HSIE Institutional Report: Anthem Biosciences Feb, 06 2026

Authored By Prime Research | Last Modified: Feb 6, 2026 02:17 PM IST

Margin Improvement Neutralized CRDMO Dip

EBITDA was muted (-1% YoY) as shortfall in revenues (-15% YoY; CRDMO declined -19% YoY) was neutralized by a sharp improvement in gross margin (+13 pp YoY to 66.3%) leading to a strong EBITDA margin at 37.1% (+511 bps YoY). The company indicated (1) that it expects mid-teen revenue growth in FY26 as modest growth of 11% YoY in 9MFY26 (global inventory de-stocking due to trade volatility and muted funding environment in CY25) could improve sharply from Q4FY26 led by supply improvement. However, EBITDA/PAT will remain strong with 20%+ growth YoY in FY26. (2) Normalizing in global supplies for existing products, improving global funding environment, and scale-up in recently approved products (four products; TAM of ~USD 10 bn) will help strong performance in FY27 (QoQ lumpiness possible). (3) The company has good visibility in peptide segment with both GLP-1 innovator pipeline projects and other non-GLP peptides. It has one ADC project in late stage of development (in Phase 3) and 6-7 ADC projects in early-stage (with innovators). (4) Specialty ingredients: It expects strong growth momentum on the back of Semaglutide API opportunity in India and RoW markets (tied-up with several India formulation companies; it will remain cost competitive to Chinese suppliers), steady growth in existing products, commercial visibility in probiotics (tied-up with few companies in RoW markets), and scale-up in biosimilars projects. (5) It expects to sustain a gross margin (backward integration) and EBITDA margin (cost optimization and ramp-up in NeoAnthem plant). It saw healthy RFP/RFQ trends and expects higher conversion rate, supported by an improving global funding environment. Factoring in Q3 and outlook, we have tweaked the EBITDA. We retain ADD and revise TP to INR 720, based on 35x Q3FY28E EV/E (implying 52x PE).

Anthem Biosciences Q3 Highlights

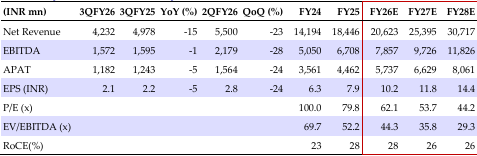

Sales declined 15% YoY to INR 4.23bn. CRDMO (79% of sales) was down 19% YoY to INR 3.33bn. Specialty ingredients (21%) grew 7% YoY to INR 899mn (+7% QoQ). Higher GM was at 66.3% (+13 bps YY), higher staff (+24%), and moderate SG&A (+9%) led to an EBITDA of INR 1.57bn (-1% YoY) and margin was at 37.1% (+511bps). Higher other income (+38% YoY) and depreciation (+70%) led to a PAT^ of INR 1.18bn (-5% YoY).

Con Call Takeaways: CDMO

Capacity utilization: (1) CDMO: (a) Unit 1 (25KL) CDMO at 75%; (b) Unit 2 (300 KL) at 75%; added 76KL; (c) Unit 3 (NeoAnthem) at still to be utilized; and (2) Fermentation (142 KL both at Unit 1 and 2): at 46%. The company has discontinued intermediates outsourcing from China and focused on backward integration for the past few years, which benefitted the gross margin. No new additions in Phase 3 clinical pipeline (at 10); one molecule undergoing USFDA review for transition from Phase 2 to 3. Unit 4: Civil work has started, and majority of capex will be in FY27; capability-wise Unit 4 partially will in small scale molecules move toward commercialization, peptides, Hi-Po API, and oligonucleotides.

Anthem Biosciences Quarterly Financial Summary

Source: HSIE Research (HSIE Results Daily Report – 06 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.