HSIE Institutional Report: Amber Enterprises Feb, 11 2026

Authored By Prime Research | Last Modified: Feb 11, 2026 11:15 AM IST

Healthy Performance Across all Segments

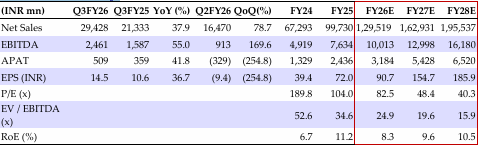

Amber’s Q3FY26 revenue grew 38% YoY to INR 29.43bn, driven by 79% YoY growth in electronics segment. EBITDAM expanded by 90/280bps YoY/QoQ to 8.4%, leading to 55/42% YoY growth in EBITDA/APAT. The company has booked INR 940mn exceptional loss on account of impairment of investment and loan to Shivalik – JV of subsidiary due to financial stress issues. Management noted that RAC channel inventory is close to normal levels, with the industry expected to stay largely flat in FY26, though its consumer durables segment should outperform the market with 13-15% growth. The company expects electronics segment will report double-digit margin in FY27 and targets 2x revenue in railway segment in the next two years, owing to strong order book visibility. It has budgeted INR 8bn in capex for FY26. The company is expected to have a gross block capitalization of INR 11–12bn for FY27. Factoring healthy Q3 performance, we increase our revenue estimates by 4% each, and APAT estimates by 1/3/9% for FY26/27/28E. We maintain BUY with a revised TP of INR 8,520/sh, based on DCF valuation.

Amber Enterprises Q3FY26 Highlights

Revenue grew 38% YoY (2-yr CAGR: 51%) to INR 29.43bn, driven by 79/27/20% YoY growth in electronics segment, consumer durables segment, and railways subsystem segment. Gross margins improved 100bps YoY to 19.7% (-80bps QoQ), while EBITDAM expanded by 90/280bps YoY/QoQ to 8.4%, leading to 55% YoY EBITDA growth. Consumer durables’ EBITDAM declined 30bps YoY to 7.2%. Electronics and railways subsystem witnessed margin expansion of 320bps and 290bps YoY to 10.4% and 14.2% respectively. APAT grew 42% YoY, led by EBITDA growth, increase in other income (up 243% YoY), partially offset by higher minority interest income, depreciation, and finance cost. The company has booked INR 940mn exceptional loss on account of impairment of investment and loan to Shivalik – JV of subsidiary due to financial stress issues.

Earnings Call Takeaways

Management noted that RAC channel inventory is close to normal levels, with the industry expected to stay largely flat in FY26, though its consumer durables segment should outperform the market with 13-15% growth. The company expects electronics segment to report double digit margin in FY27 and target 2x revenue in railway segment in the next two years, owing to strong order book visibility. It has budgeted INR 8bn in capex for FY26. The company is expected to have a gross block capitalization of INR 11-12bn for FY27. Additionally, it highlighted receiving government approval under ECMS for Ascent Circuits and Ascent K-Circuit to manufacture various PCB types; planned capex includes INR 10bn for Ascent Circuits’ to be made in phases (Phase 1: INR 6.5bn over FY26-27, with trial production to start from Q2FY27) and INR 32bn capex for Ascent K-Circuit (INR 12bn in phase 1 expected by Q2FY28). Factoring healthy Q3 performance, we increase our revenue estimates by 4% each, and APAT estimates by 1/3/9% for FY26/27/28E. We maintain BUY with a revised TP of INR 8,520/sh, based on DCF valuation.

Financial Summary

Source: HSIE Research (HSIE Results Daily Report – 11 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.