HSIE Institutional Report: Godrej Properties Feb, 06 2026

By Prime Research | Last Modified: Feb 6, 2026 01:49 PM IST

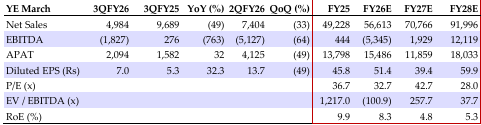

Execution Weakness Led to a Drag in Margins

Godrej Properties Ltd (GPL) reported presales at INR 85bn (+54.6/-1.0% YoY/QoQ, with a booking area of 6.4msf (+58.2%/-9.9% YoY/QoQ). It delivered 1.7msf of projects in Q3FY26. It added 12 new projects with a GDV of INR 246bn in 9MFY26 (achieving 123% of targeted guidance for FY26). The company has laid out a conservative target of INR 325bn (10% YoY) presales for FY26, backed by a strong launch pipeline worth over INR 400bn. Aggressive project acceleration, marked by a 66% rise in construction expenditure over nine months, drove a 7% decline in operating cash flow as higher upfront costs outpaced collections, lowering the cash flow to collections ratio. GPL expects demand to remain stable and end-user driven. With a strong balance sheet, prudent capital discipline, and no near-term equity dilution planned, GPL is well-positioned to deliver 20%+ earnings CAGR through FY28, driven by strong execution, rising monetization from legacy projects, and margin accretion from premium launches. Given robust presales outperformance, new launches and strong underlying demand, we believe that GPL is all set to outperform guidance. We maintain our ADD rating with a reduced TP of INR 2,082/sh (cutting our NAV growth premium from 35% to 15% as presales growth, on a high FY26 base of INR 330bn, is expected to slow down from 25 30% to 5-10%).

Q3FY26 Financial Highlights

Revenue came in at INR 4.9bn (-49.2%/-33.1% YoY/QoQ, a miss by 51.0%). EBITDA: INR -1.8bn (vs INR +217mn/-5.1bn Q3FY25/Q2FY26) against an estimated EBITDA of INR -1.1bn. APAT: INR 2.1bn (+32.1%/-49.1% YoY/QoQ, a miss of 66%). Margins were impacted due to CCM-based accounting policies and pushing out of deliveries to Q4FY26.

Strong Demand Drives Presales Momentum

Presales for Q3FY26 stood at INR 84bn (+54.6/-1.0% YoY/QoQ), with a booking area of 6.4msf (+58.2%/ 9.9% YoY/QoQ). This was led by strong demand in some key new project launches where MMR contributed 38% of total presales, largely led by Godrej Trilogy at Worli (INR 17bn), followed by Panipat and Noida launches. For FY26, GPL has guided a conservative target of 10% presales growth, which we believe it shall surpass, owing to robust launches in Q4FY26.

Expansion Drive Leads to Higher Debt

GPL net debt increased to INR 68.7bn (vs INR 55.6bn QoQ) and net D/E increased to 0.37x vs 0.30x QoQ. In 9MFY26 GPL added twelve new projects with a saleable area of 22.3msf and a GDV of INR 246bn (achieving 123% of INR 200bn targeted for FY26).

Consolidated Financial Summary (INR mn)

Change in Estimates (INR mn)

Source: HSIE Research (HSIE Results Daily Report – 06 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.