HSIE Institutional Report: Ahluwalia Contracts Feb, 17 2026

Authored By Prime Research | Last Modified: Feb 17, 2026 11:14 AM IST

Muted Execution

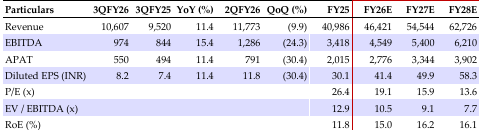

Ahluwalia Contracts (AHLU) reported a revenue/EBITDA/APAT of INR 10.6/1/0.6bn, a miss of 14.2/24.2/30.3%, affected by NGT pollution control restrictions on execution, since major OB (~44%) is concentrated in the NCR region. EBITDA margin stood at 9.2% (+32/-174bps YoY/QoQ, vs our estimates of 10.4%). For FY26, AHLU has revised revenue guidance to +10-15% YoY (earlier 15-20%), and the double-digit EBITDA margin guidance continues. The order book (OB) as of Dec’25 stood at INR 186.8bn (~4.6x FY25 revenue). AHLU is L1 in orders worth INR 24.6bn. New order wins (OI) for 9M/FYTD26 stand at INR 95.6bn (incl. INR 6bn GST). Given the focus on private sector projects, large marquee public projects, pick-up in execution in CSMT/DLF Dahaliyas/ Jewellery Park (Mumbai) projects on the back of progress in obtaining clearances, we expect growth to continue. We have cut our margins/EPS estimates to factor in delayed project start. Given the limited upside to the CMP, we maintain ADD, with a reduced TP of INR 922 (16x Dec-27E EPS).

Ahluwalia Contracts Q3FY26 Financial Highlights

Revenue: INR 10.6bn (+11.4/-9.9% YoY/QoQ, a 14.2% miss). EBITDA: INR 0.9bn (+15.4/-24.3% YoY/QoQ, a 24.2% miss). EBITDA margin: 9.2% (+32/-174bps YoY/QoQ, vs. our estimate of 10.4%). RPAT: INR 550mn (+11.4/-30.4% YoY/QoQ, a miss of 30.3%). The execution in Q3FY26 has been impacted due to GARP pollution control restrictions enforced by NGT. In Q4FY26, execution is affected and could be hampered in Mar’26 due to Holi (NCR contribution to OB stands at ~40%).

With a Robust OB, Execution Becomes the Key Focus

The OB as that of Dec’25 at INR 186.8bn (~4.6x FY25 revenue) comprises 43 ongoing projects, which are expected to be executed in the next 2.5 years. The segment-wise OB classification stood at 44.7/19.7/19.2/7.9/7.7/0.8%, toward residential/ infrastructure/commercial/hospital/institutional and hotels respectively. The sector-wise OB stood at 68.3/20/10.6/1.1%, toward private/center/state and overseas, respectively. Geographically, the OB is exposed to north/west/east/south and overseas (Nepal) at 46.2/28.3/17.7/6.7 and 1.1%. The OB is spread across 15 states in the domestic market. The overall bid pipeline stands at INR 70bn.

Robust Net Cash Position

AHLU is effectively debt-free, with a negligible gross debt of INR 0.2bn and total cash and cash equivalents of over INR 8.4bn, as of Dec’25. 9MFY26 capex stands at INR 1.9bn (FY26/27/28 targeted at INR <3bn respectively).

Standalone Financial Summary (INR mn)

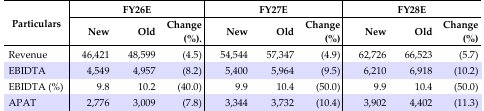

Change in Estimates (INR mn)

Source: HSIE Research (HSIE Results Daily Report – 17 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.