HSIE Institutional Report: Berger Paints Feb, 06 2026

Authored By Prime Research | Last Modified: Feb 6, 2026 12:51 PM IST

Growth Pangs Persist

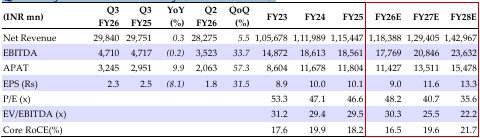

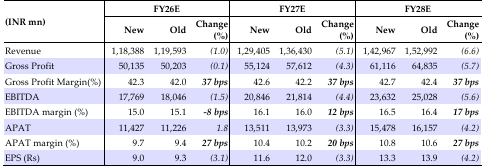

Extended monsoon and a shortened festive season kept BRGR’s consolidated revenue flat YoY at INR29.8bn (HSIE: INR30.5bn). Volume/value growth stood at 8.5/0.4%. Management expects this gap to narrow but persist in the 4-5% range as mix continues to shift toward high volume-low value products like economy emulsion, textures, and tile adhesives. Note: the FY25 price corrections (2-2.5%) impact is now behind (anniversarized in Jan-26). GM expanded by 143bps YoY to 43.1% (HSIE: 42%) due to improved product mix and stable RM prices. However, EBITDAM remained stable YoY at 15.8% (HSIE: 14.8%), constrained by negative operating leverage and sustained brand investments. Management’s EBITDAM guidance of 15-17% stays. While EBITDA stood flat YoY at INR 4.71bn (HSIE: INR 4.52bn), APAT grew by 9.7% YoY to INR 3.25bn (HSIE: INR 2.77bn), due to higher JV profits. We have cut our EPS estimates by ~3/4% for FY27/28 respectively to account for lower growth but retained ADD with a DCF-based TP of INR540/sh (implying 41x Mar-28 P/E).

Berger Paints Q3FY26 Highlights

Consolidated/standalone revenue stood flat YoY at INR29.8/25.9bn (HSIE: INR30.5/26.3bn). Growth was impacted by the extended monsoon and a shortened festive season. Volume/value growth stood at 8.5/0.4%. Management expects this gap to narrow but persist in the 4-5% range as mix continues to shift toward high volume-low value products like economy emulsion, textures, and tile adhesives. Note: FY25 price corrections (2-2.5%) impact is now behind (anniversarized in Jan-26). In deco, CC delivered robust growth and wood coatings segment reported strong double-digit growth. Dealer network expansion continued in Q3, while urban initiatives remain on track. In industrial, automotive posted mid-single digit value growth, aided by GST 2.0 reforms, whereas protective (including GI) remained muted. In international business, Bolix Poland reported strong topline and EBITDA growth, BJN Nepal was impacted by political disruption, and STP faced topline pressure due to a temporary shutdown at the Jamshedpur plant. Consolidated GM expanded by 143bps YoY to 43.1% (HSIE: 42%) due to improved product mix and stable RM prices. However, EBITDAM remained stable YoY at 15.8% (HSIE: 14.8%), constrained by negative operating leverage and sustained brand investments. EBITDAM guidance of 15-17% stays. While EBITDA stood flat YoY at INR 4.71bn (HSIE: INR 4.52bn), APAT grew by 9.7% YoY to INR 3.25bn (HSIE: INR 2.77bn) due to higher JV profits. Net cash position stood at INR9.18bn.

Outlook

The paint sector continues to face significant growth challenges as it navigates subdued demand conditions, further compounded by seasonal headwinds and intense competition. We cut our EPS estimates by ~3/4% for FY27/28 respectively to account for lower growth but retained ADD with a DCF based TP of INR540/sh (implying 41x Mar-28 P/E).

Berger Paints Quarterly Financial Summary (Consolidated)

Change in Estimates (Consolidated)

Source: HSIE Research (HSIE Results Daily Report – 06 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.