HSIE Institutional Report: Aptus Value Housing Finance India Feb, 06 2026

Authored By Prime Research | Last Modified: Feb 6, 2026 04:12 PM IST

High Profitability; Moderating Growth

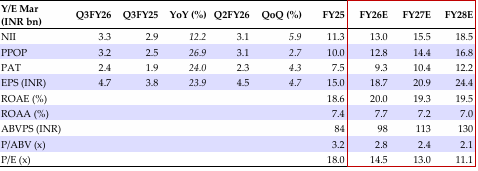

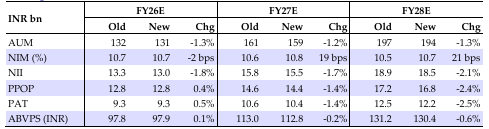

APTUS’s Q3FY26 earnings were marginally below our estimates due to lower AUM growth, partly offset by high assignment income (~16% of PBT). Disbursements growth continued to moderate (+11% YoY; 9% YoY in 9MFY26), leading to lower AUM growth of 20.6% YoY. NIM (calculated) increased by 31bps QoQ due to lower cost of funds. APTUS is gradually seeking customer diversification (floor of INR 0.7mn ticket size), while remaining focused on the LIG, self-employed, rural-based customers. Further, APTUS is accelerating distribution expansion (60-70 branches to be added annually) in Odisha and Maharashtra and high growth pockets in core states to drive loan growth. We expect APTUS to deliver ~20-22% AUM CAGR in the medium term as scalability outside the core products and geographies is likely to remain protracted. We revise our FY26E/FY27E/FY28E earnings estimates to factor in marginally lower loan growth and assignment income and maintain ADD with a revised RI-based TP of INR 320 (implying 2.6x Sep-27 ABVPS).

Increasing Share of Assignment Income, Opex Ratios to Witness an Uptick

Other income grew sharply by 214% YoY due to assignment of portfolio (4.4% of AUM). DA as % of AUM is likely to increase to 6-7% of AUM gradually, as per management. Operating efficiency remained superior to peers with opex to-AUM at 2.8% and C/I at 21%, although it is likely to inch up in the near term with distribution expansion. Cost of funds declined by 39bps QoQ, aiding core spreads. Subsequently, APTUS has reduced the incremental lending rate for home loans by ~50-75bps.

Asset Quality Marginal Deterioration

Asset quality deteriorated marginally QoQ, with GS-II/GS-III clocking in at 4.9%/1.6% (Q2FY26: 4.8%/1.6%) and uptick in early delinquencies (30+ dpd at 6.48% vs. 6.34% in Q2FY26). As per management, the uptick in delinquencies was largely seasonal and is likely to normalize by Q4. Credit costs remained steady (~58bps) with write-offs at ~46bps and largely in line with management guidance of ~50bps.

Growth Initiatives at Play to Revive Growth; Scalability Outside Core Markets Key Monitorable

APTUS’s AUM growth continues to moderate, driven by moderating housing demand, elevated competitive intensity and limited increase in ticket sizes. APTUS is taking initiatives to address these challenges such as focus on higher ticket sizes, distribution expansion, and tweaking lending rates. As highlighted in our company update, APTUS is poised to deliver ~20-22% AUM growth, along with strong profitability (RoE of ~20%).

Aptus Value Housing Finance India Financial Summary (Consolidated)

Change in Estimates

Source: HSIE Research (HSIE Results Daily Report – 06 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.