HSIE Institutional Report: Astral Feb, 06 2026

Authored By Prime Research | Last Modified: Feb 6, 2026 01:57 PM IST

Industry Leading Growth

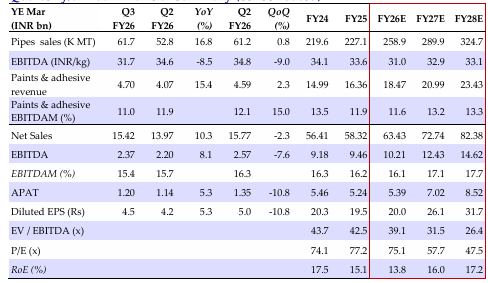

Astral reported revenue growth of 10% YoY in Q3FY26 to INR 15.4bn — plumbing grew 8% YoY while paints & adhesives (P&A) grew 15% YoY. EBITDAM declined 30/90bps YoY/QoQ to 15.4%; however, strong revenue growth led to 8% YoY EBITDA growth. Inventory loss was INR 200–250mn (~2/1.5% of plumbing/consolidated revenue). APAT grew 5% YoY, led by EBITDA. Plumbing volume grew 17% YoY (+1% QoQ), indicating market share gain. NSR declined 8% YoY (-6% QoQ). The company has revised its FY26 plumbing volume growth guidance upward to over 14% (from low double digits). Demand in Q4 has picked up, aided by channel restocking, with January plumbing volume growth exceeding 20% YoY. In bathware, the company aims for an annual revenue growth of 20-25% over the next five years, with current order book staying strong. Management anticipates UK adhesive margin to improve in Q4FY26. Considering in-line Q3 performance, we broadly maintain our estimates. We maintain BUY with an unchanged TP of INR 1,900/sh by valuing the company at 60x Mar-28E EPS.

Q3FY26 Performance

Revenue grew 10% YoY to INR 15.4bn (plumbing grew 8% YoY and P&A grew by 15% YoY). Employee cost and other expenses were up 14/12% YoY. EBITDAM declined 30/90bps YoY/QoQ to 15.4%, leading to 8% YoY EBITDA growth. APAT grew 5% YoY, led by EBITDA. Plumbing volume grew 17% YoY (+ 1% QoQ), indicating market share gain. NSR declined 8% YoY (-6% QoQ). Plumbing EBITDAM declined 25/80bps YoY/QoQ. EBITDA/kg was INR 31.7 vs INR 34.6/34.8 YoY/QoQ. Inventory loss was INR 200-250mn (~2/1.5% of plumbing/consolidated revenue).

Con Call Highlights and Outlook

The company has revised its FY26 plumbing volume growth guidance upward to over 14% (from low double digits). Demand in Q4 has picked up, aided by channel restocking, with January plumbing volume growth exceeding 20% YoY. In bathware, the company aims for an annual revenue growth of 20-25% over the next five years, with current order book staying strong. Management anticipates UK adhesive margin to improve in Q4FY26. The healthy revenue growth in paints from Q3 onward should persist into Q4. Considering in-line Q3 performance, we broadly maintain our estimates. We maintain BUY with an unchanged TP of INR 1,900/sh by valuing the company at 60x its Mar-28E EPS.

Quarterly/Annual Financial Summary (Consolidated)

Source: HSIE Research (HSIE Results Daily Report – 06 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.