HSIE Institutional Report: Bajaj Electricals Feb, 10 2026

Authored By Prime Research | Last Modified: Feb 10, 2026 01:31 PM IST

Another Weak Performance; 18 Quarter Low Margin

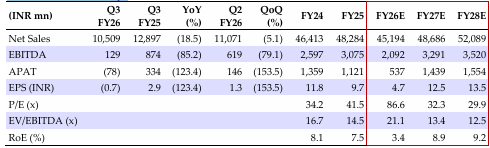

Revenue was down 19% YoY to INR 10.51bn (2-year CAGR: -8%), primarily due to 25% de-growth in consumer products segment (74% revenue mix), while lighting segment (26% revenue mix) grew by 9%. Consumer products segment EBIT margin declined 960bps YoY to negative 4.6% (-550bps QoQ). Lighting segment EBIT margin improved 470bps YoY to 6.7% but down sequentially 110bps. EBITDAM declined 550bps YoY to 1.2%, hitting an 18-quarter low, leading EBITDA decline of 85% YoY and negative APAT. Management indicated that consumer products witnessed de-growth across categories due to high channel inventory levels, while margins were impacted by operating de leverage and discounts offered. It highlighted that channel inventory has been broadly normalized, with the exception of summer products, which should normalize as seasonal demand strengthens. The company has initiated a review of key processes to enhance cost efficiency and margin improvement. Factoring weak Q3 performance, we cut our revenue estimates by 7% each and APAT by 43/10/9% for FY26/27/28E respectively. We maintain a REDUCE rating with a lowered target price of INR 375/share, based on 28x Mar-28E EPS.

Bajaj Electricals Q3FY26 Highlights

Revenue down 19% YoY to INR 10.51bn (2-year CAGR: -8%), primarily due to 25% de-growth in consumer products segment (74% revenue mix), while lighting segment (26% revenue mix) grew by 9%. Gross margins declined by 80bps YoY to 30.4% (-140bps QoQ). Consumer products segment’s EBIT margin declined 960bps YoY to negative 4.6% (-550bps QoQ). Lighting segment’s EBIT margin improved 470bps YoY to 6.7% but was down sequentially 110bps. EBITDAM declined 550bps YoY to 1.2% ( 440bps QoQ), hitting an 18-quarter low owing to lower gross margin, increase in other expenses (up 380bps YoY), and employee costs (up 100bps YoY), driven by negative op-leverage. While in absolute terms, employee costs declined 8% YoY, while other expenses remained flat YoY. So, EBITDA declined 85% YoY and APAT turned negative.

Earnings Call Takeaways and Valuation

Management indicated that consumer products witnessed de-growth across categories due to high channel inventory levels, while margins were impacted by operating de leverage and discounts offered. It highlighted that channel inventory has been broadly normalized, with the exception of summer products, which should normalize as seasonal demand strengthens. The company has initiated a review of key processes to enhance cost efficiency and margin improvement. It noted rising commodity costs as an ongoing challenge; however, the company implemented price hikes of 2-5% to offset these increases, covering the majority of the commodity cost escalation. Factoring in weak Q3 performance, we cut our revenue estimates by 7% each and APAT by 43/10/9% for FY26/27/28E respectively. We maintain a REDUCE rating with a lowered target price of INR 375/share, based on Mar-28E EPS.

Financial Summary

Source: HSIE Research (HSIE Results Daily Report – 10 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.