HSIE Institutional Report: Indraprastha Gas Feb, 16 2026

Authored By Prime Research | Last Modified: Feb 16, 2026 10:28 AM IST

Lower Gas Cost Lifts Margin

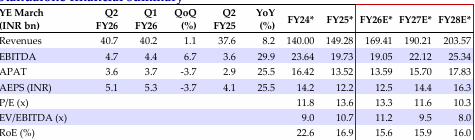

We maintain our BUY recommendation on Indraprastha Gas (IGL) with a target price of INR 255, given (1) volume growth at ~7% CAGR over FY25-33E; (2) robust margins supported by higher gas allocation from the high-pressure, high temperature (HPHT) fields to the priority sector; and (3) a strong portfolio of new geographical areas (GAs) ensuring volume growth visibility. Q3FY26 EBITDA at INR 4.7bn (+29.9% YoY, +6.7% QoQ) and APAT at INR 3.6bn (+25.5% YoY, -3.7% QoQ) were in line with our estimates.

Volumes

Blended volume stood at 9.43mmscmd (+3.5% YoY, +1.2% QoQ). Sequential volume growth was driven by the Domestic PNG segment, which reported volume of 0.78mmscmd (+7.8% YoY, +13.5% QoQ) and the industrial commercial PNG segment, the volumes of which stood at 1.22mmscmd (+2.9% YoY, +5.3% QoQ). CNG volumes declined sequentially to 6.93mmscmd (+3.4% YoY, -0.6% QoQ) and trading volumes stood at 0.5mmscmd (flat YoY/QoQ). We expect infrastructure expansion in existing and new areas to support volume growth of ~7% CAGR over FY25-33E. We estimate volume of 9.29/10.05mmscmd for FY26/27E.

Margins

Per-unit GM came in at INR 11.1/scm (+13.9% YoY, +7.7% QoQ) and per unit EBITDA margin came in at INR 5.4/scm (+25.6% YoY, +5.4% QoQ). Gas cost decreased sequentially to INR 35.8/scm (+2.0% YoY, -2.3% QoQ) as the price of brent cooled off in Q3 (58% of total gas sourced is linked to brent). Opex was at INR 5.6/scm (+4.6% YoY, +10.0% QoQ). Realization stood at INR 46.9/scm (+4.6% YoY, -0.1% QoQ). We estimate a per unit EBITDA margin of INR 5.6/6.4 per scm for FY26/27E.

Key Highlights

(1) CNG – Excluding DTC buses portfolio, CNG volume grew 10% YoY. Currently, there are close to 100 DTC CNG buses which consume 5,000 kgs of CNG per day (44k/155k kgs/day in Q2FY26/Q3FY25). By March 2026, DTC will withdraw all the CNG buses. Volume growth of the segment was impacted due to the implementation of GRAP regulations in the Delhi region during the quarter. Management noted that post the reduction of GST on CNG vehicles, the number of CNG vehicles being sold has increased from 21,000 per month to 26,000 per month in IGL’s GAs. (2) Gas cost – reduction in crude oil prices led to the sequential expansion of per unit gross profit. However, a one-time provision made due to implementation of the new labour code impacted EBITDA margin by INR 0.30/scm. Revised transmission tariff, reduction of tax in Gujarat, adjusting for one-time impact due to labour code in Q3 shall add INR 0.75/0.25/0.30 per scm respectively to the per unit EBITDA. (3) Capex – INR 8.47bn worth of capex was incurred in 9MFY26. For FY26/27, the company plans to invest INR 12.5/15bn in the core business. Additional INR 8bn to be invested in other business segments in FY27. (4) Guidance – Volume should reach 10mmscmd by the end of FY26 and grow by 1mmscmd in FY27/28 each. EBITDA should reach INR 7/mmscmd by the end of FY26, aided by reduced transmission tariff and decrease in tax on gas sourced from Gujarat (50% of total gas consumed is sourced from Gujarat).

DCF Based Valuation

We maintain BUY with a revised the TP of INR 255/sh (previously INR 249/sh; WACC 10.5%, terminal growth rate 1.5%). The stock is trading at 11.6x Mar-27E EPS.

Standalone Financial Summary

Source: HSIE Research (HSIE Results Daily Report – 16 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.