HSIE Institutional Report: Galaxy Surfactants Feb, 17 2026

Authored By Prime Research | Last Modified: Feb 17, 2026 11:15 AM IST

Speciality Driving Revenue

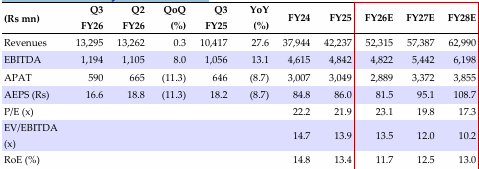

Our BUY recommendation on GALSURF with a price target of INR 2,647 is premised on (1) continuing demand in Rest of the World (RoW) markets; (2) shift in mix toward high-margin products; and (3) a strong balance sheet. Q3 EBITDA was 9% above our estimates owing to lower-than-expected raw material cost while revenue remained in line with estimates; PAT was 7% below estimates. The company has made incremental provision of INR119mn toward increase in gratuity and leave encashment owing to new labor codes.

Financial Performance

Q3 revenue increased by 27.6% YoY to INR 13.29bn while remaining in line with Q2. Specialty segment volume grew by 8% YoY while volumes in performance segment fell by 6% YoY. Total volumes were down 1.17% YoY. Gross profit per kg increased to INR54.5/kg from INR49.20/kg in Q2 while EBITDA/kg increased to 19.39/kg in Q3 from INR16.44/kg in Q2, driven by premium specialty. Continued higher raw material prices and reformulation pressure impacted the revenue in the quarter. Raw material prices (palm oil) softened but average price remained on the higher side; EBITDA margin changed by -116/+64 bps YoY/QoQ to 9%.

Post Result Con Call Takeaways

(1) Domestic performance was impacted by reformulation by customers to counter the elevated feed stock prices. The performance segment degrowth was offset by volume growth in the specialty segment. (2) Revenue in AMET region was impacted by the increased local competition although some volumes are expected to rebound in Q4. (3) RoW revenue growth was led by Latin America and Europe while it was offset by softer demand in North America due to uncertainty related to tariff. Tri-K generated stronger revenue driven by super specialty business. (4) Galaxy has launched five new products in sun care segment. (5) Reduced US reciprocal tariffs have led to reduction in the landed cost and in the near term, it will help build traction and reinstate the existing customer pipeline.

Financial Summary (Consolidated)

Source: HSIE Research (HSIE Results Daily Report – 17 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.