HSIE Institutional Report: Bajaj FinServ Feb, 06 2026

Authored By Prime Research | Last Modified: Feb 6, 2026 09:44 AM IST

Consistently Delivering

Bajaj Finserv’s 9MFY26 performance was strong across all operating businesses. BAGIC reported 10% YoY GDPI growth, with profitability slightly ahead of estimates on the back of higher realized capital gains and favourable TP loss ratio. BALIC continued to showcase benefits of strategic shifts undertaken, with 52% VNB growth and a 540bps margin improvement, despite 2% decline in APE. Bajaj Finance delivered adjusted AUM growth (+22% YoY) though PAT declined by 6% YoY due to accelerated provisioning of INR 14bn (0.3% of gross advances), given the implementation of minimum LGD floor across businesses. With the NBFC business maintaining sector leadership, the improving trajectory in insurance is expected to drive an operational turnaround and a 500bps increase in SOTP contribution, supporting a re-rating. We maintain BUY with the SOTP-based TP of INR2,510 (78% currently contributed by the flagship NBFC business).

General Insurance (12% of SOTP) Capital Gains and Favourable Loss Ratio

BAGIC reported 10/7% YoY growth in its GDPI and PAT. GDPI growth continued to be led by strong growth in motor TP (+29% YoY). However, reported PAT was ahead of our estimate, higher capital gains by INR3.0bn and lower overall loss ratios at 74.1% (9MFY25: 78.2%), mainly in Motor TP and crop businesses, partly offset by higher expenses.

Life Insurance Business (10% of SOTP) – Strategic Shift a New Normal

BALIC’s APE for Q3 grew by 26% YoY (H1FY26: -8% YoY), value of new business (VNB) witnessed healthy growth (9M:+52% YoY) as the VNB margin clocked in at 16.4% (+540bps YoY). As highlighted in our insurance thematic report, we believe FY26E will show a material turnaround in profitability metrics, with its revised product construct, balanced segmental mix, and rationalizing of costs. We were positively surprised with VNB margins due to lower impact of GST disallowance (Q3FY26:230bps, Q2FY26:223bps) (~450bps drag full year guidance). Given strong 9M performance, we revise our FY26E VNB margin estimates upward to ~17.8%.

NBFC Business (78% of SOTP) – Accelerated Provisions Dent Earnings

BAF Q3FY26 PAT declined by 6% YoY due to accelerated provisioning of INR 14bn (0.3% of gross advances), given the implementation of minimum LGD floor across businesses. Adjusted for this one-off, operating performance remained steady with AUM growth of 22% YoY, steady NIMs (~9%), marginal normalization in credit costs (1.92%), and robust profitability (RoE of 19.6%). Management guided credit costs in FY27 to sub-1.8%, along with pick-up in the MSME segment. While BAF’s credit costs normalization has been protracted compared to historical trends, overall profitability is likely to remain best-in-class along with healthy loan growth, driving premium valuation vs. peers. We maintain BUY with a RI-based TP of INR 1,070 (implying 4.5x Sep-27 ABVPS; 23x Sep-27 EPS).

Insurance Businesses to Drive Incremental Re-Rating

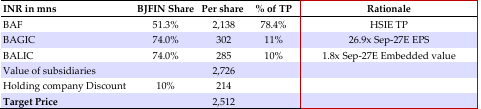

With the flagship NBFC business already commanding sector leadership, we believe that the potential turnaround in the insurance businesses is likely to drive an incremental re rating for BJFIN (SOTP contribution likely to improve by 500bps). We retain BUY with a revised SOTP-based TP of INR2,510.

SOTP

Source: HSIE Research (HSIE Results Daily – 06 Feb 26 – HSIE-202602060713371815208.pdf)

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.