HSIE Institutional Report: BSE Feb, 10 2026

Authored By Prime Research | Last Modified: Feb 10, 2026 11:51 AM IST

Open Free Demat Account

Strong Growth Momentum

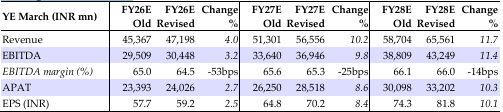

BSE delivered a strong quarter with revenue rising 16.4% QoQ and 60.8% YoY, led by sustained traction in transaction revenue and strong book-building and listing fees. Adjusted PAT (ex-labor laws provision, additional SGF, and impairment) came in at INR 6.5bn vs our estimate of INR 6.2bn. Transaction revenue, contributing 77% of total revenue, surged 26% QoQ on continued gains in options market share and recovery in industry volumes. BSE’s options premium market share improved to 26.8% in Q3FY26 vs 24.4% in Q2, with premium ADTV of INR 195bn (+30% QoQ), and further rose to 30% in Jan-26. Adjusted EBITDA margin expanded 97bps QoQ to 65.6% (reported 62.5%), while SGF contribution stood at INR 0.46bn (~5% of transaction revenue), higher than the mandated threshold. Colocation revenue was stable at INR 0.48bn vs INR 0.46bn in Q2, and BSE plans to add 20 racks by Q4, taking the total to 500 to support future growth. The share of longer-dated options rose to 5%, with management targeting further growth through higher institutional participation. We raise EPS estimates by 8-10% on better volumes, projecting robust FY25–28E revenue/EPS CAGRs of ~30/36%. We maintain an ADD rating with a revised TP of INR 3,310, based on 42x core FY28E PAT plus CDSL stake and net cash ex SGF; BSE stock trades at 43x/37x FY27/28E EPS.

BSE Q3FY26 Highlights

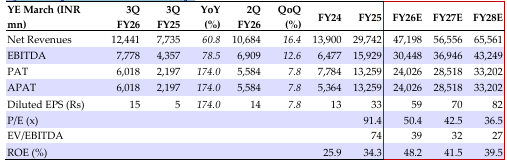

Revenue grew 16.4/60.8% QoQ/YoY to ~INR 12.4bn (vs our estimates of ~INR 12.4bn), led by +20.0/78.4% QoQ increase in transaction/book building income, supported by an increase in all other revenue segments other than cash segment income (-3.7% QoQ). The transaction revenue growth was driven by the derivatives segment (25.6% QoQ) and Star MF grew marginally by 4% sequentially. The EBITDA margin stood at 62.5% vs 64.7% in Q2. Margin contraction was led by 31.7/27.5/18.2/17.5/12.7% increase in employee cost/SEBI regulatory fees/other expenses/clearing fees and technology fees respectively. SGF contribution in the quarter stood at INR 0.46bn and reported PAT stood at INR 6.02bn vs our PAT estimate of INR 6.23bn. The derivative UCC stood at 9.5mn vs 8.7mn in Sep 2025 and 567 registered members.

Outlook

We expect revenue growth of +58.7/19.8/15.9% and EBITDA margins of 64.5/65.3/66.0% in FY26/27/28E respectively. Revenue CAGR of 30.1% over FY25-28E assumes derivatives revenues of INR 30/37/44bn in FY26/27/28E. Core PAT CAGR over FY25-28E is at 35.8%.

BSE Quarterly Financial Summary

Change in Estimates

Source: HSIE Research (HSIE Results Daily Report – 10 Feb 26 )

Disclaimer

At HDFC SKY, we take utmost care and due diligence in curating and presenting news and market-related content. However, inadvertent errors or omissions may occasionally occur.

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.