HSIE Institutional Report: Apollo Tyres Feb, 06 2026

Authored By Prime Research | Last Modified: Feb 6, 2026 03:12 PM IST

Growth Picks up, Albeit Margins May Remain Stressed

The GST rate cut let boost to OEM production as well as freight movement, coupled with higher marketing spends has led to revival of double-digit growth for the company. However, rising raw material prices, adverse forex, higher marketing spends, front loading of capex-related costs, and a new entrant (Balkrishna Industries) in the segment would keep pressure on margins in the near to medium term. However, the revival of growth in the standalone segment and improved visibility of the same has allowed us to raise the multiple from 12.5x earlier to 13x now (near its five-year mean) of Dec-27 EPS for a TP of INR 454. We maintain SELL.

Consolidated Performance

Consolidated EBITDA margin at 15.3% improved 37bps QoQ, led by European business which was aided by seasonality and higher sale of winter tyres. It was 8bps below our estimate and 40bps above the Bloomberg consensus estimate. UHP mix for Q3FY26 stood at 52% vs 48% in Q3FY25.

Standalone Performance

Standalone EBITDA margin at 14.5% declined 76bps QoQ despite benign commodity prices, 84bps miss to our estimates and 71bps miss to Bloomberg consensus estimate. Revenue growth improved to 11.8% YoY, marking the first double-digit growth in the last 12 quarters.

Segment Wise Update

Volume growth for the standalone segment in Q3 stood at mid-teen levels. While in the OEM and replacement segments, it was mid-teens, exports growth was around 20%.

Europe Demand Soft, But Can Get Operationally Better

It commented that the Netherlands plant is expected to shut down by the end of June 2026, with production shifting to Hungary and India (underway). The Europe business is expected to see the benefit to operational profitability from this in H2FY27.

Marketing, Brand Building

It indicated that sponsorship of the Indian cricket team improved brand traction, thereby contributing to higher sales. However, higher marketing spends of INR 1.5bn in Q3 were an anomaly, as they included a one-time activation fee in addition to the usual sponsorship fee. The company expects elevated expenses to persist in the near term. Overall, marketing spends are expected to increase from the earlier levels of 2% to 2.5% in a normalized scenario.

Larger Capacity Addition

Management clarified that it would be adding a capacity to produce 10.5k PCR tyres per day to the existing capacity of 58.5k, while for the TBR segment, it is adding 3.6k to the existing capacity of 15k. It expects this to be completed by FY29, with an investment of INR 58.1bn, which is to be funded by a mix of internal accrual and debt. Current consolidated net debt stood at INR 13bn.

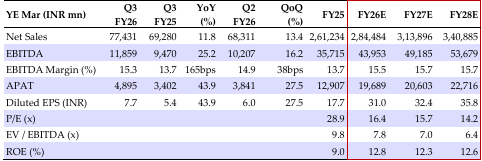

Quarterly/Annual Financial Summary

Source: HSIE Research (HSIE Results Daily Report – 06 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.