HSIE Institutional Report: IRB Infra Feb, 17 2026

Authored By Prime Research | Last Modified: Feb 17, 2026 11:16 AM IST

Toll Revenue and Execution Drive Performance

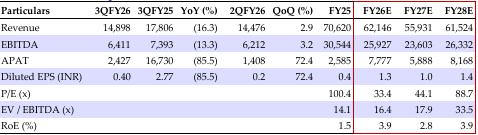

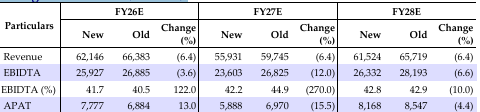

IRB Infrastructure Developers (IRB) reported strong revenue/EBITDA/APAT of INR 14.9/6.4/2.4bn, a beat/(miss) of +2.7/-1.2/+26.9% to our estimates; APAT growth reflects resilient operating performance and disciplined cost management. IRB basis strong performance announced 1:1 bonus with interim dividend announcement to reward shareholders. The order book (OB) as of Dec’25 stood at INR 373bn (~5.3x FY25 revenue), with EPC and O&M accounting for ~4%/96% of the overall OB. IRB has guided for INR 34bn revenue from EPC and O&M, with margin guidance for O&M at 20%, while being net-debt-free balance sheet by FY30, driven by disciplined capital allocation and calibrated asset monetization. Improved capital efficiency can support cash RoE targeted by IRB to expand from ~8% to 14%+ by FY32. IRB’s access to two InvIT platforms (IRB InvIT Fund and IRBIT) has facilitated capital unlocking through asset monetization and will continue to unlock value with future asset transfer. It is also planning to pursue further opportunities in the TOT segment. Given weak ordering, we have cut our estimates on EPC. We maintain our ADD rating, with a reduced SOTP target price of INR 54/sh.

IRB Infra Q3FY26 Financial Highlights

Revenue stood at INR 14.9bn (-16.3/+2.9% YoY/QoQ, a beat of 2.7%) while EBITDA came in at INR 6.4bn (-13.3/+3.2% YoY/QoQ, a miss of 1.2%). The EBITDA margin stood at 43% (+151/+12bps YoY/QoQ vs. our estimate of 44.4%). The APAT stood at INR 2.4bn ( 85.5/+72.4% YoY/QoQ, a beat of 26.9%, driven by reflecting resilient operating performance QoQ and disciplined cost management). Net debt stood at INR 84bn in Q3FY26 (Q2/Q1FY26: INR 125/120bn; Q3FY25: INR 119bn), with a net debt to equity ratio of 0.41x in Q3FY26 (Q2/Q1FY26: 0.61x/0.86x; Q3FY25: 0.6x).

Q3FY26 Business Vertical Highlights

The average daily toll collection for wholly-owned concessions (four assets; one TOT, one BOT and two HAM (under-construction)) came in at INR 73mn in 9MFY26 (FY25/24: INR 69/66mn); for Private InvIT, toll collection stood at INR 95mn (FY25/24: INR105/85mn). In Q3FY26, revenues from construction, BOT/TOT, and InvITs/other segments contributed 41.9/37.8/20.4% respectively (compared to Q2FY26: 46.8/35.8/17.3%).

Order Wins Provide Revenue Visibility

Order inflow (OI) includes wins of TOT-17 & TOT-18 (FC underway) in Q3FY26 worth INR 93/40bn respectively. Management continues to expect total projects worth INR 100-120bn under TOT and fewer under BOT which are to be awarded in the near term.

Financial Summary (INR mn)

Change in Estimates (INR mn)

Source: HSIE Research (HSIE Results Daily Report – 17 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.