HSIE Institutional Report: Apollo Hospitals Enterprise Feb, 12 2026

Authored By Prime Research | Last Modified: Feb 12, 2026 01:49 PM IST

Strong Q3; Growth and Margin Visbility Intact

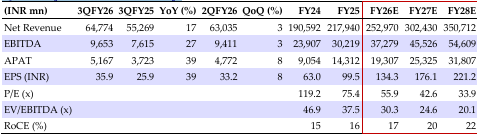

EBITDA (+27% YoY) was 3% ahead of our/consensus estimates, led by 17% YoY sales growth. The hospital business grew 14% YoY (ARPP +11% YoY), HealthCo grew 20% YoY (offline/online sales up 21%/15%), and AHLL grew 20% YoY. Hospital EBITDA grew 18% YoY (margin at 24.8%; +73 bps) and lower Apollo 24/7 spend (-24%) led to a better HealthCo margin. APHS expects (1) existing hospitals: steady growth with improving occupancy and ARPP growth (focus on CONGO-T); margin to see 100bps expansion and cost optimization led support of 80bps for the next few years; (2) expansion over FY26-27 is on track (Pune and Delhi Defense Colony commissioned in Q3FY26, Kolkata, Sarjapur, and Hyderabad in Q1FY27 and Gurgaon in Q2/H2FY27) – total addition of ~1,500 (of which 750 beds will operationalized in FY27 and balance in FY28; it expects to have a drag of ~INR 1.5 bn; (3) HealthCo: to sustain growth momentum and cost controls on Apollo 24/7 spend to help margin expansion, slight delay in digital cash break-even to Q1FY27 from Q4FY26 earlier (due to impact of GST changes in insurance vertical); and (4) AHLL: strong growth and margin improvement. We see growth visibility across – Hospitals: improving occupancy, ARPOB growth, and capacity expansion; HealthCo: steady growth in offline and scale-up in Apollo 24/7; and AHLL: steady growth and margin expansion. Factoring in Q3, we have tweaked EBITDA for FY26/27E at a revised TP to INR 9,200 (26x Q3FY28E EV/EBITDA). BUY stays.

Apollo Hospitals Enterprise Q3 Highlights

Sales grew 17% YoY to INR 64.7bn, with hospitals growing 14% (ARPP +11%), HealthCo and AHLL at 20%. Steady staff (+9%) and higher SG&A (+17%; Apollo 24/7 spend at INR 859 mn -24%) led to an EBITDA of INR 9.65bn (+27%) and 14.9% margin (+34 bps). EBITDA: (1) Hospital: +18% YoY, margin at 24.8% (+73 bps). (2) HealthCo: EBITDA at INR 1.27 bn; Offline: +23% YoY and margin at 7.8% (+12 bps). (3) AHLL: +39% YoY and margin at 10.2% (+142 bps). PAT^ was at INR 5.16bn (+39% YoY).

Operating Metrics: Hospital

ARPP was at INR 180,917 (+11% YoY) and occupancy at 67% (68% YoY). IP/OPD volume grew 4%/ flat YoY. ALOS improved to 3.16 days. Healthco: GMV at INR 5.25 bn (+28% YoY) added 185 stores (7,113 as of Dec-25).

Con Call Takeaways

CONGO specialties saw 6% YoY volume and 16% revenue growth. Hospitals’ growth break-up: 5% volume growth, 4% case mix and 5% price increases. GMV: The company had an impact from discontinued Amazon online channel, GST rate changes impacting insurance vertical, and muted growth IP/ OPD; it expects to see recovery in Q4FY25. GMV (adjusted for Amazon and GST impact) to see ~28% growth in FY26. HealthCo demerger on track; received CCI approval and NCLT hearing to start soon; listing timeline of New Co stays in Q4FY27.

Quarterly Financial Summary

Source: HSIE Research (HSIE Results Daily Report – 12 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.