HSIE Institutional Report: Cummins Feb, 06 2026

Authored By Prime Research | Last Modified: Feb 6, 2026 10:16 AM IST

Marginal Miss; Strong Outlook

Cummins India Ltd (CIL) reported muted financial performance in absence of Powergen Data Centre orders, with revenue/EBITDA/APAT missing our estimates by 5/4/5%. Strong FY26 double-digit revenue growth guidance, sustaining/improving Q3FY26 gross margins for the remainder of FY26, and robust underlying demand commentary by the management were some of the positives. While exports were a bit muted, CIL remains positive on domestic demand whilst navigating cautiously through geopolitics and end markets exports demand. Exports were also impacted by inventory corrections. Despite better availability of Powergen nodes from peers and rising competitive intensity, CIL has been able to hold on to the prices and maintain gross margins, owing to cost controls and mix. The company has multiple tailwinds, namely, strong data centre demand, capex cycle recovery, revival in industrials and exports, strong upcoming residential and commercial real estate deliveries, and support for manufacturing policies. CIL remains a play on data centre and capex recovery. We have marginally recalibrated our estimates lower to factor in delays in industrial recovery. We maintain BUY, with a revised SOTP of INR 5,483 (54x Dec-27 EPS roll over).

Q3FY26 Financial Highlights

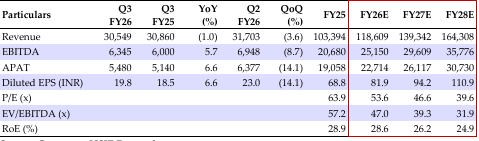

Revenue: INR 30.5bn (-1/-3.6% YoY/QoQ, miss by 5.2%). Domestic sales: INR 25.4bn (-2/-2% YoY/QoQ) and export of INR 4.7bn (+2/ 14% YoY/QoQ). EBITDA: INR 6.3bn (+5.7/-8.7% YoY/QoQ, miss by 3.8%). EBITDA margin came at 20.8% (+132/-115bps YoY/QoQ) vs est. of 20.5%. Other income: INR 1.4bn (+15/-29% YoY/QoQ). APAT: INR 5.5bn (+6.6/-14.1% YoY/QoQ, a 4.6% miss).

Pricing Stable Despite Competitive Intensity, Owing to Strong Demand

In Q3FY26, the domestic power gen revenue stood at INR 10.7bn (-16/-20% YoY/QoQ), distribution at INR 9.4bn (+26/+18% YoY/QoQ), industrials at INR 4.6bn (-9/+20% YoY/QoQ). CIL is witnessing increased competition in CPCB4+ segment and high HP nodes but believes that pricing has settled now and is managing gross margins through the mix. BESS solutions, which is a new market segment but may take time to establish as new growth driver, albeit inquiries continue to pour in, indicating market interest with pick up expected from FY27.

Powergen Demand Healthy, Distribution Highest Ever Quarter

Powergen segment ex of data center (no data center revenue for Q3FY26 as it got booked in Q2FY26) grew in double digits, driven by strong demand in realty, manufacturing, and infra. Industrial segment’s performance was muted by extended rains, slow railways, and mining orders. Distribution growth is fueled by increasing on ground presence and upgrades and with CPCB 4+ 2-yr warranty period ending start of Jul-26, after market sales get further augmented. CIL is expecting double-digit growth in FY26/27, supported by sustained growth in power gen and focus on quick commerce and data center.

Standalone Financial Summary

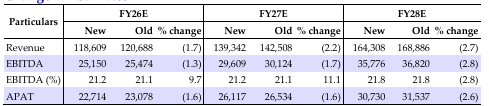

Change in Estimates

Source: HSIE Research (HSIE Results Daily – 06 Feb 26 – HSIE-202602060713371815208.pdf)

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.