HSIE Institutional Report: Century Plyboards India Feb, 06 2026

Authored By Prime Research | Last Modified: Feb 6, 2026 04:08 PM IST

Strong all Round Performance

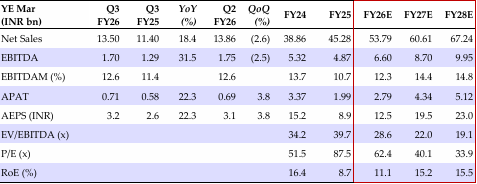

Century’s revenue grew 18% YoY to INR 13.5bn, led by healthy growth in MDF segment (up 19% YoY), ply segment (up 15% YoY), laminates segment (up 10% YoY) and particle board (up 84% YoY). MDF/ ply/ laminates/ particle board volume grew 13/14/115% YoY, while laminates declined 8% YoY. Healthy revenue traction and improved margins drove a 32/22% YoY rise in EBITDA/APAT. The company has broadly maintained its guidance for FY26. It also plans major plywood expansion of more than 50% by FY29 to cut outsourcing. MDF capacity is likewise set to expand more than 50% by FY29. Factoring in Q3 performance, we broadly maintain our revenue and EBITDA estimates. However, we trim our APAT estimates by 4/8% for FY27/28E, respectively, to account for the new announced ply and MDF expansions, leading to increase in our depreciation and interest cost projection. We value Century Ply using SOTP—ex-particle board business at 40x Mar-28E EPS and the upcoming particle board business at 2x capital employed in Mar-28E—to arrive at a TP of INR 935/sh.

Century Plyboards India Q3FY26 Highlights

Revenue grew 18% YoY (+19% QoQ) to INR 13.5bn, led by healthy growth in MDF segment (up 19% YoY), ply segment (up 15% YoY), laminates segment (up 10% YoY), and particle board (up 84% YoY). MDF/ply/laminates/particle board volume grew 13/14/115% YoY, while laminates declined 8% YoY. MDF/ ply/ laminates operating margin expanded by 130/350/330 bps YoY to 12.1/15.1/ 7.7%, while particle board margin declined 450bps YoY to 0.4%. Healthy revenue traction and improved margins drove a 32/22% YoY rise in EBITDA/APAT.

Con Call KTAs and Outlook

The company has reaffirmed its FY26 guidance, projecting 13% revenue growth with 12-14% EBITDAM in ply; 25% revenue growth with 14-15% EBITDAM in MDF; 15-17% revenue growth with high single-digit EBITDAM by Q4-end in laminates; and 40% revenue growth with low single-digit EBITDAM in particleboard. For FY27, laminate revenues are expected to grow by 20% with double-digit EBITDA margins, while particleboard margins are projected to reach ~15% by Q4FY27. It also plans major plywood expansion by more than 50% by FY29 to cut outsourcing— particularly in Sanik MR (water-resistant) ply. MDF capacity is likewise set to expand more than 50% by FY29. Factoring in Q3 performance, we broadly maintain our revenue and EBITDA estimates. However, we trim our APAT estimates by 4/8% for FY27/28E, respectively, to account for the newly announced ply and MDF expansions, leading to an increase in our depreciation and interest cost projection. We value Century Ply using SOTP— ex-particle board business at 40x Mar-28E EPS and the upcoming particle board business at 2x capital employed in Mar-28E—to arrive at TP of INR 935/sh.

Quarterly/Annual Financial Summary (Consolidated)

Source: HSIE Research (HSIE Results Daily Report – 06 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.