HSIE Institutional Report: General Insurance Corporation Feb, 12 2026

Authored By Prime Research | Last Modified: Feb 12, 2026 01:23 PM IST

Consistent on Execution

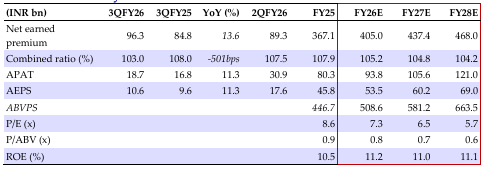

General Insurance Corporation (GICRE) reported in-line NEP/PAT growth of +14%/11% YoY, driven by steady improvement in underwriting performance. GICRE continued to witness improvement in loss ratios, which improved by ~250bps YoY. GICRE, India’s leading re-insurer (FY25 domestic market share: 51%), benefits from 4% mandatory domestic re-insurance cessation, and right of-first-refusal (ROFR), which offers preferential access to domestic re insurance placements. With the rating upgrade to A- (previously B++) by AM Best, GICRE is likely to grow faster on international business, given enhanced qualifying criteria for participation in overseas reinsurance market, although growth was modest at 7% for 9MFY26. We flag the inherent risk to GICRE’s topline from potential abolition of obligatory cessation, alongside moderation in domestic market share on account of rising competition from foreign re insurer branches, cross-border re-insurers, and domestic insurers’ risk retention strategy. We build 8% NEP CAGR over FY25-28E and a 15% PAT CAGR on the back of stronger float income from the investment book (INR1.6tn). We maintain ADD with a revised TP of INR490 (0.8x Sep-27 BV).

Shift in Business Mix Towards Motor

During the quarter, overall NEP grew 14%, primarily led by growth in the motor segment (15% YoY), stronger than the industry growth of 11%, owing to business from new proportional treaties added over the past couple of quarters. This has contributed to meaningful improvement in profitability, given the lower combined ratio (COR) in the motor business compared to the health business.

Improving Profitability

GICRE has focused on improving its profitability and consistently de-risking its domestic as well as international business. The management guided for a 100-120bps improvement in combined ratio (COR) for FY26E (achieved ~500bps YoY during 9MFY26). Given these outcomes, we don’t expect any material improvement in COR for FY27E and FY28E.

Overhang From Potential End to Obligatory Cessation

With the Indian re insurance market beginning to mature, grant of approval to Indian re-insurer Valueattics, and the increasing presence of global re-insurers such as Swiss Re and Munich Re, the industry has been lobbying for abolition of 4% obligatory cessation. Our analysis suggests a 15-20% adverse knock to GICRE’s domestic premium, in case the IRDAI removes mandatory cessation.

General Insurance Corporation Financial Summary

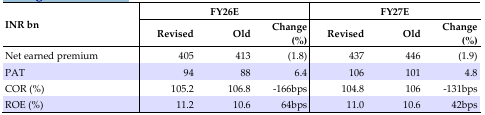

Change in Estimates

Source: HSIE Research (HSIE Results Daily Report – 12 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.