to approximately ₹107.50 on May 19 its best level of the week before beginning a consistent and uninterrupted slide that carried it down through ₹106.00 on May 20, ₹105.40 on May 21, and further to ₹104.40 by May 22. Monday’s early-session gap-down extension of this weakness to ₹100.31 signals that the selling pressure has intensified rather than abated, suggesting that the stock’s short-term trend remains firmly negative despite the strong underlying earnings print.

Q4 FY26 Consolidated Results: Revenue Up 47%, Net Profit Down 15%

NTPC Green Energy Limited (NSE: NTPCGREEN) delivered a mixed fourth-quarter performance on a consolidated basis for the quarter ended March 31, 2026, with revenue growth significantly outpacing profit expansion as rising finance costs weighed on the bottom line. Revenue from operations for Q4 FY26 surged 46.7% year-on-year to ₹912.63 crore from ₹622.27 crore in Q4 FY25, while total income for the quarter rose 25.4% to ₹942.49 crore from ₹751.50 crore in the year-ago period.

Net profit for the quarter, however, declined 15.4% year-on-year to ₹197.17 crore from ₹233.21 crore in Q4 FY25, as finance costs jumped sharply to ₹257.45 crore from ₹176.77 crore a direct consequence of the company’s aggressive debt-funded capacity expansion across its renewable energy portfolio. EBITDA for the quarter came in at ₹822.32 crore against ₹689.45 crore in Q4 FY25, a gain of 19.3% year-on-year, indicating that operational performance remained healthy even as debt servicing pressures compressed the net profit line. Basic EPS for Q4 FY26 stood at ₹0.23 against ₹0.28 in the year-ago quarter, a decline of 17.9%.

FY26 Full-Year Consolidated Results

For the full year ended March 31, 2026, NTPC Green Energy reported a 29.4% jump in revenue from operations to ₹2,858.42 crore from ₹2,209.64 crore in FY25, while total income for the year rose 23.1% to ₹3,035.12 crore from ₹2,465.70 crore. Full-year net profit grew a modest 9.96% to ₹521.35 crore from ₹474.12 crore in FY25, with the gap between revenue growth and profit growth again explained by finance costs rising to ₹687.00 crore from ₹760.68 crore in FY25. Full-year EBITDA expanded 13.8% to ₹2,471.61 crore from ₹2,171.56 crore in FY25. Basic EPS for FY26 stood at ₹0.62 against ₹0.67 in FY25, a decline of 7.5%, with no dividend announced for the year.

Source:

- https://www.nseindia.com/get-quote/equity/NTPCGREEN/NTPC-Green-Energy-Limited

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.

Please Note: The information shared is intended solely for informational purposes and does not make any investment recommendations