HSIE Institutional Report: CemIndia Projects Feb, 06 2026

Authored By Prime Research | Last Modified: Feb 6, 2026 04:44 PM IST

Muted Execution

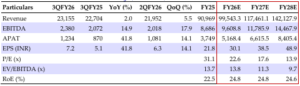

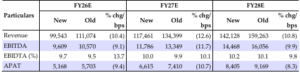

CemIndia Projects’ (CPL)revenue/EBITDA/APAT was a miss on our estimates by 12.6/8.4/4.7% respectively, majorly attributed to delay in execution towards Vadhavan port project (Order Value: INR 10bn). With an OI of INR 35.4bn in Q3FY26 (9MFY26: INR 97.3bn), the OB as of Dec’25 stood at INR 218.8bn (~2.4x FY25 revenue). OB from group entities is ~27%. CPL management has guided for 15% revenue growth, 10% EBITDA margin, and OI of ~INR 150bn (20% from group entities) in FY26, with current bid pipeline at INR 250bn. The OB is well diversified, offering a natural hedge against any slowdown in specific business segments and targeting maritime, industrials, urban infra/MRTS/airports, roads, hydro, data centre, and other segments. CPL continues to focus on bidding for only higher ticket-sized orders, expanding into new segments such as data centres and ports based on Adani group requirements, and improving execution of projects in hand. While 9MFY26 execution was impacted by delay in execution of Vadhavan port project due to local issues (Q3FY26 revenue impact: INR2-3bn), uptick in metro and data centre projects provides support. We have tweaked our estimates lower, reiterate BUY, with a reduced TP of INR 834/sh (18x Dec-27E EPS, rollover from Sep-27 to Dec-27).

Q3FY26 Financial Summary

Revenue: INR 23.2bn (+2/+5.5% YoY/QoQ, 12.6% miss). EBITDA: INR 2.4bn (+14.9/+17.9% YoY/QoQ, 8.4% miss). EBITDA margin: 10.3% (+115/+108bps YoY/QoQ, vs. our estimate of 9.8%). APAT: INR 1.2bn (+41.8/14.1%, 4.7% miss).

Growth in OB, Supported by Expansion in Marine, Airports, and Data Centers

As of Dec-25, client-wise, the OB shows diverse distribution among government, private, and PSU accounting for 44/48/4%. Business-wise, the OB is spread across maritime/industrials/urban infra (including MRTS and airports)/hydro/data center/highway/specialist engineering and water at 33.9/19.7/27/5.5/8.3/1.4/3.3/0.9% respectively. CPL plans to add more complex projects to its portfolio with increased focus on marine, airports, and data centers (civil), which it considers highly profitable.

Comfortable Balance Sheet

The net debt-equity stands at 0.26x as of Dec’25 (Sep/June’25: 0.25/0.34x), with gross debt at INR 9.2bn. CPL guides for INR 3bn capex in FY26 (9MFY26: INR 2bn deployed). Receivables from Bangladesh continue to be at normalized levels, with completion expected by Jun-26.

Consolidated Financial Summary (INR mn)

Change in Estimates (INR mn)

Source: HSIE Research (HSIE Results Daily Report – 06 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.