HSIE Institutional Report: Aavas Financiers Feb, 06 2026

Authored By Prime Research | Last Modified: Feb 6, 2026 05:27 PM IST

Yet Another Quarter of Muted Growth

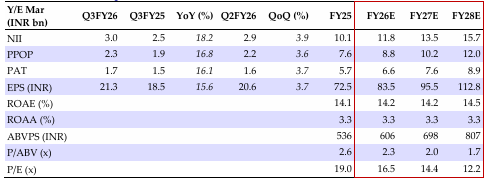

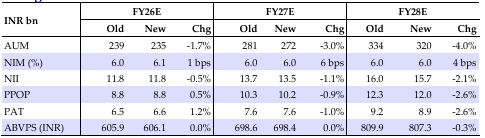

]AAVAS’s Q3FY26 earnings were marginally higher than our estimates, driven by better-than-expected operating efficiency and improving asset quality. Disbursements growth remained muted (+8% YoY), leading to further moderation in AUM growth to +15.4% YoY. While opex ratios improved sequentially (C/I at 43%; opex to AUM at 3.2%), it is yet to see meaningful improvement. Amidst growth headwinds (disbursements growth for FY25/9MFY26 at 10%/8% YoY), AAVAS has deferred its aspirational AUM guidance of INR 550bn by FY31-FY32E vs. FY30 earlier. We revise our FY26E/FY27E/FY28E earnings estimates to factor in lower loan growth, partly offset by higher NIM and maintain ADD with a revised RI-based TP of INR1,570 (implying 2.1x Sep-27 ABVPS).

NIM Reflation led by Cost of Fund Tailwinds

AAVAS’s core spreads reflated to 5.34% (Q2FY26: 5.23%), driven by reduction in cost of funds (by 16bps), while asset yields moderated marginally. Other income grew by 17% YoY, driven by assignment income (26% YoY). Opex ratios improved marginally sequentially despite impact of labor wage code (opex to AUM at 3.3%) driven by Tech transformation, although major benefits are yet to be seen.

Improving Asset Quality

AAVAS’s asset quality improved marginally sequentially with 1+ dpd/GS II/GS III at 3.8%/1.52%/1.19% vs. 3.99%/1.53%/1.24% in Q2FY26, driving credit costs of 18bps. Improvement in asset quality amidst a challenging macro environment is reflective of conservative underwriting practices at AAVAS.

Uphill Task for Meaningful Growth Revival Ahead

AAVAS’s AUM growth continues to be driven by MSME loans (21% of AUM; +33% YoY), while home loans (+11% YoY) and LAP growth remained subdued (+12% YoY). While management is upbeat about strong loan growth prospects on the back of tech transformation, increasing distribution and widening customer acquisition funnel, heightened competitive intensity coupled with the current macroeconomic environment and increasing scale remain a key concern for AUM aspiration of INR 550bn by FY31-32E (~15-18% CAGR).

Financial Summary

Change in Estimates

Source: HSIE Research (HSIE Results Daily Report – 06 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.