HSIE Institutional Report: ABB India Feb, 24 2026

Authored By Prime Research | Published at: Feb 24, 2026 01:14 PM IST

Orders Surge; Margins Squeeze

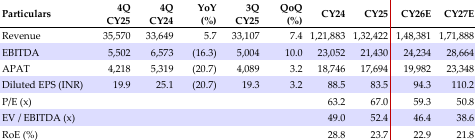

ABB India Ltd (ABB) reported a stable quarter with revenue/EBITDA/APAT beat/(miss) of +4.0/5%/in line respectively. ABB’s Q4CY25 order inflow (OI) stood at INR 40.9bn (+52%/+19.5%YoY/QoQ) and the backlog (OB) stood at INR 104.7bn as of Dec’25 (0.77x CY25 revenue). ABB plans to expand across 23 segments with a strategic focus on renewables, electronics, data centers, and grid modernization, positioning itself to benefit from an anticipated resurgence in private capex in 2026 supported by favorable policies and trade agreements such as the India-EFTA deal. It is integrating AI and ML into automation and motion products while witnessing rising demand for premium offerings in Tier 2 and Tier 3 cities, driven by entrepreneurial growth. ABB anticipates persistent margin pressures for the next 2 3 quarters, led by a combination of rising costs, an unfavorable revenue mix, increased competitive pressure, foreign exchange volatility, and longer QCO approval cycle for new products manufactured locally, necessitating higher cost imports to meet client requirement. Further clouding the outlook, geopolitical tensions and the deferral of large project awards present tangible risks to both overall demand and pricing power. We have revised our earnings estimates upward and revised our TP to INR 5,905/sh (based on a 54x P/E multiple), driven primarily by the sustained strength in order inflows.

Q4CY25 Financial Highlights

Revenue stood at INR 35.6bn (+5.7/+7.4% YoY/QoQ, a 4% beat). EBITDA came in at INR 5.5bn (-16.3/+10.1% YoY/QoQ, a beat by 5%). EBITDA margin was at 15.5% (-406/-35bps YoY/QoQ, vs. our estimate of 15.4%). RPAT/APAT stood at INR 4bn (-7.2/-3.6% YoY/QoQ, in-line). However, profitability faces near-term pressure due to the new labor code, and external risks including forex volatility, commodity price swings, geopolitical uncertainties, and competitive pricing dynamics. For CY25 business-wise, revenue grew +12/+6/ 9/+57% from EL/MO/PA/RA respectively, with product offerings continuing to dominate at 79% and the balance from services (13%) and projects (8%).

Robust Order Growth Across all Segments

OI stood at INR 40.9bn (+52%/+19.5%YoY/QoQ) and the backlog (OB) stood at INR 104.7bn as of Dec’25 (0.77x CY25 revenue). Key wins included projects in wind energy, electric vehicle mobility, electronics manufacturing, metals, and power distribution, along with instrumentation solutions for a global player.

Long-term Growth Drivers Intact, Near Term Headwinds Key Challenge

ABB is strategically positioning itself to capitalize on high-growth sectors like data centers, renewables, and electronics, supported by a resilient operational model that spans 23 market segments. However, risks include softer demand growth, global trade barriers, geopolitical tensions, and commodity price volatility.

Standalone Financial Summary (INR mn)

Change in Estimates (INR mn)

Source: HSIE Research (HSIE Results Daily Report – 24 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.