HSIE Institutional Report: Eureka Forbes Feb, 06 2026

Authored By Prime Research | Last Modified: Feb 6, 2026 05:52 PM IST

A One Off Slow Quarter; Growth to Pick Up

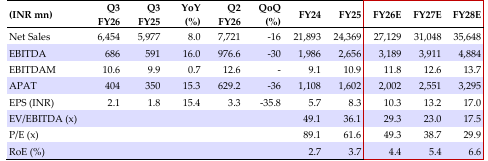

Eureka’s revenue growth slowed down to 8% YoY in Q3, owing to slowdown in water purifier sales post festive and high channel inventory impact. However, management highlighted it has gained market share in water purifier category. Robotic, water softeners and air purifiers (grew 3x YoY) delivered healthy growth. Service business momentum builds up with third successive quarter of double-digit AMC bookings growth. EBITDA margin expanded by 70bps YoY owing to improved gross margin to 10.6%, leading to 16/15% growth in EBITDA/APAT. The management highlighted channel inventory pressures have eased across channels, except e-com, which will be normalize by Q4FY26 end. Management guided Q4 revenue growth will be higher than 11% delivered in 9MFY26. Considering a muted Q3 performance and continued elevated inventory in e-com channel, we have trimmed our revenue estimates by 2% each for FY26-28E and APAT estimates by 3/2% for FY27/27E, respectively, while broadly maintaining for FY28E. We maintain BUY with an unchanged TP of INR 830/sh, valued at 45x Mar-28E AEPS (excluding non-cash intangible amortization and 50% of performance-based ESOP expenses).

Eureka Forbes Q3FY26 Highlights

Revenue growth slowed down to 8% YoY in Q3, owing to a slowdown in water purifier sales post festive and high channel inventory impact. However, management highlighted they have gained market share in the water purifier category. Smaller categories: robotic, water softeners and air purifiers (grew 3x YoY) delivered healthy growth. Service business momentum builds up with third successive quarter of double-digit AMC bookings growth. Gross margin grew 340/410bps YoY/QoQ to 61.2%, driven by COGS reduction program, lower discounting and change in channel mix (lower e-com sales). Employee expenses grew 7% YoY, while other expenses grew 21% YoY led by 23% growth in A&SP spends. So, EBITDA margin expanded by 70bps YoY (-200bps QoQ) to 10.6%, leading to 16/15% growth in EBITDA/APAT.

Earnings Call Takeaways and Valuation

The management highlighted channel inventory pressures have eased across channels, except e-com, which will normalize by Q4FY26-end. It guided Q4 revenue growth will be higher than 11% delivered in 9MFY26. Service bookings grew at mid to high teens YoY in 9MFY26. The robotics business maintained strong traction, representing about two-thirds of vacuum cleaner revenues. Considering muted Q3 performance and elevated inventory in e-com channel, we have trimmed our revenue estimates by 2% each for FY26-28E and APAT estimates by 3/2% for FY26/27E, respectively, while broadly maintaining for FY28E. We maintain BUY with an unchanged TP of INR 830/sh, valued at 45x Mar-28E AEPS (excluding non-cash intangible amortization and 50% of performance-based ESOP expenses).

Financial Summary

Source: HSIE Research (HSIE Results Daily Report – 06 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.