HSIE Institutional Report: Ashok Leyland Feb, 12 2026

Authored By Prime Research | Last Modified: Feb 12, 2026 02:02 PM IST

Improved Demand Visibility, Albeit Valuation is Rich

Management has guided for improved demand visibility over at least the next 2-3 quarters as freight movement as well as freight rates have been rising, and this is also leading to large fleet operators starting to come back to the CV market, which was earlier being driven largely by the retail customer. We expect the recently launched products and increasing touchpoints to further aid volume growth. Considering the positives, we value the company’s core business at 13.5x Dec-27 EV/EBITDA (vs 13x earlier), and add the value of Hinduja Leyland Finance (INR 22) to get a TP of INR 209. We maintain an ADD rating. However, we remain concerned by the higher pledging of the promoter group, and will closely watch out for any developments on that front.

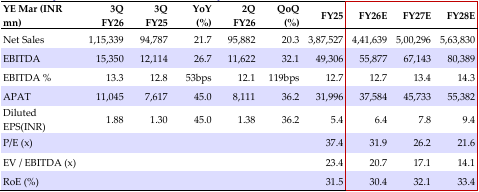

Ashok Leyland Quarterly Performance

EBITDA margin at 13.3%, improved 53bps YoY and 119bps QoQ, in line with our estimate of 13.3%, but above Bloomberg consensus estimate of 13%, driven by operating leverage, increasing non-CV mix and continued focus on cost reduction, though partially negated by higher commodity costs.

Demand Momentum to Continue

Management mentioned that the GST rate cut has created a major fillip in domestic consumption and therefore freight demand, leading to improved sentiment for both retail and fleet buyers. It expects momentum to continue into H1FY27, aided by a low base. It sees good potential for replacement demand as a reasonable number of inefficient and higher polluting older vehicles remain on the road.

Improving Non CV Mix

The power solutions business grew 45% YoY and the defence business grew 84% YoY. As a % of revenue, power solutions mix = 3.6% (vs 3.0% last year) and defence mix = 1.5% (vs 1.0% last year).

Other Highlights

1) It highlighted more product launches planned over the next six months, with a focus on product innovation for differentiation and premiumization. 2) Total touchpoints added in 9M for MHCV = 75 (45% were in the North and North East regions) and for LCV = 77, taking the total touchpoints to 2,041 (1,126 for MHCV and 915 for LCV). 3) Gross margin impact was on account of product mix and a 50bps impact from higher commodity costs; while it is countering that by reducing discounts. 4) On SWITCH India, it updated that in 9M, the entity sold 850 e-Buses and 1,200 eLCVs, with a positive PAT, and current order book at 1,350 units, on track to be FCF positive in FY27. 5) It does not believe the western DFC will have much impact on total volumes as a decrease in tractor trailer volumes will be made up for by ICV and LCV segments used in last mile connectivity.

Quarterly/Annual Financial Summary

Source: HSIE Research (HSIE Results Daily Report – 12 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.