HSIE Institutional Report: Happiest Minds Technologies Feb, 11 2026

Authored By Prime Research | Last Modified: Feb 11, 2026 12:15 PM IST

AI-led Growth Acceleration; Margin Focus

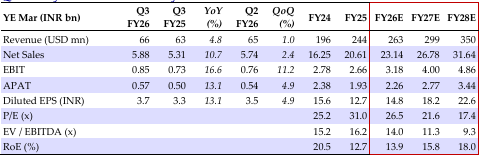

HAPPSTMN delivered a steady Q3 performance, with revenue growth in line with expectations and margins exceeding forecasts. The company reported +1.2% QoQ CC revenue growth, driven by the BFSI and healthcare verticals. This company clocked 10.2% CC growth for 9MFY26, in line with the target to deliver double‑digit CC revenue growth for FY26E. The management remains confident in its multi‑year growth trajectory, supported by the scaling GBS unit and an improving deal pipeline with greater visibility. The GBS unit turned profitable in Q3, marking an important milestone, and continues to broaden its suite of replicable AI solutions. HAPPSTMN plans to increase its AI team to 1,000 people by the end of FY27E. The demand environment remains selective, with momentum cantered around workflow automation using GenAI and Agentic AI, AI‑enabled productivity, and modernization of core platforms. The FY26E outlook is maintained, targeting CC revenue growth of >10% and EBITDA margins in the 20–22% band (including other income). We maintain our BUY rating on HAPPSTMN with a TP of INR 670, based on 30x Mar‑28E EPS, supported by a 13/21% revenue/EPS CAGR over FY25–28E.

Happiest Minds Technologies Q3FY26 Highlights

(1) Revenue came in at USD 65.7mn (vs HSIE USD 65.8mn), +1.2% QoQ CC, supported by healthy growth in healthcare (+16% QoQ), BFSI (+3.7% QoQ) and industrial verticals (+2.4% QoQ). (2) GBS revenue grew 50% QoQ and turned profitable in Q3, driven by improved execution discipline and more use cases moving from pilots to production. (3) EBITDA margin stood at 18.2% (+100bps QoQ), led by operational efficiencies, favorable forex, GBS turning profitable, and improved utilization, partially offset by fewer working days and a forex loss (INR 62mn). (4) Q4 revenue growth is expected to be driven by continued momentum in BFSI, healthcare, and GBS while stability is expected in retail and hi-tech verticals. Management has maintained its revenue growth target of 10% plus CC for FY26 with EBITDA margin in the 20-22% range.

Outlook

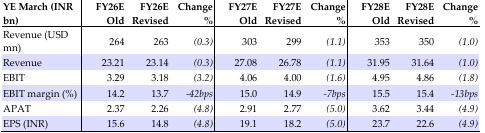

We have factored in USD revenue growth of 7.8% for FY26E (4.8% organic) and 14/17% for FY27/28E. EBITM has been factored in 13.7/14.9/15.4% for FY26/27/28E. At CMP, HAPPSTMN is trading at 22/17x FY27/28E, lower than its historical average multiple of 48x.

Quarterly Financial Summary

Change in Estimates

Source: HSIE Research (HSIE Results Daily Report – 11 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.