HSIE Institutional Report: Indian Hotels Feb, 13 2026

Authored By Prime Research | Last Modified: Feb 13, 2026 12:03 PM IST

Long-Term Outlook Strong Despite Soft Short-Term Performance

IHCL’s Q3FY26 performance was relatively soft, reflected in modest 12% YoY revenue growth. 9% YoY RevPAR growth at consolidated level was mainly led by modest ARR increase by 7% to INR 17,700, whereas occupancy remained high at ~78% (+1.2pp). Taj continues to be the lead revenue generating brand, with 69% of operating revenue coming from this luxury segment while TajSATS and the Upscale segment (Vivanta, SeleQtions, and Gateway) accounted for 13% and 10% of total revenue, respectively. Despite soft growth of the quarter, long-term prospects of the company remain healthy as hotel supply growth of ~5% during FY25-28E is estimated to lag demand growth (~9%) in key business locations. It will lead to sustained high occupancy; however, we believe ARR might be peaking at a few locations. Hence, in our view, growth in operational rooms happens to be the key growth driver hereon. IHCL has acquired 51% stake in Atmantan resort and is in process of acquiring 51% stake in Bridge hotel. Together, they have a revenue potential of INR 2bn in FY27E. Further, Taj Bandstand, Mumbai is a large upcoming luxury asset with ~450 keys, expected to generate INR 10bn upon stabilization with 50% EBITDA margin. Above growth drivers apart from existing hotel portfolio and future pipeline are expected to drive EBITDA growth hereon. As stock has steeply corrected by ~13% in the last two quarters, it has come to more reasonable valuation levels. Hence, we change our rating to “Add” from “Reduce” despite keeping similar EBITDA CAGR estimates of 16% for FY25-28E. We roll forward to FY28E and value the stock at 25x FY28 EV/EBITDA for a TP of INR 801.

Indian Hotels Q3FY26 Highlights (Consolidated)

IHCL’s revenue grew 12% YoY to INR 24.4bn, while EBITDA rose 12% YoY to INR 10.7bn. Net profit showed stronger growth, increasing 16% YoY to INR 6.7bn. Air catering segment Taj SATS reported 18% YoY topline growth. EBITDA margin of hotel segment was higher at ~41% vis-à vis ~26% of air catering segment. High single digit RevPAR growth was mainly led by modest ARR increase, while occupancy remained high at ~78%. As a part of the asset-light growth strategy, managed hotel rooms grew by a healthy 55% YoY to 17,677, and management fees rose by 15% YoY to INR 2.03bn. The company expects to continue capitalizing on its brand strength to grow its asset light portfolio.

Group Update (Q3FY26)

New business (Ginger, ama, and Qmin) contributed 8% of total revenue, recording a 31% YoY growth to INR 2.15bn, with a 46% EBITDAR margin.

Outlook

IHCL opened 89 new hotels (3,747 keys) in Q3 FY26 and has a planned opening of 10 hotels (~850 keys) in Q4 FY26. On a base of 32,296 keys (55% managed, 45% owned) across 361 operational hotels, the company is planning a strong expansion and has a pipeline of ~30,200 (owned ~5,940 keys and managed~ 24,360 keys) additional keys across 256 hotels. Upcoming marquee owned projects include Taj Bandstand (450 Keys), Ranchi (~200 keys), Lakshadweep (~183 keys) Taj at Shiroda (~300 keys), Gateway at Aguada Plateau (~110 keys), Kaziranga (80 keys) and Agartala (~100 keys). We believe with disciplined execution; the company is on its trajectory to register ~16% EBITDA growth for FY25-28E.

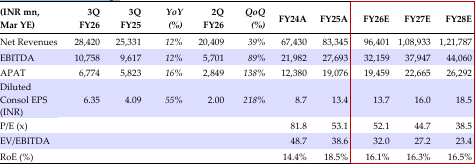

Financial Summary

Source: HSIE Research (HSIE Results Daily Report – 13 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.