HSIE Institutional Report: Eicher Motors Feb, 11 2026

Authored By Prime Research | Last Modified: Feb 11, 2026 10:45 AM IST

Demand Momentum Sustains Even Post Festive Season

Despite the company’s “volume over margin” strategy, we have seen the company’s standalone EBITDA margin expand to a seven-quarter high. While operating leverage played a big part, the company’s value engineering and cost reduction efforts are also aiding the margin expansion. Demand momentum continues post the key festive season and management’s visibility of sustained demand momentum in the medium term has led to a brownfield capacity expansion plan of increasing capacity by almost 1/3rd. We also expect that the company’s efforts of the last few years as well as continued efforts in international markets to pay off, once global macro turns more favorable. We value the company at 29x Dec-27 EPS, and along with the value of VECV (INR 688), we achieve a TP of INR 7,721, and maintain our ADD rating.

Standalone Performance

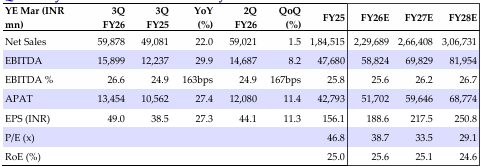

EBITDA margin at 26.6% improved 162bps YoY and 167bps QoQ, 191bps above our estimate and 152bps above Bloomberg consensus estimate. The good performance was on the back of higher operating leverage and lower marketing spends. Revenue at Rs.59.9bn grew 22% YoY and 1.5% QoQ, led entirely by volumes.

VECV Performance

VECV revenue grew 21.0% YoY and 15% QoQ to INR 70.2bn, with EBITDA margin of 9.3% (up 51bps YoY and 144bps QoQ). PAT grew 12.3% YoY to INR 3.38bn.

Demand Momentum Still Strong

Management indicated sustained retail traction with higher bookings and conversions. Additionally, international markets too are well poised, aided by recent new launches. While it expects the domestic 2W industry to grow in high single digits in FY27, it expects the company to outperform. It hinted at new products lined up for FY27.

Capacity Expansion

It is seeking to expand capacity of Royal Enfield bikes from the current 1.45mn units p.a. to 2mn units p.a. by FY28, for which it will invest INR9.58bn over the next two years. This expansion is on the back of management’s visibility of sustained demand momentum in the medium term. It is also working with vendors to ensure they too increase capacity so as to fulfill the company’s orders seamlessly. At VECV too, management is in early consideration of capacity increase since the capacity is 85-90% utilized.

Other Key Highlights

1) Rate of recovery has been good for the 650cc segment, which was impacted due to higher GST rates. (2) Blended price hike of 0.5% taken in Jan and along with value engineering efforts should help soften higher commodity cost impact, going forward. (3) Rural and semi urban markets are growing well, though even urban markets are making a comeback, aided by income tax cuts. (4) Age profile of the ‘Hunter’ customer is moving downward as the 23-24 year group now forms 40% of the buyer mix, vs 34-35% which was there pre-GST rate cuts.

Eicher Motors Quarterly/Annual Financial Summary

Source: HSIE Research (HSIE Results Daily Report – 11 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.