HSIE Institutional Report: FSN E-commerce Ventures (Nykaa) Feb, 06 2026

Authored By Prime Research | Last Modified: Feb 6, 2026 12:50 PM IST

Strong Print; Margins Beat Expectations

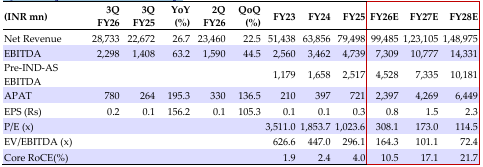

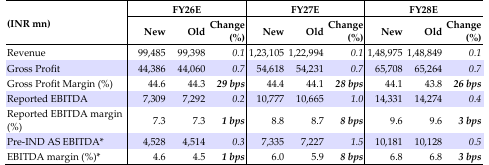

Nykaa’s Q2 topline grew 26.7% YoY to INR28.7bn (in-line), driven by healthy customer acquisition in BPC and fashion (26.4/32.3% respectively), successful Pink Friday sale and a strong performance in House of Nykaa BPC. BPC/fashion revenue grew 27.3/18.1% to INR26.2/2.35bn (in-line) respectively. GM expanded by 144bps YoY to 45.2% (HSIE: 44.5%), driven by higher owned brand share and improved margins in eB2B. Consequently, EBITDAM expanded 179bps YoY to 8% (HSIE: 7.3%). BPC EBITDAM (as % of NSV) expanded by ~130bps YoY to 10.1%, while fashion losses continue to ebb (at -2% vs -5.4% in Q3FY25), led by improved operating leverage. We largely maintain our FY27/28 EBITDA estimates and our SELL rating (given heady valuations; ~74x FY28 EV/EBITDA), with a DCF-based TP of INR 205/sh, implying 58x FY28 EV/EBITDA.

FSN E-commerce Ventures (Nykaa)Q3FY26 Highlights

Revenue grew 26.7% YoY to INR28.7bn, led by robust customer acquisition, successful Pink Friday sale and a strong performance in House of Nykaa BPC brands. BPC/fashion revenue grew 27.3/18.1% to INR26.2/2.35bn (in-line) respectively. BPC AUTC/orders grew 26.4/20.7% YoY in Q3 to 18.7/18.1mn respectively. Fashion AUTC/orders grew 32.3/42.9% YoY to 4.1/3mn respectively. Nykaa’s owned brands’ GMV surged 65% YoY in BPC to INR 7.75bn, while that in fashion declined 17% to INR 1bn. The company’s retail presence expanded to 276 beauty stores (+34% retail space YoY) with double-digit SSSG in Q3. GM expanded by 144bps YoY to 45.2% (HSIE: 44.5%), driven by higher owned brand share and improved margins in eB2B. Consequently, EBITDAM expanded 179bps YoY to 8% (HSIE: 7.3%), as aided by higher GM and better operating leverage. Notably, this expansion was achieved despite a 31% YoY increase in marketing and S&D spends to INR4.6bn. Note: BPC EBITDAM (as % of NSV) expanded by ~130bps YoY to 10.1%, while fashion EBITDAM expanded by 340bps YoY to -2%. EBITDA/APAT grew 63.2/195.3% YoY to INR2.3bn/780mn (HSIE: 2.1bn/755mn).

Outlook

Nykaa continues to be a leading platform for global beauty brands. The path to profitability for fashion and eB2B segments remains a key monitorable. We largely maintain our FY27/28 EBITDA estimates and our SELL rating (given heady valuations; ~74x FY28 EV/EBITDA), with a DCF-based TP of INR 205/sh, implying 58x FY28 EV/EBITDA.

FSN E-commerce Ventures (Nykaa) Quarterly Financial Summary

Change in Estimates

Source: HSIE Research (HSIE Results Daily – 06 Feb 26 – HSIE-202602060713371815208.pdf)

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.