HSIE Institutional Report: Aurobindo Pharma Feb, 11 2026

Authored By Prime Research | Last Modified: Feb 11, 2026 11:02 AM IST

Steady US/EU, Pen-G Ramp Up to Improve Margin

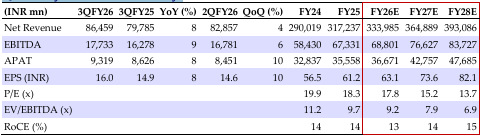

EBITDA grew 9% YoY, which was 4% beat to consensus estimates, as sales increased 8% YoY (US flat QoQ; EU up 27% YoY) and GM improved by 129bps YoY, though this was offset by a 16/15% YoY rise in staff costs/SG&A. Excluding gRevlimid, sales grew 9% YoY and EBITDA growth was at 15% YoY. ARBP indicates (1) to meet its guidance of single-digit growth (ex-gRevlimid) in FY26 and expects to sustain momentum in the coming years, with steady US OSD business (at USD 1bn) through new launches, improvements in injectables (+17% YoY), normalization of Eugia-3 plant supplies, and commercialization of Vizag plant (three products filed and 10+ in process of filing); (2) strong growth in the EU, led by geographical/product expansion and support from scale-up in China plant, with improved EBITDA; (3) ramp-up in its Pen-G plant – utilization improved to 60-70% in Q4FY26 and targets 10k MT in FY27 to support the margin (captive) and external sales (from 6-APA; support from MIP); (4) to sustain EBITDA margins at 20–21% in FY26, with operating leverage supporting margins in subsequent years; (5) scaling up the biosimilar business, with four launches in the EU and stronger traction expected from FY27 and inflection point in FY29 (meaningful contribution); and (6) Lannett acquisition will complement the US OSD business growth; we have not factored in our estimated as transaction is excepted to complete in H1FY27; after factoring in Q3 results, we have tweaked FY26/27E EPS and revised the TP to INR 1,280 (16x Q3FY28E). ADD stays, led by improvements in the US base business, steady EU growth, ramp-up in Pen-G/ China/US plants, and gradual biosimilar scale-up, all likely to drive steady mid-to-long-term growth.

Aurobindo Pharma Q3 Highlights

Sales grew 8% YoY to INR 86.4bn as the US (43% of sales) grew 1% QoQ to USD 420mn (-3% YoY), led by volume growth. EU sales (31%) grew 27% YoY. ARV sales (4%) grew 22% YoY, and API (11%) declined 4% YoY. Higher GM at 59.7% (+129 bps YoY), higher staff/SG&A (+16/15%), and lower R&D (-9%) led to an EBITDA of INR 17.73bn (+9% YoY) and margin of 20.5% (+11 bps). Higher other income (17%) and depreciation (11%), and lower interest (-22%) resulted in a PAT^ of INR 9.32bn (+8% YoY).

Con Call Takeaways

US OSD: Sales were up QoQ, led by volume growth. China plant: ramping up to support the EU supplies. Dayton plant: Commercialized and contribution to start in FY27E. Biosimilars: (1) launched Bevqolva (Bevacizumab) in the UK, Dazublys (Trastuzumab) in Lithuania, and supplies initiated to France and Germany for upcoming launches. (2) Received approval for Dyrupeg (pegfilgrastim) in Canada. (3) Denosumab filing delayed due to extended validation requirements. (4) Targets Bevacizumab filing in the US in H2CY26.

Quarterly Financial Summary

Source: HSIE Research (HSIE Results Daily Report – 11 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.