HSIE Institutional Report: Dilip Buildcon Feb, 11 2026

Authored By Prime Research | Last Modified: Feb 11, 2026 11:48 AM IST

Muted Execution; Record High OB

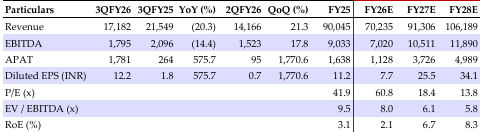

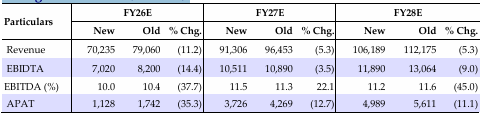

Dilip Buildcon (DBL) reported revenue/EBITDA/APAT beat/(miss) of -11.4/ 12.6/-18% respectively. DBL has cut FY26 revenue guidance from INR 80bn to INR 70-75bn, with EBITDA margin of 10% and has surpassed its order inflow (OI) target of INR150bn. It expects strong INR 100bn in revenue for FY27 on the back of strong opening order book with EBITDA margin expected to improve to 12-13%. Capex is expected to be stable (INR 1bn annually), focused mainly on replacement needs. FYTD OI stands at INR 175.7bn while the OB stood at INR 293.7bn. NHAI awarding is expected to pick up in FY27. DBL has divested 26/24.99% equity stake in 7/11 HAM projects to Alpha Alternatives (AA). The balance 13 assets are under construction. From the combined AA/Shrem platform, DBL expects INR 0.8/10.2/11.98/5.9/5.9bn in cash/InvIT units by Q4FY26/27/28/29/30. Given the slower execution and back ended order booking, we have cut our FY26/27/28 EPS estimates. We retain ADD with an increased SOTP-based TP of INR 545 (12x Dec-27E EPS, 1.1x P/BV HAM equity investment).

Dilip Buildcon Q3FY26 Financial Highlights

Revenue: INR 17.2bn (-20.3/+21.3% YoY/QoQ, a 11.4% miss); EBITDA: INR 1.8bn (-14.4/+17.8%, YoY/QoQ, a 12.6% miss); EBITDA margin: 10.4% (+72/-30.6bps YoY/QoQ), vs. our estimate of 10.6%. RPAT: INR 6.1bn (+597.8/+1395.8% YoY/QoQ)—due to exceptional income on monetization of assets and implementation of labor code. APAT: INR 0.34bn (+28/+255% YoY/QoQ, a miss of 18%).

Uptick in Order Inflows

DBL OB at INR 293.7bn as of Dec’25 is 3.3x of FY25 revenue. OI has surpassed management expectation in FY26 of INR 150bn (INR 175.5bn won FYTD). OB comprises 86/14% of EPC/HAM respectively. The OB is well diversified, with exposure across mining/ metro/tunnel/bridges/optical fiber/renewables/road/irrigation/water/ transmission at 20/4/6/6/3/18/19/16/2/6% respectively.

Balance Sheet Net Cash Status by FY28

Amid lower OI and revenue degrowth, the net cash status has been extended to FY28 (from FY27). Total equity requirement for 13 road HAM, 1 ERCP-HAM, BOT-ZOTL, solar, transmission projects stands at INR 47bn, of which INR 17.8bn is invested as of Dec’25. The balance equity investment of INR 29.2bn (INR 0.8/12.9/11.3/1.5/0.5bn) is expected to be invested in Q4FY26/27/28/29/30. The standalone equity/net debt and net DE ratio stood at INR 67.5/21.5bn and 0.32x as of Dec’25 (Sep’25: 0.45x).

Standalone Financial Summary (INR mn)

Change in Estimates (INR mn)

Source: HSIE Research (HSIE Results Daily Report – 11 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.