HSIE Institutional Report: IPCA Laboratories Feb, 17 2026

Authored By Prime Research | Last Modified: Feb 17, 2026 12:07 PM IST

Base Business Remains Strong; Unichem Ramp Up Key

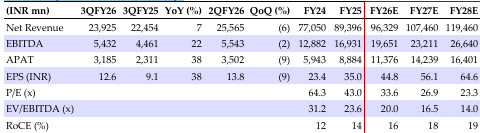

EBITDA growth of 22% YoY was driven by 7% YoY sales growth (India grew 12% YoY), higher GM (+226 bps YoY at 72.5%), and cost controls (staff/SG&A +10%/+4% YoY), causing the margin to expand to 22.7% (+284 bps YoY). IPCA expects (1) overall business to see 10-11% growth in the near term (IPCA standalone growth at 10-12% and Unichem business at 8-9%); (2) India business to outperform IPM growth in the next few years, led by sustained momentum in key therapies (pain, CVS, anti-diabetics, CNS, and derma); looking to in licensing Semaglutide to participate in India GLP-1 market; (3) export formulation to see gradual improvement, led by traction in the EU and UK businesses, scale-up in the US business, and steady growth in branded generics; to sustain 10-12% YoY in near term; (4) API business to see slightly slower growth; (5) Unichem to see gradual pick-up in growth momentum from FY27/28E, led by product commercialization across EU and RoW markets (registration process started and approval may take 10-12 months) as well as new launches in the US; and (6) consolidated margin to improve by ~150 bps p.a. for the next couple of years; aims to achieve Unichem margin of 15% in the next 2-3 years and it hopes to reach 18-20% sustainable margin in the long term. We believe IPCA is well-positioned for growth (~10% CAGR over FY25-28E), given steady India growth (new launches, steady growth in focused therapies, and scale-up in chronic categories) and export formulation ramp-up (through Unichem integration and new launches in the EU/RoW), with improving margins (~16%/23% EBITDA/PAT CAGR over FY25-28E). Considering Q3 results, we have reduced the EPS by 5/2% for FY26/27E, while maintaining for FY28E and revised the TP to INR 1,750 (28x Q3FY28E EPS). Maintain BUY.

IPCA Laboratories Q3 Highlights

Sales grew 7% YoY to INR 23.92bn. India (41% of sales) grew 12% YoY, branded generics grew 28%, generics exports grew 21%, and institutional declined 21%, and API was flat (India/export -14%/+6%) and Unichem (22%) declined 2% YoY. Higher GM at 72.5% (+226 bps YoY) and moderate costs (staff/SG&A +10%/+4% YoY) led to EBITDA^ of INR 5.43bn (+22% YoY) with a margin of 22.7% (+284 bps). Muted other income and moderate interest/depreciation (+5%/9%) led to reported PAT of INR 3.26bn (+31% YoY). Adjusted for one-offs^, PAT stood at INR 3.18bn (+38% YoY).

Key Takeaways From Con Call

Overall, US sales (IPCA + Unichem) grew 17% YoY to INR 3.95bn (for 9M it grew 15% to INR 11.4 bn). It expects Unichem to gradually improve through cost optimization, shifting API sourcing to IPCA’s in-house facilities, ramping up operations in EU and RoW markets with new product registrations, and improving capacity utilization. The company expects to start tech-transfer and manufacturing for two biosimilars soon (five candidates under development) and is targeting global markets.

Quarterly Financial Summary

Source: HSIE Research (HSIE Results Daily Report – 17 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.