HSIE Institutional Report: Divis Laboratories Feb, 12 2026

Authored By Prime Research | Last Modified: Feb 12, 2026 01:01 PM IST

Steady Q3; Visibilty of Growth and Margin Stays

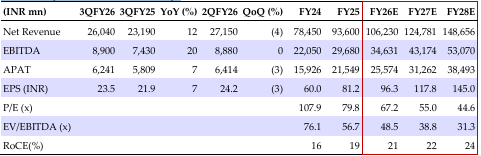

EBITDA (+20% YoY) was 4% ahead of our/consensus estimates, driven by steady sales growth (+12% YoY; CS grew 13% YoY, generic API +9% and Nutraceutical +26%) and GM improvement (+347 bps YoY to 63.7%). This led to EBITDA margin of 34.2% (+214 bps YoY). Divi’s highlighted (1) GLP-1 capacity build-up is on track. It has already commissioned pilot plant and its commercial large scale SPPS capacity is under validation for one customer; (2) in peptide chemistry, the company continues to advance across value chain (protected amino acids and fragments) to support various innovative projects; apart from GLPs, it is also focusing on molecules for indications like anti-inflammatory, psoriasis, and CVS. The company is working on backward integration for peptide molecules (up to resins); (3) it is engaging in several RFPs and few molecules are expected to move closer to commercial stage in near term; (4) its three dedicated capex projects (for three molecules; capex worth of ~INR 20 bn) is expected to enter commercial phase in CY27; (5) Unit 3 (Kakinada) is effectively used for KSM (backward integration for Unit 1 and 2) and transfer of more KSMs is under progress. This helping in freeing up capacity in its cGMP approved Unit 1 and 2. It is evaluating the phase 2 expansion (initial plans for four manufacturing blocks); and (6) it continues to see pricing pressure in generic API business, which it sees as getting offset by volume growth. We see strong sales growth visibility (17% CAGR over FY25–28E), with improved profitability (EBITDA/PAT CAGR 21%) on back of multiple growth levers like GLP-1 supply opportunity, scale-up in contrast media, ramp-up in Kakinada plant, commercialization of three dedicated capex, and gradual pick up in generic API and steady Nutraceutical business. We reiterate BUY with a TP to INR 7,630, based on 39x Q3FY28E EV/EBITDA (implying 55x PE).

Divis Laboratories Q3 Highlights

Sales grew 12% YoY to INR 26.04bn. Custom synthesis (57% of sales) grew by 13% YoY to INR 14.84bn (-2% QoQ), Generic API (35%) grew 9% YoY to INR 9.05bn, and Nutraceutical (8%) grew 26% YoY to INR 2.14bn. Higher GM at 63.7% (+347 bps YoY), higher staff (+24%), and SG&A (+13%) led to an EBITDA of INR 8.9bn (+20% YoY) and margin of 34.2% (+214bps). Lower other income (-4%) and higher depreciation (+17%) led to a PAT of INR 5.83bn (-1% YoY). Adjusted for one-offs, PAT^ was at INR 6.24bn (+7%).

Con Call Takeaways

For 9MFY26, growth in cc terms was at 8.6%. Export was at 89% of sales (grew 15% YoY) and export to the US/EU was at 73% of sales (up 11% YoY). It expects operating environment for raw material pricing to remain stable over the next six months and freight rates to remain stable in the near term. Its China de-risking strategy (material procurement from India was at ~70%) will focus on minimizing impact from material price surge due to China’s removal of export tax rebates (from Apr-26). As of Dec-25, cash/equivalent was at INR 36.86 bn, CWIP was at INR 23.94 bn, asset addition at INR 7.76 bn, receivable at INR 26.37 bn, inventory at INR 36.67 bn.

Quarterly Financial Summary

Source: HSIE Research (HSIE Results Daily Report – 12 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.